Turkey: Growing risks to the outlook

- 22 March 2022

- FX Turkey

Following the announcement of measures to support the lira last year, relative stability has returned to Turkish financial markets. Policymakers maintain hopes of boosting exports to achieve FX and price stability. However, risks are on the rise

'Liraisation' strategy in play

The Central Bank of Turkey (CBT) has increasingly focused on a new policy approach – ‘liraisation’. This is built on three pillars: new financial products, collateral diversification, and liquidity measures. While “liraisation” as a term refers to de-dollarisation in the financial system, the new and reusing of financial products along with other complementary measures seem to be at the core of policy.

In this regard, we have seen a series of measures to support local residents' savings in TRY by bolstering yields on a range of Turkish assets and decreasing local residents' demand for FX.

The key instrument that is expected to contribute to liraisation is the FX-protected deposit scheme and involves:

- FX-indexed deposits to reduce demand for a switch by TRY deposit holders to FX deposits.

- Interest income incentives to convert FX deposits into TRY time deposits protected against FX risk.

This instrument introduced on 20 December was extended to include firms from 11 January, while providing a tax exemption to companies that participated until 25 February.

The scheme was also extended to Turkish citizens living abroad to repatriate their savings to Turkey. This is a practice that was introduced in the 1980s and meant that total savings held at the CBT, mainly coming from Germany, reached roughly US$18-19bn in 2004. However, the CBT gradually reduced its reliance on these savings, which stood at less than $0.3bn as of October 2021. With the latest move, the policymakers have intentions to tap this source again.

Additionally, the CBT further extended these measures to companies that are established abroad and in which Turkish citizens (living abroad) have shares. The CBT will determine the eligibility of these companies. Whether it is attractive for non-resident companies has yet to be seen, though it can be supportive for the CBT reserves in the near term.

Finally, the government also granted the CBT the authority to extend previously one-time interest income incentives for the conversion of FX deposits into TRY time deposits and allowed the shortening of the minimum maturity required to participate from six months to three months for corporates.

To facilitate the take-up of these instruments and the involvement of banks in the conversion of regular deposits into these new instruments, the CBT has also introduced some incentives for banks, including lower commissions and required reserves within a time frame.

According to the latest figures from the Banking Regulation and Supervision Agency (BRSA) as of 14 March, the total size of the FX protected deposits is TRY 557 billion (roughly US$38bn). The BRSA does not provide a breakdown, though previous communication hints that the conversion from FX deposits has been the primary source (perhaps 56%) while the rest is attributable to FX-linked TRY deposits.

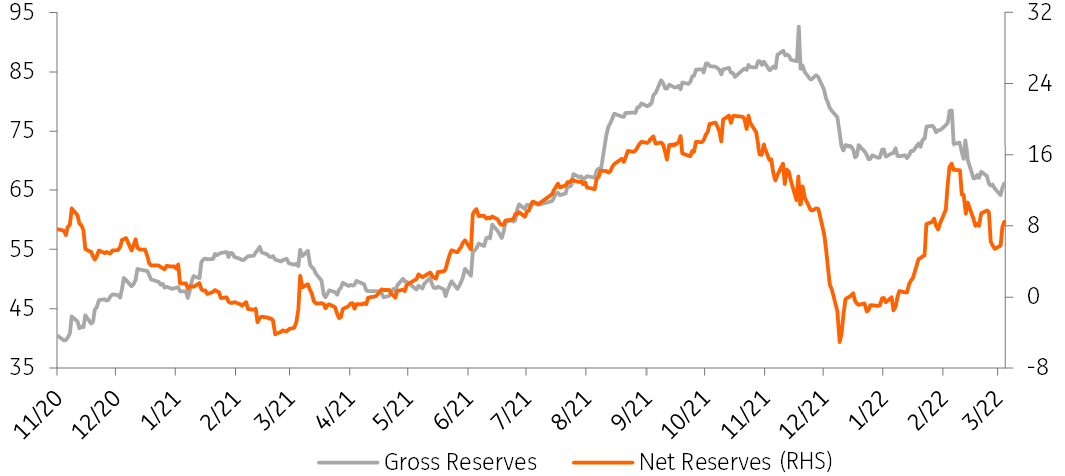

FX reserves have improved

The CBT's reserve position has improved since the start of the year. Accordingly, its net FX position excluding swaps, which declined by $19.6bn in December, improved by $14.2bn since the start of the year (as of 25 February). However, recent geopolitical developments signal some pressures on reserves as we see a decline in net and gross reserves according to more recent data.

The improvement since the beginning of this year reflects not only the increase in its FX purchases related to conversions to the FX-protected scheme (more than $20bn) but also FX purchases related to exporters' FX sale requirements (there's no official data for the time being). On the flip side, selling FX to SEEs that reached an all-time high in February and the decline in banks' swap stock with the CBT are the other factors that impacted reserve developments.

Assuming that the FX-deposit scheme and other CBT efforts will help currency stability in the period ahead, we should also have a look at the key variables that can create further challenges for the sustainability of the current policy framework. Two of the most important variables are inflation and the current account.

CBT FX position on its balance sheet (US$bn)

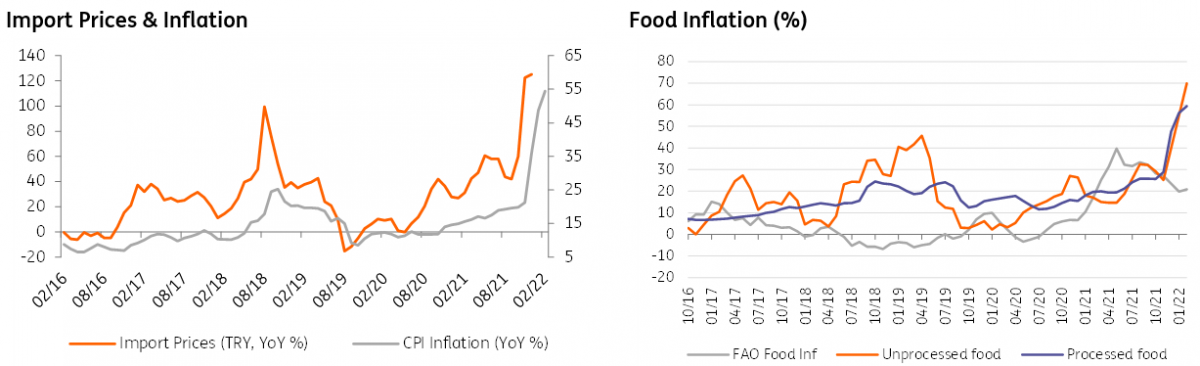

Inflation is on the rise

Annual CPI inflation has maintained a rapid rise since last October and has reached 54.4% – the highest in the last two decades. Inflation in the last four months, on the other hand, stood at 36.9%, reflecting the impact of worsening inflation expectations, the pass-through from currency weakness in the last quarter of 2021 – attributable to deep monetary easing delivered by the CBT, along with large administrative price hikes. Following these developments, trend inflation that had been at high single digits in the past is now estimated to be around 20%, confirming a need for policy reversal towards a more restrictive stance.

On the other hand, market forecasts for year-end inflation rose to 40.5% in March, while 12-month and 24-month expectations stand at 26.4% and 17.0% respectively. These show that inflation expectations are high and unanchored given that the current policy framework does not directly address disinflation.

It is not only rising inflation expectations and the FX pass-through, but also other demand-pull and cost-push factors – including rapid uptrend in global commodity prices – which have increased inflation significantly. Given the broad-based deterioration in price dynamics, risks continue to lie significantly on the upside.

Closing the section on prices, higher inflation, leading to even deeper negative real rates, should cloud the currency outlook and raises significant challenges to the current policy framework.

Import prices, food prices, CPI... all on the rise

Current account deficit expands rapidly

The 12-month rolling current account (c/a) balance showed a significant improvement last year. Driving that was:

- A narrower goods deficit despite surging energy imports, thanks to an improved gold balance and rapid export growth.

- The sharp recovery in the services balance on the back of tourism and transportation revenues. Accordingly, the deficit narrowed to $-14.9bn at the end of 2021, translating into 1.9% of GDP.

However, the c/a deficit recorded a sharp expansion in January with the worst monthly figure since the end of 2017. And the deficit widened back out to above $20bn on a 12-month rolling basis mainly on the back of a more than quadrupled (over the same month of 2021) energy deficit and a decline in core trade surplus.

Given that negative real rates reduce the incentive to save, and oil prices are on the rise, the external balance will remain under pressure in the near term. The outlook for the whole year will be determined by tourism revenues and oil. The risk of oil prices remaining higher for longer given the ongoing conflict between Russia and Ukraine will be a negative, while the slowdown in economic activity and weaker core imports can be a limiting factor.

Rising import costs will widen the current account deficit

Oil prices and net energy imports

Growing risks to the current policy framework

As long as the government can limit the inflation uptrend as well as the widening of the external deficit, the current policy framework can be sustained for longer. However, as we discuss above, challenges are growing on both the inflationary and external sides. Furthermore, the outlook for these two variables is concerning:

1) Acceleration in lending:

Looking at the latest data, we see:

- Signals of re-acceleration in TRY corporate lending momentum with the Credit Guarantee Fund (CGF).

- Credit card momentum remains strong showing the appetite for consumption amid rapidly deteriorating inflation expectations and a wave of price hikes.

- A deceleration in general purpose loans

Normally, the CBT communication is that “balanced growth in commercial and retail loans is a requirement for price stability and financial stability”. This implies selective lending on the commercial side and a restrained retail lending expansion. However, further acceleration in TRY corporate loans within the CGF package can undermine the selective growth strategy with a stronger and wider stimulus than anticipated earlier.

One major risk attributable to the acceleration in lending is that it can feed into local FX demand and increase inflationary pressures via accelerating domestic demand and a weakening TRY. It can also pressure the current account balance if we see real lending growth.

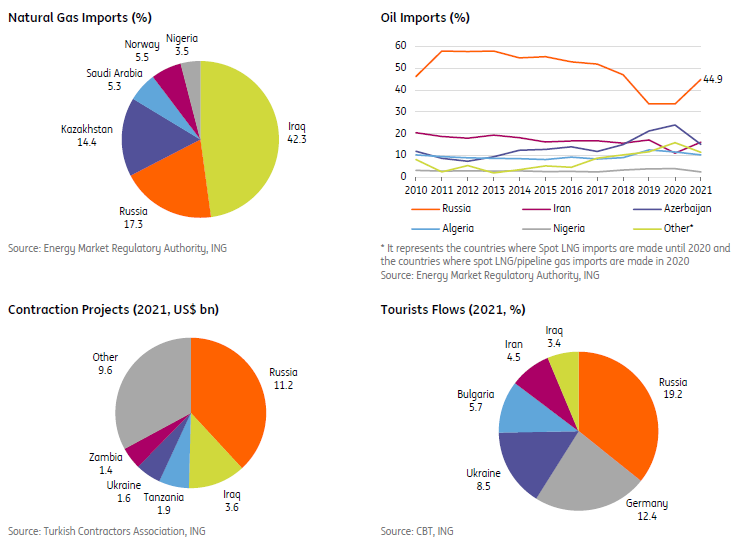

2) Geopolitical Issues:

The ongoing conflict between Russia and Ukraine can pose significant risks to Turkey via:

- Trade: While trade with Ukraine is relatively low and balanced, Russian trade is large and more concentrated given Russia’s high share of energy in Turkish imports. According to 2021 data, Russia is the main supplier of Turkey’s 44.9% of natural gas imports and 17.3% of oil imports. Additionally, Turkey relies on agricultural imports from both countries with a significant share of wheat in the total.

- Tourism: Tourists from Russia and Ukraine constitute 19.2% and 8.5% of the total, respectively, based on 2021 data.

- Construction projects: Total volume of projects secured by Turkish contractors from Russia in 2021 is at $11.2bn ($4.6bn in 2020), translating into 38.2% of the total (30.1% in 2020). The deteriorating outlook for Russia is likely to weigh on the initiation of new large projects.

- Pressure on oil prices: The rise in energy imports was the main driver of the c/a deficit, while 12-month trailing energy imports are on an uptrend in recent months to $56.9bn in January from $27.1bn in February 2021. The latest spike in energy prices should add to Turkey’s fragility.

- Higher risk premium: Turkey’s five-year CDS premium has spiked over recent weeks, which should further increase external borrowing costs for Turkey in the period ahead.

This backdrop supports views for increasing inflationary problems and widening external imbalances. Despite the acknowledgement of geopolitical risks in the latest Monetary Policy Committee statement, the CBT’s general assessment for the macro outlook has remained broadly unchanged. For the future course of inflation, the bank continues to be quite optimistic, restating that it sees the start of the disinflation process on the back of measures taken by the policymakers along with supportive base effects and “the resolution of the ongoing regional conflict”. For the current account, it dropped the expectation of a surplus this year, though maintained its emphasis on the importance of a sustainable current account balance for price stability.

3) Shift in global central bank policies:

As of January, and on a 12-month rolling basis, $18.8bn reserve accumulation was realised. Helping this were $8.9bn in net errors and omissions, relatively higher capital inflows at $30.2bn, and a narrowing in the c/a deficit. These numbers still show a challenging picture for external financing given the reliance on the contribution from the CBT’s swap deals at roughly $5.0bn and the IMF’s SDR allocation at $6.3bn for Turkey. However, we saw a strong long-term debt rollover rate for corporates at 134% (vs 138% in January alone), while the same ratio for banks stood at 95% (106% in January). Trade credits have also markedly expanded at $13.6bn versus a slight contraction over the same month of 2021.

For the coming months, the expected tightening of global central bank policies can increase challenges for Turkey given the still large external financing requirements. Given this backdrop, focus on external financing will likely shift to roll-overs rather than portfolio flows.

Turkey is dependent on Russian gas, tourists and construction projects

Adjustments in the deposit scheme likely, depending on market developments

In conclusion, there are growing risks to the currency outlook, including:

- An acceleration in lending that can feed into local FX demand.

- The conflict between Russia and Ukraine leading to further inflationary challenges via higher food and energy prices.

- The ongoing tightening of global central bank policies while external financing requirements are still high.

However, while acknowledging these challenges driven by recent regional developments, the CBT opted to remain mute again in March and reiterated that it would continue to use all available instruments decisively “within the framework of a liraisation strategy”. So, it should be a signal that the current policy framework will continue and hence the durability, as well as the attractiveness of the FX-protected deposit scheme, will be key in the period ahead. Accordingly, we can see some adjustments depending on market developments in the recently introduced FX-protected deposit scheme to reduce demand for a switch by TRY deposit holders to FX deposits, and incentivise for conversion of FX deposits into TRY time deposits.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more