Turkey: What the elections mean for markets and the economy

- 25 June 2018

- Turkey

Based on the unofficial results, President Recep Tayyip Erdogan has won the presidential election in the first round, while the AKP/MHP alliance has gained a parliamentary majority. Market movements will now likely be determined by how the government manages the economy and the specific policy mix

Erdogan and People’s Alliance won the elections

Turkey held its first dual parliamentary and presidential elections on Sunday. This was originally scheduled for 3 November 2019 but was brought forward by President Recep Tayyip Erdoğan in late April, despite the government's insistence that the general elections would take place at the scheduled time. Following the approval of constitutional changes in April 2017 referendum, the president is both the head of state and head of the Turkish government and does not need parliament to form a government.

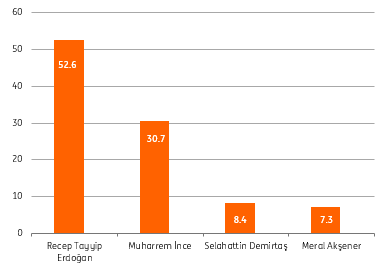

Presidential Elections (%)

Five leading parties participated: the Justice and Development Party (AKP), the Republican People's Party (CHP), the Nationalist Movement Party (MHP), Iyi Party (IYI) and the Peoples' Democratic Party (HDP). In recent surveys, it was not clear whether President Erdogan would get the 50%+1 support to win outright in the first round, while the parliamentary vote was also expected to be close, with the People’s Alliance (AKP and MHP) uncertain of securing a simple majority of 301 of the 600 seats up for grabs.

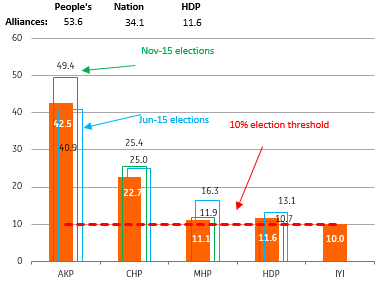

Parliamentary Elections (%)

Out of 59.4 million eligible voters (including those residing abroad), the participation rate stood at 86.7%, above the rate realised in the last three general elections since 2011. The unofficial results show that President Erdogan had 52.6% of the vote, comfortably ahead of Muharrem Ince at 30.7%. Parliamentary elections, on the other hand, show a decline in AKP support to 42.5% vs 49.4% at elections in November 2015 and close to the level seen at the June 2015 elections. However, the People’s Alliance secured 53.6% of the vote with a better-than-expected performance from the junior member, MHP, at 11.1%. Nation Alliance had 34.1% of the total vote while CHP had 22.7%- below the 25% support seen in the two elections back in 2015. The newly established Iyi Party (formed by those who left MHP) recorded 10.0%, while HDP, not a member of an alliance (and hence subject to the 10% threshold), once again, exceeded this level with 11.6%.

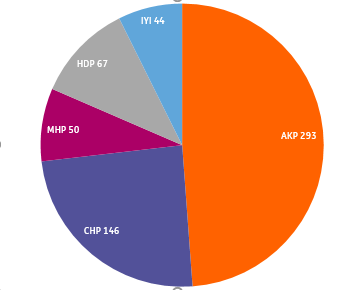

Seat Distribution (out of 600)

Seat distribution

AKP won 293 seats, below the simple majority of 300- and the 317 seats in elections back in November 2015- despite the number of MPs increasing from the previous 550 to 600. However, with MHP’s 50, the People’s Alliance seats surpassed 340, while Nation Alliance had 190 seats, 146 of which belong to CHP. IYI had 44 and HDP’s seats stood at 67 vs 59 in November 2015.

Controlling a majority of parliamentary seats is still important despite the constitutional amendments approved in the April 2017 referendum, which give the power of issuing decrees to the presidency. These amendments also allow parliament to overcome a presidential veto if it adopts the same bill with an absolute majority. While it's not a decisive blow, without a simple majority in parliament, the AKP cannot control the legislature unless it has MHP support. So, the election outcome will make AKP and President Erdoğan more dependent on the MHP in law-making and parliamentary issues.

On the flip side, the current (revised) constitution is designed for these sorts of irregularities and allows for the proper functioning of executive authority without significant intervention from parliament. Therefore, we don't expect calls for another election.

Markets in the period ahead

In previous elections, AKP/Erdogan victories were followed by positive market reactions, even rallies in some cases due to a perceived end of political uncertainty. Early price movements following the announcement of unofficial results show some improvement in sentiment with strength in the currency.

However, the policy outlook in the aftermath of elections matters for the markets given concerns about President Erdogan’s recent statements that he intends to take more responsibility for monetary policy after the elections. Also, the election outcome suggests a decline in AKP support compared to previous general elections, which may raise concern in the party about the forthcoming local elections in March 2019. Further market movements will likely be determined by the new management team running the economy and the policy mix. A continued loose fiscal stance to revive growth may weigh on markets due to already elevated inflation prospects and surging government bond yields.

Economic outlook

Pressure on the currency has intensified from early March, not only because of increasing macro vulnerabilities, but also a far more challenging external environment than before. Geopolitical/event risks have increased and there is pressure on emerging market assets amid growing expectations for US interest rate increases. There are also questions about the global growth path and worries about trade. In other words, a strong US dollar rally- which has sparked steep falls in EM assets- has been another driver for volatility in local financial markets.

Macro vulnerabilities have been at the forefront

Growth last year represented the strongest performance among major emerging market economies, helped by a benign global backdrop and strong stimulus measures. In the last quarter of 2017, strength came entirely from domestic demand. Accordingly, growing concerns about an overheated economy with adverse effects on inflation, an already imbalanced external position and pressure on the fiscal accounts have significantly worsened Turkey’s macro risk perceptions:

- On the inflation side, recent data shows some deterioration, likely further weighing on the headline rate and on inflation expectations. A rise in import prices on the back of currency depreciation and upward pressure on energy prices are the major reasons for the ongoing uptrend. Looking ahead, we expect inflation to continue to rise with the plunge in currency, spike in oil prices and unsupportive base effects, exceeding 14% in summer. We expect it to change direction thereafter until the end of this year, though upside risks should remain in the near-term.

Inflation Trend (%)

External balances

- The current account balance has been on a widening track, with the 12-month rolling figure in April 2018 reaching its highest level since mid-2013. This was due to an expansion in the trade deficit, with imports accelerating on the back of rising core imports (though these lost momentum lately) and higher gold and energy prices. The current account widened despite an improvement in services income thanks to a sharp recovery in net tourism revenues. The ongoing loss of momentum in the economy and weaker TRY will likely help the trade balance to recover, suggesting that we may have reached a peak for the external deficit. On the other hand, the outlook for capital flows has weakened since the last quarter of 2017 to some extent, showing the impact of a more challenging global backdrop and volatility in the global financial markets as well as deterioration in the macro risk perception for Turkey. This leaves little room for policy complacency. Though the latest April 2018 data points to a recovery from deposit flows, it is not likely to be sustainable for very long.

- The government has stepped up its fiscal stimulus for 2018 by introducing a new set of incentives, with a focus on stimulating investments. In addition to its already loose fiscal stance, the government has proposed a recent spending package amounting to TRY22-24 billion as well as bonus payments to pensioners and a restructuring of the private sector debt to the state. All of this has weighed on markets and added to concerns about the inflation outlook. The total impact of election spending is calculated at 0.7-0.8% of GDP. The budget performance in the first five months of this year reveals strong revenues driven by surging tax income, while primary spending also continued to expand, with skyrocketing capital spending, despite single-digit growth in currents transfers. The government’s balance sheet has been one of the strengths of the Turkish economy with an average 1.3% budget deficit-to-GDP ratio since the global crisis, while the primary balance has almost always been in surplus. But loosening fiscal policy has raised concern that public debt- currently low at under 30% of GDP- would return to an upward path. Whether the policymakers maintain a pro-growth bias after the elections will determine the fiscal outlook in our view.

Economy on course for a slowdown: Risk of a hard landing?

GDP grew at another rapid pace of 7.4% in 1Q18 while domestic demand was still the main driver with a 10.9ppt contribution to the quarterly performance, marking an increase over the previous quarter at 10.4ppt. Private consumption expanded by 11% year on year and added 6.7ppt to the headline, while fixed investments were surprisingly strong, lifting the quarterly performance by 2.8ppt, driven by construction and machinery investments.

However, the recent data (PMI at the lowest level since the global crisis, decline in confidence indicators, softening IP, auto, white goods, and house sales etc) also indicate some further deceleration in 2Q and show the effects of volatility in financial markets. The central bank hike of 500 basis points will be reflected in the wider economy in the coming quarters. In other words, given the impact of TRY depreciation on the corporate sector's balance sheet (with repercussions for investment demand) and the effect of rising borrowing costs on credit demand, the rebalancing that started this year will accelerate in the remainder of 2018. But whether the Turkish economy will face a hard landing is a major issue in the period ahead. To avoid a hard landing, the key issues in our view are:

Fiscal policy: Policymakers, including Deputy Prime Minister Mehmet Simsek and Minister of Finance Naci Agbal, have increasingly pointed to tighter fiscal policy after the elections. They have suggested that the election package could be easily paid for, as the Ministry of Finance has already worked on possible actions/scenarios for fiscal tightening.

A one-off round of restructuring of the private and public sector debt to the state would help the fiscal balance, likely keeping the deficit under control this year. But a rationalisation of public spending and adherence to fiscal discipline would be a strong positive signal.

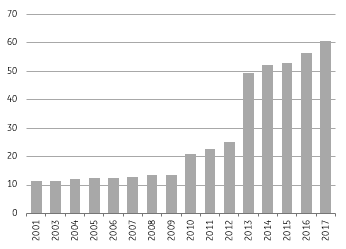

The new government should divert its focus to the off-balance sheet liabilities as well, since Turkey has one of the highest cumulative public-private partnership (PPP) investments in Europe, according to the IMF. The size and implementation rate of the PPP portfolio has accelerated during the last decade, exceeding $60 billion at end-2017 with 7.1% of GDP. As a number of PPP project components are also in FX terms, the Treasury is exposed to currency risks through some of these contracts. So recent financial volatility should be a source of fiscal risk, given the deterioration in growth prospects and the extent of adjustment in interest rates and the currency. Accordingly, transparency on the likely burden from contingent liabilities would be a step in the right direction.

Cumulative Size of PPPs (USD bn)

Monetary policy: The CBT has continued its strategy of safeguarding price stability with strong hikes in May and June, signalling that policymakers such as Mehmet Simsek remain independent. According to recent news on the restructuring of the administration, Erdogan's government doesn't currently have any intention of changing the current CBT law or mandate. In fact, the pressure for lower interest rates has significantly weighed on the inflation outlook with a deterioration in inflation expectations. Accordingly, the new government should address the issue and accept central bank independence (that was the major pillar, along with an inflation-targeting monetary policy framework, to control inflation and support rapid growth after the 2001 financial crisis). Strengthening CBT independence with a sole focus on inflation and financial stability would be key for investors.

Real Policy Rate (%)

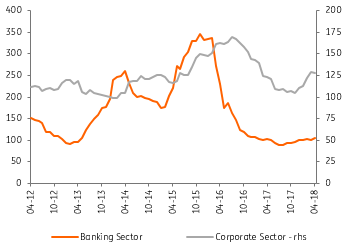

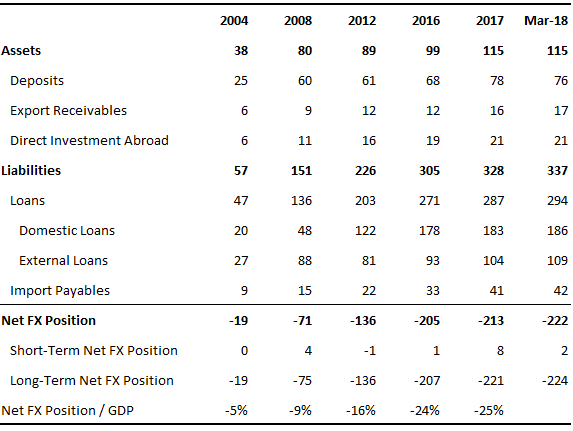

Corporate sector & banks: Adverse spillovers from excessive TRY weakness on corporate balance sheets should be addressed quickly. The short FX position of the nonfinancial sector, standing at $222 billion (more than 25% of GDP) as of March 2018, has been a source of vulnerability for the Turkish economy, though this figure does not fully reflect the natural and financial hedges.

Corporate Sector FX Position (USD bn)

Early this year, the government announced a legislative change that aimed to mitigate high FX-based risks of nearly 26,000 SMEs. This was put into force at the beginning of May and also introduced a threshold of $15 million for total FX liabilities.

According to the authorities, around 20-25% of the corporate sector’s open position is held by SMEs. For the remainder, further regulations to reduce large corporates’ currency risk should contribute to financial stability. To this end, hardening FX borrowing for those not generating FX revenues should be a step in the right direction. It should also be noted that the level of non-performing loans is expected to rise in the coming period with downside pressures on the growth outlook (despite the lack of a meaningful correlation with TRY depreciation or surging lending rates). In fact, increasing loan-restructuring demand- 3.6% of the lending book at end-2017- is a stress signal.

A deterioration in corporate sector balance sheets should be negative for the lending demand of the banking sector. Another likely force of deleveraging for banks could be external funding. Banks have reduced short-term external debt since end-2014 from more than $92 billion to $75.8 billion in Mar-18 (though this increased in Apr-18 to $78.3 billion). So, short-term refinancing risk remains high, although there are sufficient FX liquid resources to cover obligations, with the inclusion of banking sector holdings at the CBT (under the framework of the reserve option mechanism) amounting to $30 billion- of which $13.7 billion is in the form of gold. Despite the improving long-term debt rollover ratio in recent months (which is comfortably above the 100% threshold on a 12-month rolling basis as of April 2018) the external funding of banks should be under close scrutiny, as it can trigger a deleveraging cycle.

Short-term external debt (USD bn)

Overall, macro and financial actions by the new government addressing short-term vulnerabilities will be key for the macro performance in the period ahead, while a reviving reform agenda in social, economic and political areas will also be crucial in taking Turkey to a recovery path.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more