UK jobs: Why this recovery may be different

- 19 April 2021

- United Kingdom

While the UK unemployment rate is likely to rise towards 6-6.5% this year as the furlough scheme comes to an end, there's a fair chance the situation may already be gradually improving again by year-end, barring any more Covid-19 surprises

The jobs market has calmed down over the winter - thanks to furlough

When asked where UK unemployment will be at the end of this year, most economists – ourselves included – would probably say 'higher than it is now'. But predicting how high remains a tricky question to answer and highlights how several aspects of the crisis in the jobs market differ from previous recessions.

Forecasting how high unemployment will be at the end of this year remains a tricky question

Let’s start with the noticeable difference – the furlough scheme. The extension of wage support through the winter lockdown – and now until the end of September – has helped the jobs market turn a tentative corner over recent months.

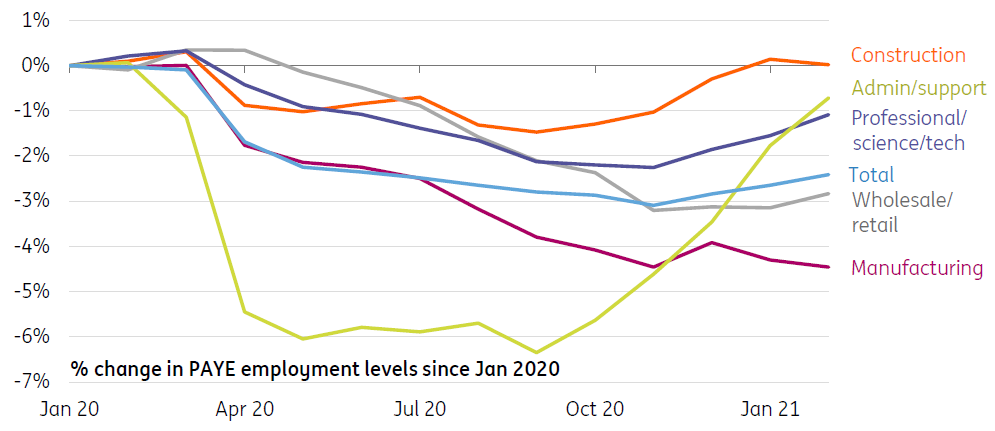

While payroll-based employment is still down some 2.4% on pre-pandemic levels, we've begun to see a gradual recovery outside of the consumer services arena – no doubt as firms have become more adept at operating through lockdowns. The admin/support sector, for instance, has now all-but-erased the 6.3% fall in employment seen amid the pandemic.

Outside of consumer services, employment has generally stabilised/increased

Unemployment is likely to rise through the middle of 2021

Still, there is likely to be a further round of redundancies as the job retention scheme gradually comes to an end. The spike in job losses we saw last autumn, as firms prepared for the original October 2020 furlough end-date, shows what is at stake. Jobs data due tomorrow is likely to show the unemployment rate at roughly 5%, up from its pre-pandemic low of 3.8%.

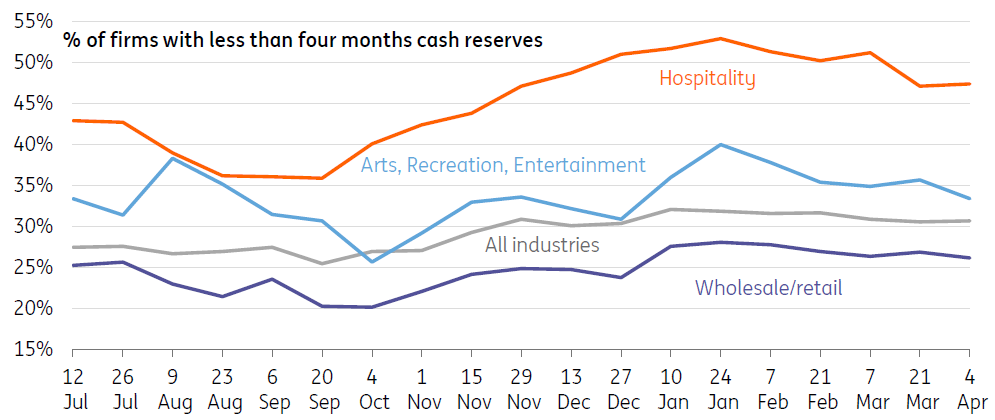

One concern is that consumer services firms remain under financial pressure. Office for National Statistics survey data consistently pointed to low cash reserves and weak confidence among the hardest hit sectors through the first quarter.

Jobs data due tomorrow is likely to show the unemployment rate at roughly 5%, up from its pre-pandemic low of 3.8%

However, the critical difference this time is that wage support (and other measures) are set to remain available until well after many sectors reopen. The hope is that this will give firms enough time to get back on their feet and therefore support most commercially viable roles back from furlough. While there will inevitably still be job losses, the ongoing support schemes may mean that these can be limited to roles that no longer exist – for instance, where the pandemic has caused lasting structural changes to business models.

Hospitality firms have been reporting reduced levels of cash reserves

Source: ONS Business Impact Survey, ING calculations

">

Migration is something of a wildcard for the jobs market

The second major difference compared to past recessions is the sharp spike in outward migration we saw last spring.

Economists are divided on its full extent, but recent ONS analysis suggests a 7.4% fall in the number of EU nationals on UK payrolls. That accounts for around a fifth of the drop in employment between 4Q19 and 4Q20.

Once vaccination rates have risen and Covid-19 cases stabilised across Europe, it's probably fair to assume a proportion of these workers will look to return. At that point, we may see a further, though temporary, rise in unemployment if not all manage to find jobs straight away. But this too is somewhat uncertain - and the FT reported this weekend that businesses in London (where the population fall appears to have been most stark) have found it tricky to find enough staff for reopening.

This recovery may be quicker than past jobs recessions

Altogether, we think the UK unemployment rate will rise to 6-6.5% later this year. But unlike past recessions, it may not stay there for long.

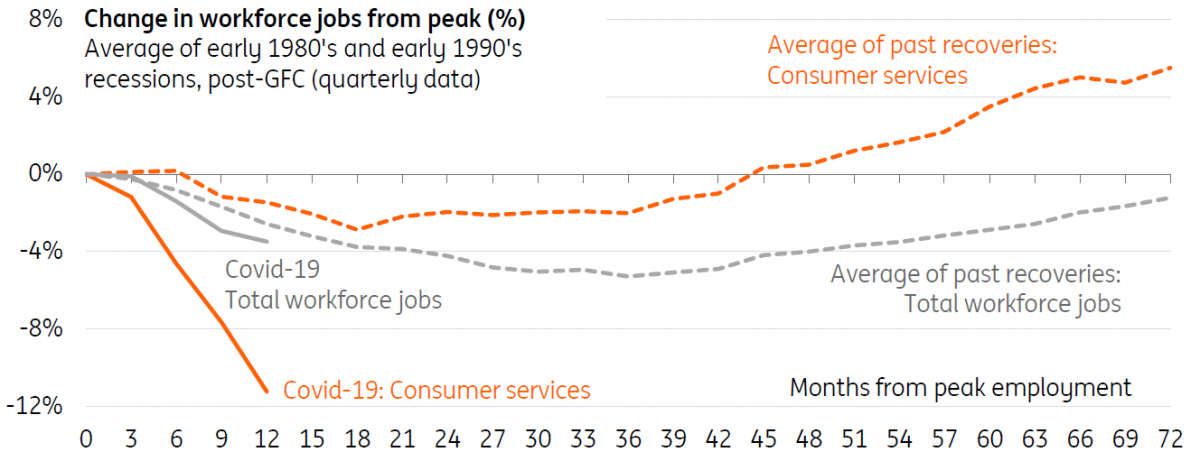

To explain why it's worth reflecting on the fact that so many of the job losses have so far been concentrated in the consumer services industry - something that is undoubtedly another unusual feature of this crisis. These industries (encompassing hospitality and arts, recreation and entertainment, and other services) have accounted for around half of the total fall in employment in 2020, though it varies slightly depending on which data you look at.

We think the UK unemployment rate will rise to 6-6.5% later this year. But unlike past recessions, it may not stay there for long

While this is not that surprising, it carries a potentially important implication for the recovery. Our chart below shows that these sectors typically weathered the previous three job recessions better than the broader economy, but more importantly, have often led the wider labour market out at the other end.

Consumer services tend to lead other sectors out of jobs market turbulence

One explanation is that the jobs market tends to be more fluid in these sectors.

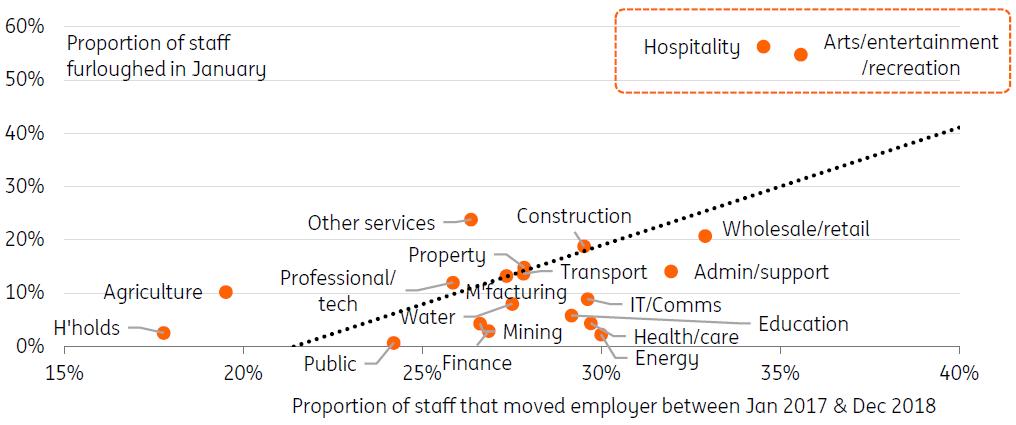

Here, jobs are often created much more quickly than elsewhere – perhaps linked to the fact that they tend to be more insecure forms of employment and are typically lower paid. Employee turnover is also noticeably higher in the likes of hospitality and arts/entertainment/recreation sectors than elsewhere – and the chart below shows a rough upward-sloping relationship between those sectors that have made the heaviest use of the furlough scheme and those with higher staff churn.

Hardest-hit sectors tend to have higher rates of employee turnover

Assuming the economy continues to recover as currently predicted, the upshot is that at least some of the jobs lost so far may return relatively quickly. And in turn, that could mean the recovery in the overall jobs market towards pre-pandemic levels may be more rapid than after the global financial crisis. We’d still expect it to take some time for employment to recover fully, and it's worth remembering that the upheaval caused by the new EU-UK relationship will also add pressure over time.

Returning to the question we posed at the beginning: will the unemployment rate be higher at the end of the year than today? The answer is probably yes.

But will it start to fall again by that point too? Barring another significant deterioration in the Covid-19 situation, there's a fair chance that the answer may also be yes.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more