Lower gas prices point to a more modest recession in the UK

- 3 February 2023

- United Kingdom

Lower gas prices should herald a fall in consumer energy bills by the summer. A recession is still the base case, but the reduced squeeze on household incomes suggests the peak-to-trough fall in GDP could now be less than 1%

Lower gas prices are good news for UK consumers

Lower gas prices are as much of a boon for the UK as they are for the rest of Europe. It’s true that Britain has considerably less gas storage than its peers, making it more vulnerable on days of low temperatures and wind. But in general, lower prices point to lower consumer bills – and that means the hit to GDP this year is likely to be less than feared.

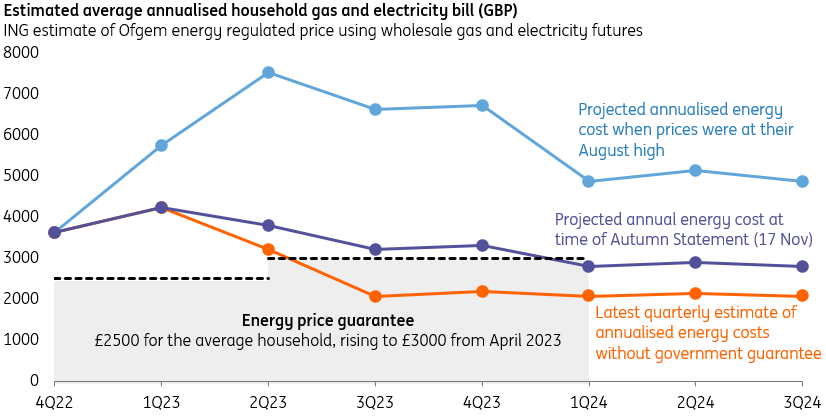

April’s planned increase in unit prices can probably be cancelled, and in fact, the average annual household bill is likely to fall from £2,500 under the government guarantee, to £2,000 over the summer. Such a move would shave roughly 1 percentage point off headline inflation later this year and means it would end the year only modestly above the Bank of England’s 2% target. Admittedly, business support is still set to become less generous, though with wholesale gas prices so much lower, this looks less consequential than it once did.

The average annual household energy bill should fall by the summer

The UK doesn't look like it will be a notable outlier on GDP

With the hit to household incomes diminished, we now think the peak-to-trough fall in UK GDP is likely to be less than 1%. Most of the hit is likely to fall in the first quarter. But while this still places the UK towards the bottom of the pack on growth (again), we think it’s an exaggeration to say it will be a notable outlier.

For instance, while higher mortgage rates are likely to weigh on 2023 growth, the UK doesn’t look any more exposed than much of Europe to a house price correction. Unlike somewhere like Sweden, which has so far seen a 15% fall in house prices, the UK has a very low share of variable rate mortgages and ranks in the middle-of-the-pack on household indebtedness, as well as on increases in price-to-income ratios over recent years.

The situation is trickier for businesses, particularly smaller corporates where floating rate lending makes up 70% of outstanding debt. Survey data suggests that’s a particular issue in consumer services and real estate. The latter, combined with weaker homebuyer demand, unsurprisingly points to a fall in construction this year.

For now, the Bank of England is more focused on persistently strong wage growth and service-sector inflation. While it looks like we’re close to the top of this tightening cycle, we think the UK’s somewhat unique combination of structural labour shortages and exposure to Europe’s energy crisis points to somewhat sticky core inflation. That suggests the UK is likely to be slower than the US Federal Reserve to cut rates, and we don't expect policy easing before next Easter.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING’s February Monthly: This could well be a ‘fool’s spring’

- This bundle contains 12 Articles