UK set for negative growth as cost of living crisis bites

We're now pencilling in negative growth for the second quarter as health spending falls and the cost of living squeeze begins to really bite. The Bank of England looks set to press pause on its tightening cycle by the summer

Expect at least one quarter of negative growth

The UK economy is heading into the midst of one of the largest cost of living crises for several years. Per head, the Office for Budget Responsibility (OBR) reckons the next fiscal year will be the worst for disposable incomes in decades. Yet perhaps the more surprising thing, given that backdrop, is that most forecasters (including the OBR) are not predicting a recession.

We’re a little more cautious – even if we agree a technical recession may well be avoided – and we’re now pencilling in negative growth for the second quarter. Household energy bills rise by 54% on average this week and consumer confidence has plunged as a result. Petrol prices look like they’ve peaked for now, but that’s unlikely to stop the overall inflation rate peaking above 8% during April.

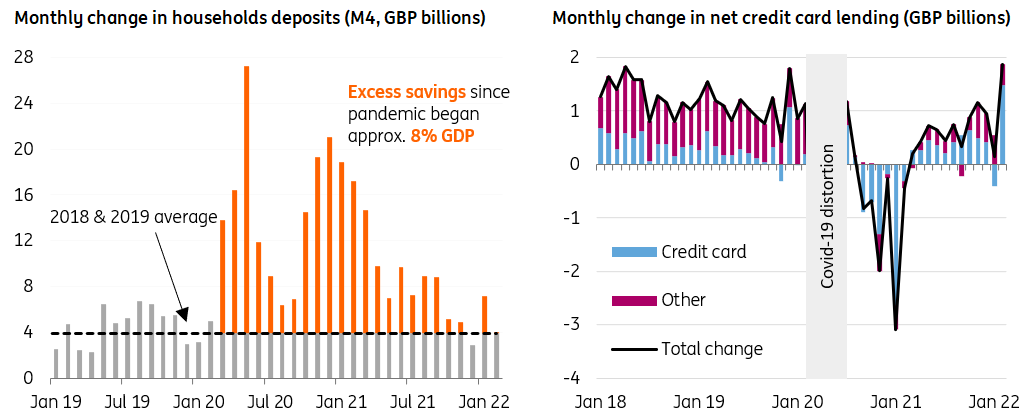

Savings built up through successive lockdowns, amounting to 8% of GDP, will offer a partial offset, even if they are believed to be more heavily concentrated among higher earners, who are less likely to cut back spending in response to inflation. Indeed households are adding to bank deposits at the slowest rate since the start of the pandemic, while the most recent month saw net credit card borrowing shoot higher.

Households have scaled back savings and increased net credit card borrowing

Admittedly the consumer isn’t the only story here. Health spending, which feeds into GDP, will be sharply lower in April now that free Covid-19 tests have been substantially scaled back. This, more so than household spending, will probably determine the depth of any slide in economic growth in the very near term. The extra bank holiday scheduled for June will also artificially lower growth a tad before the summer.

If there’s one piece of good news, it’s that gas prices have fallen noticeably over the past few weeks. And that means the next update of the household energy cap in October will see prices rise by around 20-25%, rather than the 50%+ increases predicted at the start of March.

That’s still a big change – average bills will have gone from around £1,000 last April to around £2,700 in the autumn, net of a £200 government rebate. And in the meantime, plenty of other items, from food to air fares, will be adding to the crunch. Inflation is unlikely to dip below 6% this year.

While Chancellor Rishi Sunak announced some modest tax changes in his spring mini-budget, these are unlikely to offer much additional support to households. We suspect the government may be forced to go further over the coming months, especially if gas prices surge once more.

Having been laser-focused on higher inflation rates over the past few months, the Bank of England is becoming more cautious now that it has three hikes under its belt. After another rate hike in May (and perhaps one more thereafter), we think the committee will press pause on its tightening cycle.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

31 March 2022

ING Monthly: There’s nothing normal about the global economy This bundle contains 17 Articles