UK: The good times and economic recovery return as Covid-19 recedes

Falling Covid-19 prevalence and widespread vaccinations have boosted confidence in the durability of the recovery. Several data points are at post-pandemic highs and that suggests second-quarter growth could hit 5%. Away from Covid-19, the main risks are politics-related; Brexit disruption is ongoing, while Scottish independence is back in focus

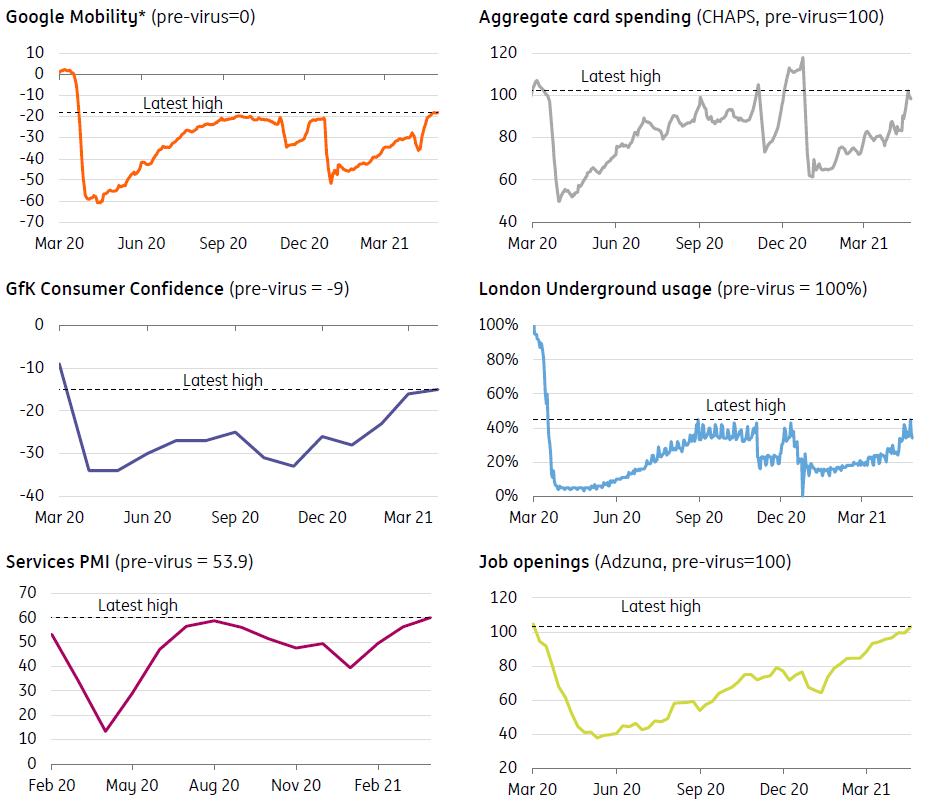

Pretty much wherever you look, there are signs that the UK economy’s long winter is starting to thaw.

What’s particularly interesting is that several indicators – from the PMIs to transport usage – are now higher than they were last summer, when restrictions were at their pre-second wave low. That's despite the economy having only having partially reopened - shops are no longer closed, but restaurants and bars are only able to operate outdoors.

This latest upturn in the data partly just tells us that businesses and consumers are becoming more adept at living with restrictions. First-quarter GDP is likely to be considerably ‘less bad’ than first feared. But it also reflects growing confidence in the durability of the recovery. For instance, consumer confidence has surged over the past couple of months, helping March retail sales to exceed pre-virus levels even before shops had reopened.

UK data has begun to outperform last summer's highs

Covid-19 has continued to recede in the UK

Of course, whether or not this optimism persists depends on what happens with Covid-19, though for the time being things are looking positive.

New cases have continued to fall despite school reopenings in early March and the more recent lifting of restrictions. Encouragingly, recently detected new variants of the virus from overseas have failed to gain a foothold so far – and remember the UK does considerably more genomic sequencing of the virus than any other country (the process that tracks mutations).

Admittedly, the pace of vaccinations has been less exciting over recent weeks. And it’s hard to gauge how quickly the programme will move through the under-40s, partly it seems due to a lack of clarity on Astrazeneca deliveries. However, there's no reason to doubt that all adults will have been offered their first dose by the end of July, as the government has promised.

This positive virus situation implies that the next step of the reopening will go ahead, with indoor dining/mixing allowed from 17 May. We expect this to translate into roughly 5% GDP growth through the second quarter, and we think the UK economy won’t be far off pre-virus levels by the end of the year – though that’s partly because vaccine/Covid testing is now being included in the GDP figures.

Scottish Independence is back in the spotlight

Beyond Covid-19 and looking to 2022, there are three stories that are worth watching.

Firstly, unsurprisingly, Brexit will continue to weigh on the UK recovery to some extent. While trade flows have partially recovered since January’s hit, it’s clear that some firms are still struggling under the burden of new paperwork. Don’t forget that so far the UK government hasn’t actually introduced the bulk of Brexit-related checks/paperwork – that will happen at the start of 2022, which could introduce further challenges for UK firms.

Secondly, attention at the Bank of England is turning towards future tightening, and it’s becoming increasingly clear that this process – likely to start in 2023 – will involve some balance sheet reduction (more on this in the central bank article of our monthly).

Finally, the Scottish Independence story has come back to the fore amid Parliamentary elections in the country. While the Scottish National Party is likely to remain in power, either as a majority or some kind of coalition agreement, the road to another referendum is likely to be a long one. Prime Minister, Boris Johnson’s government is poised to reject any future request for a second vote on independence, though the issue may well end up in the courts. For now, the polls are back to 50:50 on the issue, though many commentators suspect that repeated rejections of new referendums from London may only succeed in boosting support for independence further.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

UKDownload

Download article

6 May 2021

Someone left the cake out in the rain… This bundle contains 12 Articles