UK inflation uncertainty makes life difficult for the Bank of England

- 11 March 2022

- United Kingdom

The war in Ukraine means that UK inflation is going to stay higher for longer. That indicates that the Bank of England is likely to raise rates again next Thursday and probably again in May. But with growth prospects deteriorating, we think that might be more or less it. Markets are likely overestimating the pace of tightening this year

Inflation could go above 9% if energy prices surge dramatically

The Bank of England will be very glad that it doesn’t have to publish new inflation forecasts when it meets next Thursday. Fortunately for policymakers, those can wait until May. And that’s probably just as well, given the volatility we're seeing in everything from gas prices to interest rate expectations. Inflation forecasts are changing markedly on a daily basis – and actually, if anything they've come a little lower in recent days.

Still, the direction of travel is clear – inflation is going to stay higher for longer. If energy prices stabilise around where they are at the time of writing, then we’d expect inflation to top out at around 8% in April, which is when the already-announced 54% increase in household energy prices will kick in. Headline CPI would stay above 6% for almost all of 2022.

Inflation forecasts are changing markedly on a daily basis

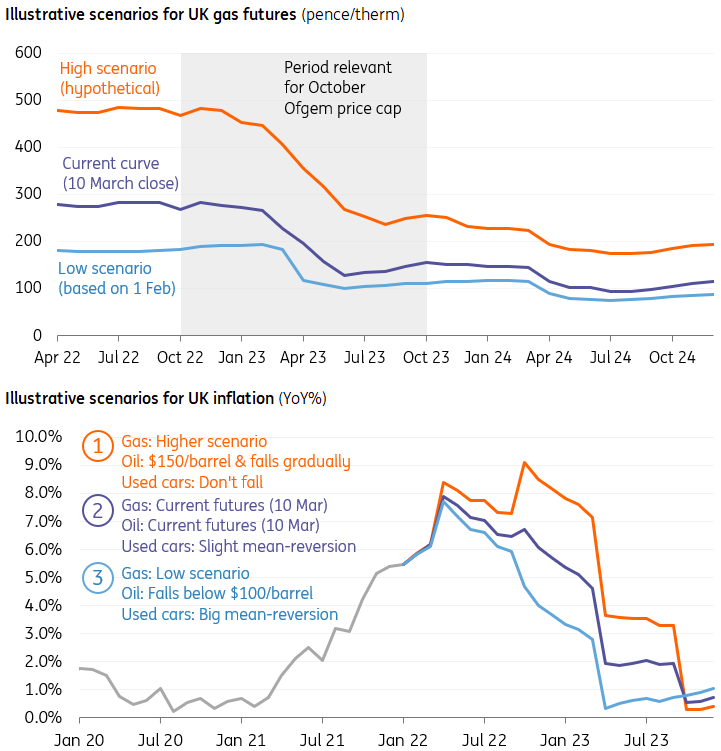

But if energy prices were to surge once more, then what really matters is how high household electricity and gas costs end up being capped in October (the cap is revised twice a year). Importantly this has little to do with the headline price of gas, which is currently based on delivery for April. Instead, the energy regulator Ofgem will consider futures prices covering the twelve-month period from October onwards.

If we take those futures prices as they stand – and make the fairly unrealistic assumption that they’ll stay there until the end of July, which is the ‘observation window’ Ofgem is monitoring – then October’s price cap could rise by around 35-40%. That’s net of a £200/household rebate from the government.

But that’s clearly only one of many scenarios. Our chart below shows a hypothetical scenario where gas prices for next winter rise dramatically once more, in which case October’s cap could increase by more like 75%. If oil were also to hit $150/barrel and stay elevated, then we could see a ‘double peak’ in inflation. Headline CPI would go above 9% in October.

Second-order effects are harder to predict

The much harder bit to forecast though is what happens to everything else. We know food inflation is likely to accelerate this year owing to higher commodity and fertiliser prices. Airfares are also a prime example given the pressure on jet fuel.

However, what remains much less certain is how far the war amplifies the strains on supply chains experienced during the pandemic. One interesting barometer will be used car prices, which have surged 30% in the last eight months alone, contributing more than half a percent to the current rate of headline inflation. Before the war, it looked possible that we’d see some mean-reversion in those prices as new vehicle availability improved. The tightness in metal markets risks prolonging last year’s supply challenges.

Bank of England to shift focus to deteriorating growth later this year

With inflation inevitably set to remain high throughout this year, markets have concluded that the Bank of England will double-down on tightening this year. Investors are once again forecasting six rate rises for the remainder of 2022.

But we remain less convinced. Barring a decisive increase in government support, it’s becoming increasingly hard to see consumer spending avoiding a downturn later this year. The £200 per household rebate from the government would have to increase to around £1000 to neutralise the projected increase for energy prices in October.

'Excess savings' accumulated through the pandemic - now totalling 8% of GDP - will provide a reasonable offset, albeit much of this is concentrated away from lower-income earners who will be most vulnerable to price pressures.

We think focus will quickly shift to the deteriorating growth outlook

But ultimately a surge in energy costs generally ends up being medium-term disinflationary given the lower spending, even if it keeps headline inflation rates higher in the short term. Indeed, in most scenarios, we'd expect inflation rates to dip below target by late 2023 as base effects kick in.

In short, once the Bank of England has got another couple of front-loaded hikes under its belt, we think the focus will quickly shift to the deteriorating growth outlook. Remember that even before the war, the Bank of England was forecasting an increase in unemployment and below-target inflation - and that was based on a market that was pricing fewer hikes than it is today.

We expect another 25 basis-point rate rise next week, and probably another in May. But that might be more or less it.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more