UK Chancellor’s medium-term challenges remain despite near-term boost

- 15 March 2023

- United Kingdom

Lower energy prices have allowed the Chancellor to make a few headline policy changes. But with little-to-no headroom against his fiscal goals – and key question marks over how previously-announced spending restraint will be achieved – the Treasury's challenges have far from disappeared

The Chancellor's near-term boost doesn't remove medium-term challenges

The UK Chancellor Jeremy Hunt was able to launch his Spring Budget against a more buoyant backdrop than he – and the independent forecasting body – had projected back at his crisis Budget in November. Lower energy prices and calmer inflation forecasts for this year have lowered borrowing projections in the next fiscal year by roughly £30bn, and the Chancellor has spent roughly three-quarters of that on targeted interventions to boost labour supply and investment, amongst other things.

But more importantly perhaps, the medium-term constraints on the Chancellor have not gone away. The Office for Budget Responsibility estimates that his 'headroom' against the government’s main fiscal goal – to see debt fall as a percentage of GDP across the medium-term – is just £6.5bn.

That’s very small by historical standards, and indeed the fact that it’s so narrow is in part because the OBR has revised down its previously optimistic assumptions for medium-term growth, from 2.7% to 2.1% in the case of 2026. Medium-term inflation is higher too, in part because of less pessimism about the near-term recession outlook. Both changes serve to increase borrowing in isolation later this decade.

It's also probably within the margin of forecasting error, and the extreme moves in markets this week are a reminder that things can change quickly. This particular set of forecasts is premised on market prices from early-mid February, and against a more stressed market backdrop, we suspect the forecasted headroom would be squeezed further had the numbers been crunched again on today’s prices (lower bond yields would be offset by increased growth concerns).

The extreme moves in markets this week are a reminder that things can change quickly

Beyond the forecasts themselves, it’s worth remembering that the government’s fiscal goal is met in large part due to hefty public sector spending restraint across the medium-term announced last November. Over time the Chancellor will, in theory, be under pressure to put more details on these plans. In general, we think plans for public sector day-to-day spending restraint will be tricky to achieve given budgets have already been heavily squeezed over recent years. Last week’s announcement on curbing the High Speed Two rail project is a reminder that trimming Public Sector Net Investment plans is likely to be the path of least resistance, at least politically, in keeping borrowing projections contained.

In short, the Chancellor’s room for manoeuvre around his fiscal goals is likely to stay limited. The fact that some of his key announcements today – including on capital allowances designed to boost investment – are initially just temporary, highlights the challenges he faces in persuading the OBR that his goals will be met across the medium term.

The Bank of England impact

On paper, the changes to the Energy Price Guarantee are the most consequential for the Bank of England, in so much as it changes the outlook for inflation.

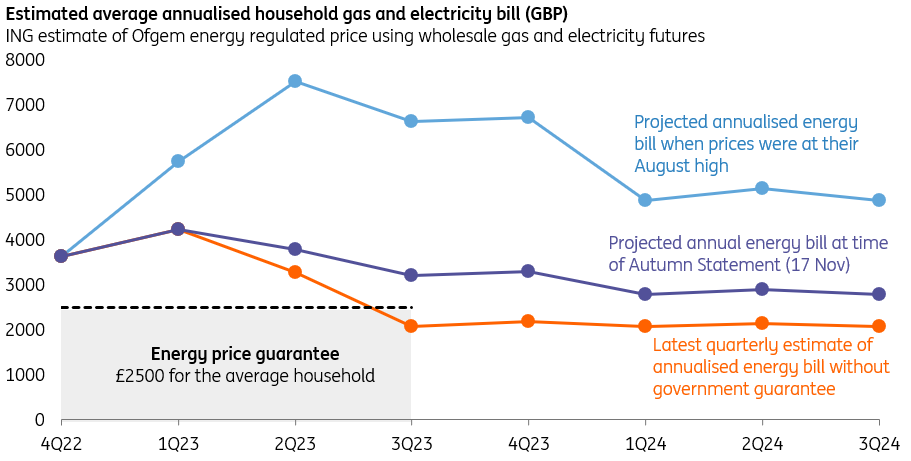

The government’s decision to cap the average household energy bill at £2,500 (annualised) in the second quarter, as opposed to £3,000, will cost roughly £3bn next fiscal year. But the scheme is still set to cost a small fraction of what it had been expected to cost at inception last summer. Lower wholesale energy prices mean that the government will end the scheme in the third quarter, and household bills will return to £2,000-2,100 on an annualised basis, based on the latest market pricing and the regulator Ofgem’s price-setting methodology.

Compared to a scenario whereby the government fixed the average bill at £3,000 for one year as had been envisaged back in November, headline inflation is likely to be roughly one percentage point lower across the remainder of 2022 by our reckoning. Indeed it’s likely to end the year at 2%, on our current forecasts.

UK energy bills are likely to fall by the summer

While that is welcome news for the BoE, the reality is it had already accounted for the fact that wholesale gas prices have collapsed, and its most recent forecasts assumed that government support would end in the third quarter. While these hadn’t factored in the cancellation of the planned increase in bills from April-June, there should be no difference to the inflation projections from the third quarter onwards.

The question of whether the BoE will follow through with a 25bp hike next week depends much more heavily on the situation in the banking sector. While the feedthrough to the UK is still unclear, beyond global moves in asset prices, the BoE has made it clear that the bar to pausing rate hikes is now fairly low – certainly lower than the Fed and ECB have recently been indicating. The chances of 'no change' are much higher than they were last week.

Will the Budget fix the UK’s labour supply woes?

The UK has been one of few – and perhaps the only – country that has seen economic inactivity rates persistently increase since the Covid-19 pandemic. That refers to working age people that are neither in employment or actively seeking it. In response, the Chancellor has various plans – some more significant than others – to try and address the root causes.

First: early retirement. The data are mixed on exactly how significant this is in driving up inactivity. The labour market data suggest it’s been relatively small, though an ONS survey last year suggested retirement accounted for 25% of over-50s that left the jobs market throughout the pandemic period. Either way, the Chancellor has announced large increases to pension allowances in a bid to address this, though given this change only makes a material difference to the highest earners, it’s unlikely to make a huge difference to overall participation rates (with the possible exception of the NHS, which the policy is partially aimed at).

Second, illness, and here the data are much clearer on the impact this has had on inactivity – and indeed long-term sickness rates are still rising as of the latest figures. The Chancellor has announced some changes to disability benefit processes amongst other things. But with NHS treatment waiting lists generally expected to continue rising, this is likely to remain a key challenge for the labour market for some time.

Flexible working has helped lower female inactivity over recent years

Finally, childcare, and this is where the Chancellor’s decision may have more impact. Children over nine months old will receive up to 30 hours of free childcare (currently this only applies when a child is over three years old). Expensive childcare is widely viewed as holding back participation, and these measures should help build on progress through the pandemic in helping female workers back to the jobs market. Female inactivity has decreased over recent years, which as the chart above shows, is heavily linked to fewer women of working age citing family care duties. This trend accelerated during the pandemic when flexible working became more prevalent.

Overall, it’s worth remembering these measures are a medium-term story. And in the short-term, worker shortages are likely to remain an issue for firms, which suggests both wage growth and core services inflation will be fairly slow to fall. For the Bank of England, and putting the uncertainty surrounding the banking sector temporarily to one side, this would suggest less urgency to cut Bank Rate from current levels.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more