Three trends to watch in the US data centre industry

- 25 June

- Energy United States AI

From behind-the-meter power to new data centre hubs and ‘boomtowns’, an AI-era 'makeover' is now reshaping energy, infrastructure and local economies across the US

AI has become a key driver of economic growth in the US, with power constraints emerging as a defining factor shaping how sectors evolve. As AI-driven data centre expansion accelerates, it is reshaping energy demand, infrastructure needs, and local economies.

For instance, data centres are driving energy demand growth at a rate not seen in decades, requiring significantly more power than the grid can deliver in a 12 to 18-month span. Moreover, data centres are driving an infrastructure revolution, requiring significant buildouts necessitating new real estate and fibre networks in remote areas. All this will also affect affordability for the public, putting the topic at the forefront of data centre development.

Against this backdrop, we're closely tracking several key data centre trends in the US. This article explores behind-the-meter power, the rise of ultra-large hubs, and the emergence of data centre ‘boomtowns’. A follow-up piece will examine modular solutions and evolving supply chains.

1. How data centres’ own power can be a new grid asset – and more than a stopgap

Power availability is now a first‑order concern for the data centre industry. Grid interconnection for both data centres and new power generation remains slow, often exceeding four-year timelines. Multiple reforms are underway, such as recent action by the Federal Energy Regulatory Commission (FERC) to accelerate large power consumer interconnection, but the effects take time to be seen.

As data centres race to bring new capacity online in the next 12-18 months, many are turning to on-site (or ‘behind-the-meter’) power. This means generating and using electricity directly on their premises, bypassing the grid.

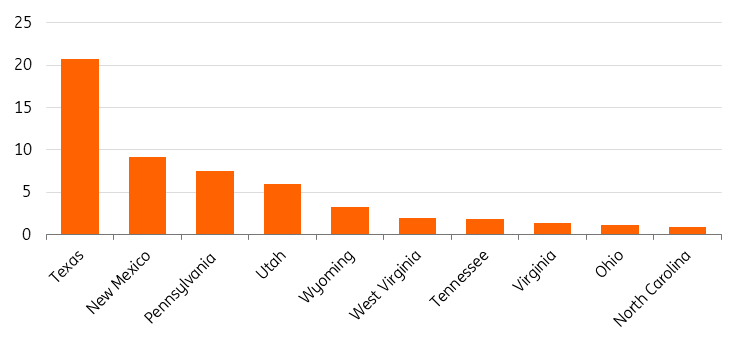

Conservatively, over 55GW of behind‑the‑meter capacity is being planned at US data centres. That is higher than the total installed power capacity in the state of New York. Texas has the most planned on-site capacity, followed by New Mexico and Pennsylvania.

US planned data centre on-site power generation capacity in top 10 states

The US accounts for most of the world’s planned data centre behind-the-meter power capacity. This is driven by a huge project pipeline and cheap gas resources. Indeed, 75% of the planned US onsite power capacity is expected to be from natural gas through turbines, engines, and fuel cells. Renewables could also be a niche alternative, such as Switch's solar and battery-powered Citadel Campus in Nevada.

Most data centres view on-site generation as a ‘bridging solution’

Still, most data centres view on-site generation as a ‘bridging solution.’ In the long term, the majority would still return to relying on grid power. In fact, many data centres are developing behind-the-meter solutions while waiting to be connected to the grid.

An emerging issue today, however, is managing rapid load surges (e.g., over 20MW of surge in 0.25 seconds) thanks to shifts in AI workload-driven data centre design. These surges can be too quick for on-site generators to respond to, and they can put sudden strain on the grid. Another key challenge is how data centres can be seen as grid supporters rather than isolated power users, especially as power prices come under pressure.

Power storage stands out as a solution

For both challenges, power storage stands out as a solution.

Behind-the-meter power can already help smooth out demand spikes. And if combined effectively with utility-scale battery storage, it can give excess power back to the grid, boost overall capacity, and stabilise prices. Furthermore, batteries can help meet instant load surges, enhancing on-site generator performance. That is why we expect more battery systems to be added to data centres, not only alongside renewables, but also with gas-fired power generation.

Ultimately, data centres must adopt strategies that support local energy systems. That essentially means supporting consumers who rely on power from the grid. Battery storage onsite at data centres, as discussed above, will be an asset to the grid. Beyond that, participating in virtual power plant (VPP) programmes can make power demand from the grid more flexible (e.g. Google’s deal with Voltus).

All these will become increasingly important as data centres are more vertically integrated with the energy sector (e.g. Google’s acquiring of Intersect’s digital power business). Smart data centre energy strategies, combined with evolving grid policies, will enable genuine energy transformation.

2. The rise of new ultra‑large hubs calls for system efficiency

Data centres, especially those in the US, are large in size. Now, though, they are growing even larger, as demand from AI and cloud workloads continues to surge. Hyperscalers are moving from gigawatt factories to multi-gigawatt campuses. Colocation providers are shifting away from traditional enterprise models toward higher‑capacity deals with anchor customers.

Traditionally, data centres are spatially concentrated to take advantage of shared infrastructure and customer proximity. Now, though, an increasing number of larger data centres are in development, meaning concentration is not going away. In North America, approximately 80% of the data centres in the pipeline are expected to be in clusters, both existing and new.

Geographical distribution of data centres in the US

Hyperscalers and operators are deepening the expansion of existing clusters, such as Northern Virginia and major Texas metropolitan areas, including Dallas and San Antonio.

Meanwhile, new hubs are forming. Rising land, power, and interconnection constraints in existing clusters are catalysing the emergence of new hubs such as West Texas and Ohio. Infrastructure in these regions is quickly developing. Digital infrastructure company US Signal, for instance, is constructing over 1,000 miles of new fibre networks across Ohio and Indiana. That length is enough to get you from New York City to Tampa, Florida.

For data centres, efficiency is key. This is true at the asset level, but it becomes more important at the system level – at clusters. Achieving system efficiency requires a holistic approach. Coordinated planning of fibre networks, grid connectivity, and general resource utilisation will make these hubs more efficient at their formation stage.

Achieving system efficiency needs a holistic approach

For instance, new regional hubs serve both latency‑sensitive AI inference and location‑agnostic AI training. So, coordinated planning of fibre networks, grid connectivity, and general resource utilisation will make these hubs more efficient at their formation.

Another key factor of system efficiency is local support. Data centre development can inevitably create pressure points for communities. For instance, in Ohio, now a major data centre hub, retail electricity prices rose 22% year over year. In some other cases, local communities have had concerns about data centre water usage and pollution. As local sentiment becomes a bigger consideration for project development, data centres need to demonstrate they can be part of the solution. Effective strategies include engaging with communities early, identifying their needs, and reflecting them in project plans.

3. How remote data centre boomtowns can keep booming in the long term

But not all data centres will go for clusters. Some have headed to remote towns outside major metropolitan areas, betting that their multi-gigawatt ambition alone can achieve economies of scale.

One example is Abilene in Texas, home to the nearly 300,000-square-foot Stargate facility. The economic benefits from the project have surged: it has created thousands of construction jobs since its launch in mid-2024, while drawing in out-of-town labour. Other boomtowns and communities include New Florence, Missouri; Holly Ridge, Louisiana; and so on.

For these towns, much of the local economic growth now relies on data centres. That has raised questions about how these towns can sustain growth once data centre construction is completed. Studies suggest that for a traditional large data centre, operational job creation potential tends to be less than 10% of that of construction jobs.

We argue, however, that with the right strategies, data centres can meaningfully contribute to the development of local communities.

The key, first and foremost, is to transform construction jobs into skill-oriented on-site asset management jobs. As hyperscalers become larger and more sophisticated, the need for skilled labour to run such data centres could disproportionally grow. With more data centres pursuing behind-the-meter power solutions, there will be extra demand for labour capable of maintaining energy assets.

The second priority is to transition from being a construction hub to becoming part of a broader AI ecosystem. Even at the planning stage, data centres are encouraged to work with local stakeholders to develop a regional AI blueprint. For instance, Microsoft’s hyperscaler buildout in Wisconsin includes partnerships with nearby colleges to support research and development (R&D), train skilled labour, and facilitate AI adoption among local companies, such as Regal Rexnord and Renaissant. By doing this, Microsoft is helping turn parts of Wisconsin into an “AI lab,” with hyperscalers surrounded by educational institutions running dedicated AI programmes.

Data centre boomtowns need to transition from a construction hub to a broader AI ecosystem

This can create high-quality research jobs locally, with spillover benefits for employment in services and hospitality. Data centres would also benefit from working closely with state and local governments to ensure that local communities have affordable housing, power, and other resources.

Conclusion

As AI becomes a megatrend affecting many sectors of the US economy, data centre development increasingly hinges on coordination across the supply chain and with local stakeholders. Power strategy, system-level efficiency and local alignment will increasingly define business success.

Ultimately, local support is a critical ‘social license to operate’. Community trust will be awarded to players who align the interests of data centre developers, tenants, and power suppliers with those of local communities from the start. Data centres that incorporate flexible design, efficient hardware and software, and smart use of water and power – while engaging supply chains and local communities – are more likely to survive the 'boom' period and sustain long-term business continuity.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more