UK energy plan boosts net-zero but does little to reduce short-term gas dependence

- 8 April 2022

- Energy Sustainability United Kingdom

The UK government's Energy Security Strategy offers new details on offshore wind and nuclear generation plans. But while the strategy is a necessary step forward in the UK's net-zero journey, it still leaves the UK reliant on natural gas in the meantime. That means Britain is vulnerable to further bouts of power price volatility over the coming years

The UK has unveiled a new Energy Security strategy

Countries across Europe are grappling with energy security following the war in Ukraine when the world is under growing pressure to step-up climate mitigation policies. The latest IPCC report from the UN offered a renewed warning that the chances of limiting global warming to 1.5°C are diminishing.

The UK government is the latest to unveil a new strategy for securing energy independence. And what stands out immediately is that, unlike the EU’s recent REPowerEU plan, the strategy is much less about shoring-up near-term sources of supply and much more about long-term ambitions to reduce reliance on imported energy.

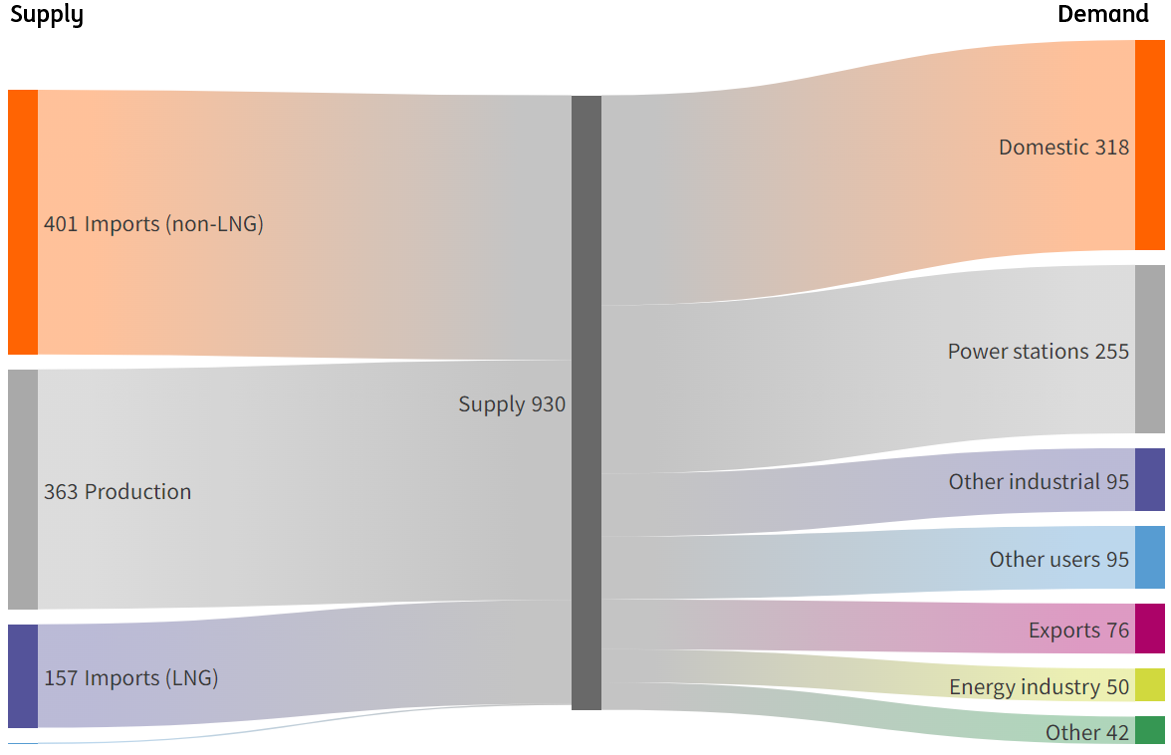

That’s not totally surprising. After all, the UK only sources 5-10% of its natural gas from Russia, despite relying on the fuel for roughly a third of its energy needs. Compare that to Italy, which is similarly reliant on gas, but which directly sources around 50% of the fuel from Russia.

Indeed, a little under half of the UK’s gas supply comes from domestic production, and around a quarter of the remaining imports come via LNG. Britain’s comparably large quantity of spare LNG regasification capacity offers greater scope to increase that share if required. In theory, the UK could even provide re-gassified LNG through existing pipelines to Northern Europe, where LNG capacity is often more limited – our team has written more about the EU’s challenges here.

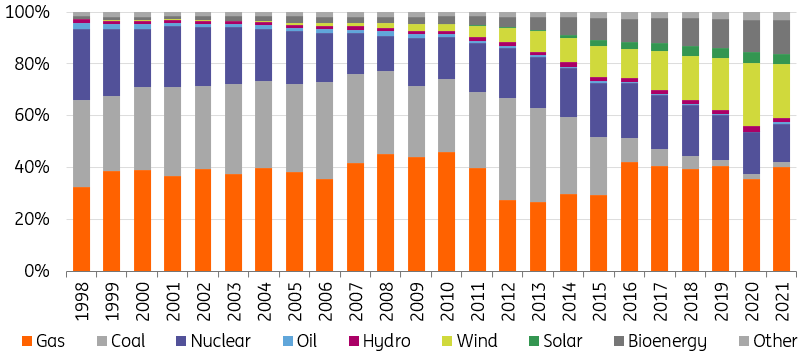

UK electricity generation by fuel (% total)

In short, the starting point for energy security in the UK is comparably favourable. Even so, the UK is still heavily reliant on gas, to the extent that the marginal price of electricity is effectively set by global gas prices. Unsurprisingly the UK has been among the most vulnerable to increased prices over recent months.

Reducing that reliance inevitably needs to be a key feature of any energy strategy. And the UK government is heavily pushing offshore wind and nuclear as the primary means of achieving that. Both were flagged in last year’s Net Zero Strategy, and Thursday’s announcement adds further colour to how it will be achieved.

The government has increased its target for offshore generation to 50GW by 2030, up from 40GW, with a new target for 5GW to come from floating turbines. Meanwhile, where Europe is more divided on the role of nuclear, the UK is hoping that new capacity can generate as much as 25% of electricity by 2050, including a role for small modular reactors (the government has recently asked the regulator to assess designs from Rolls Royce).

But a key challenge for the government is that many of these proposals – necessary though they are for achieving long-term net-zero and energy independence – contain few silver bullets to reduce the UK’s reliance on gas in the short/medium-term. And that inevitably means that Britain will continue to be vulnerable to volatility in power prices over the next few years for four key reasons:

No immediate alternatives to gas as a back-up fuel for renewables

Firstly, the rapidly growing role of wind and solar in the UK’s energy system necessitates a reliable backup fuel. That was a lesson learnt last summer when power prices spiked amid a period of unusually low winds.

Nuclear will play that role in the long term, but clearly it’s going to take well over a decade for enough new plants to come online. Before then, the share of electricity from nuclear will fall dramatically as much of the UK’s existing nuclear capacity is retired. The UK is also further ahead than most in phasing out coal, which is on the table again in parts of Europe as a short-term way to reduce gas dependency with Russia, despite being twice as polluting.

Achieving the targeted offshore capacity will also be gradual, given the associated planning decisions are often time-consuming (though the new strategy seeks to reduce that). The national grid will also require considerable investment to get the electricity onshore to where it’s needed and minimise imbalances in local power networks. For now, onshore wind, which is perhaps easier to deploy in the short term, is less favoured by the government.

Hydrogen target may lift gas usage

Secondly, the government is now targeting 10GW of hydrogen capacity this decade, double the original target. That’s ambitious, not least because the technology is in its infancy. And that – as the government implicitly accepts – will require some to be generated using gas-fuelled power (so-called ‘blue hydrogen’). In other words, hydrogen may actually increase the UK’s gas dependency in the short term.

Where the UK gets its gas - and how it uses it (TWh, 2021)

Alternatives for gas heating present a challenge

Thirdly, the UK faces an enormous challenge to reduce reliance on gas for domestic heating. Britain has the highest share of residual buildings built before 1945 in Europe. Gas is used for three-quarters of the UK’s domestic heating, second only to the Netherlands, and in turn, domestic usage accounts for over a third of total gas demand.

The new strategy hints that the government would like to utilise some of the new hydrogen capacity for domestic heating, given the potential to use a lot of existing infrastructure. But in practice, it’s heat pumps that most experts, including the government’s independent Climate Committee, see playing the dominant role in future heating systems (with any hydrogen reserved for industrial applications).

The government is now offering grants to help speed up the rollout of heat pumps, but these only work effectively where homes are well insulated. And as things stand, the UK has very little in place to help finance/incentivise household investment in efficiency products – there’s little discussion of this in the new strategy.

Gas storage capacity is limited

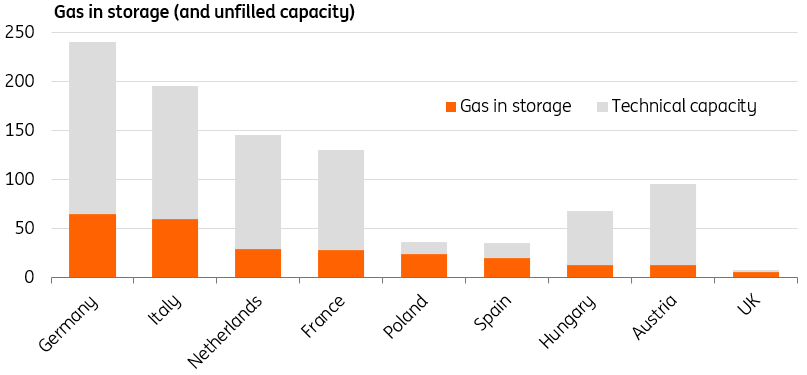

Finally, the UK’s gas storage capacity is extremely minimal. That follows the closure of Britain's largest storage site in 2017, which at the time provided 70% of the country's capacity.

A key target of the EU’s REPowerEU plan is to get its own stores 90% full ahead of next winter. For Italy, which consumes similar amounts of gas to the UK, that would mean roughly 175TWh in storage (based on current working capacity). The UK’s total working capacity is a little under 10TWh, leaving very little scope to ride out future short-term supply issues.

The UK has much less gas storage capacity than European neighbours

Growing pressure on the government to offer further economic support

For the UK economy, the more pressing question is whether the government will offer further support for consumers and businesses while gas prices remain elevated. Household energy prices rose by 54% at the start of this month, and gas futures point to another 30% increase in October. That’s net of a £200 per household rebate, which we think would need to increase to roughly £800 to neutralise the increase in energy prices due in October. Barring further support, and with real wages under pressure and consumer confidence falling, we now expect a modest fall in GDP in the second quarter.

Set alongside the risk of future bouts of power price volatility as the UK continues its necessary journey toward net-zero, there's a growing risk that the public becomes more disenfranchised. Maintaining the currently high levels of public support for renewable energy will be a key challenge for the government over the coming years.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

{kind=link}