Three Bank of England questions that matter for markets

- 30 October 2017

- United Kingdom

The Bank looks set to hike rates for the first time in 10 years, but who will vote for it and will they signal that more tightening is to come?

Our Bank of England scenarios

Three things to look out for

This week's Bank of England meeting is likely to be both historic and contentious as the Monetary Policy Committee (MPC) looks set to hike rates for the first time in 10 years. But its what comes next that really matters for markets.

We expect the BoE to continue talking up the possibility of further tightening this week, but with uncertainty elevated, demand sluggish and few signs of domestic inflation, we think the Bank will tread carefully. And while policymakers are keen to avoid getting left behind by other central banks (thus limiting further downside for sterling), and to exit emergency mode as the post-Brexit shock dissipates, the BoE will be wary of repeating the ECB's mistake of tightening too early back in 2011.

We wouldn't rule out a second hike next year, but we are still yet to be convinced the BoE will embark on a meaningful tightening cycle. So the Bank of England has a tricky path to tread when it meets this week, and here are the three main signals that we think matter for most for markets...

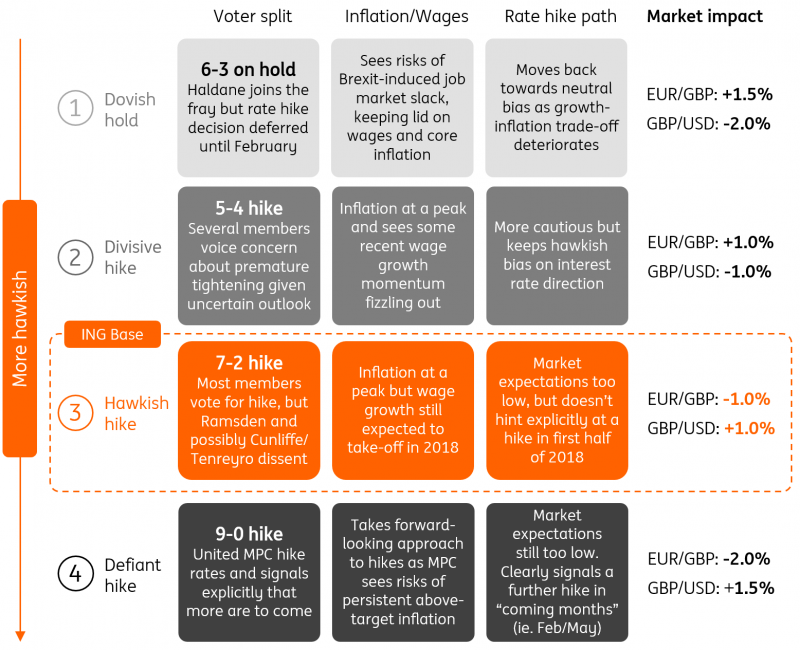

Which members will vote for a hike?

So far this year, two MPC voters, Ian McCafferty and Michael Saunders, have voted for rate hikes. And over the summer, chief economist Andy Haldane seemed close to joining them.

Assuming those three members vote in favour of a hike, it's now a question of how big the "core" group of voters will be. This will almost certainly comprise of Governor Carney and Ben Broadbent, and despite previously being viewed as an "arch-dove", Gertjan Vlieghe's hawkish comments on wage growth back in September mean he's likely to follow suit.

Either a 7-2 or 8-1 vote looks most likely but anything less could expose divisions among the MPC

That makes six, but this could be where the dissent starts. Both Silvana Tenreyro and Deputy Governor Jon Cunliffe have signalled they are in no rush to increase rates - the latter saying the timing of a hike is an "open question". That could be enough for at least one of them to dissent on a rate hike vote, although both do agree to the principle of tighter policy.

But at the far end of the dovish spectrum sits Dave Ramsden, who when asked whether he was in the group looking to tighten policy over the next few months, said: "I was not part of that majority". This makes it pretty likely that he'll vote against a rate hike this time around.

Adding it all together, either a 7-2 or 8-1 vote looks most likely. But anything less could expose divisions amongst the MPC on the need for tighter policy and would signal that further 2018 hikes are far from guaranteed.

| 7-2 |

How we expect the MPC to vote on a rate hike |

Are market rate hike expectations still too low?

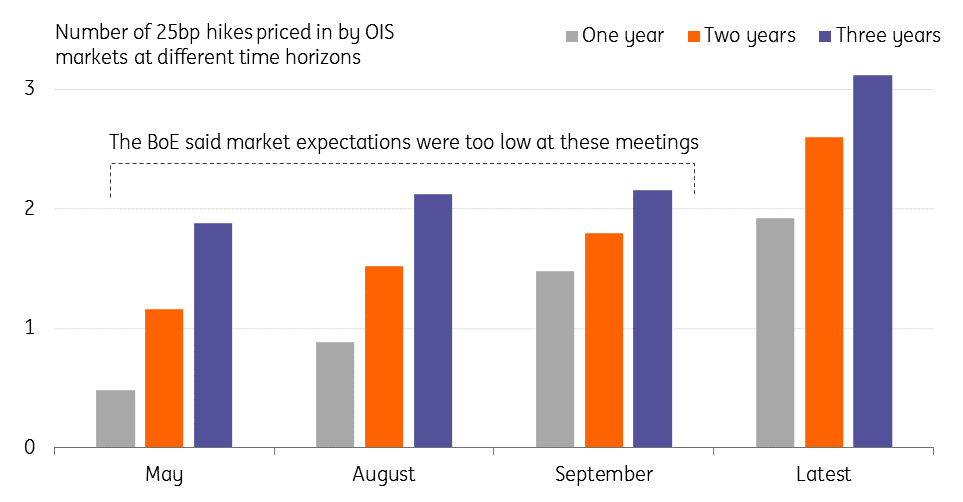

For several meetings now, the BoE has signalled it thinks market's rate hike expectations are too low. But it was not really until the Bank's direct rate hike signal in September that markets really started to take note. As well as virtually pricing in a November hike, the market is now expecting an additional increase by next September.

So does the MPC still think that markets are underestimating future rate rises? The answer is probably yes. That's because, after September next year, markets only expect the Bank to hike once over the subsequent two years. We suspect the Bank would ideally like markets to have slightly more than this priced in, although, given all the various economic and political uncertainties, they may take a little more convincing.

We suspect the Bank would ideally like markets to have slightly more priced in

But before then, the bigger question is whether or not the Bank throws in another explicit hint that rates need to rise further in "coming months". At this stage, we think the MPC will be reluctant to tie its hands too much. While we could potentially get some more positive Brexit news as we head into the new year - the concrete agreement of a transition deal and possibly the initiation of trade talks - there are still plenty of political hurdles and landmines that have to be navigated first. A lot can happen before February.

For sterling, this means we could see an asymmetric reaction to the four scenarios outlined above. Given that short GBP positions have been reversed of late, a more dovish Bank of England could see the pound fall more against the dollar than the euro. But on the flip side, a more hawkish BoE, one where there is a clear hint at another hike early next year, could see GBP rally more against the EUR than USD, because of the ECB's dovish forward guidance.

ue

Market rate hike expectations have risen noticeably

Wage growth - still about to takeoff?

At the heart of the Bank's thinking is an assumption that wage growth will pick-up pace considerably over the next few months. With the unemployment at multi-year lows, the BoE forecasts pay to rise 3% next year.

And there has certainly been some renewed momentum in the pay numbers over the past few months - a key reason why the BoE's Vlieghe turned more hawkish in a speech back in September. As the Bank tries to keep markets aligned to the idea of further gradual rate hikes to come, we suspect the Bank will maintain it's optimistic stance on wage growth when it meets in November.

We may not see wage growth take-off to the extent the Bank is forecasting

However, we are slightly more cautious. The recent pick-up is partly explained by a rise in the national living wage back in April. And going forward, we think that a combination of ongoing Brexit uncertainty, weaker demand, and pressure on costs owing to the weaker pound, mean we may not see wage growth take-off to the extent the Bank is forecasting. There's also the issue of productivity growth, which is still stubbornly low.

It's also possible that much of the labour market resilience we've seen so far this year is down to the surprising economic momentum in the months following the UK referendum - in which case we could see the unemployment rate trough over the next few months if the growth slowdown starts to weigh on the jobs market.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more