THINK Ahead: Wanted! A superhero to save the markets

All good Hollywood bestsellers need a superhero. And frankly, so do financial markets after the week they've just had. Will the Fed come to the rescue, and how long are the tariffs likely to last? James Smith attempts an answer to those questions and more as the team looks ahead to another blockbuster week for the global economy

Wanted! A superhero to save the markets

Who is going to save the US stock market?

I’ll admit, it’s not exactly the making of a Hollywood blockbuster. And if it was, the theme tune would presumably be played by a single, very tiny violin.

Anyway, markets think they know the answer: Jerome Powell. As is so often the case when stocks wobble, investors are shining the proverbial bat signal at the night sky and waiting for their superhero to calm things down. Markets are now pricing upwards of four rate cuts this year, up from a little under three a week ago.

Is that naïve? Whisper it quietly, but the Fed doesn’t really care about stock markets unless it all becomes disorderly and provokes problems in the financial system. That isn’t the place we find ourselves right now. Not yet, anyway.

But that doesn’t mean Powell isn’t watching closely. Remember that tariffs were meant to be a big dollar positive, but as Chris Turner explains, concerns about corporate America have led investors to find safe havens overseas. Markets are – rightly – focusing on what looks like a rapidly deteriorating US economic outlook.

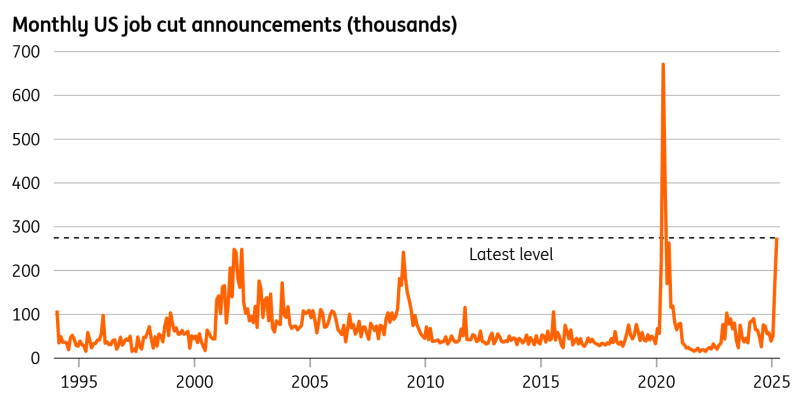

The rise in job cut announcements during March, tracked by Challenger and released this week, was frankly astonishing. It eclipsed anything we saw in the height of the financial crisis or dot-com bubble. For now, that’s all linked to cost-cutting in the federal government and the latest official jobs numbers, hot off the press, look more solid. But tariffs surely only add pressure, as my US colleague James Knightley explained in detail immediately following the announcements.

Chart of the week: US job cut announcements surge

Whether or not all of this leads to a recession is more uncertain. As James K regularly reminds us, the US consumer is bifurcated. The bottom 60% are already struggling, judging by rising delinquency rates, but the top 20% – which spend as much as the bottom 60% – have been propelled by higher wealth accumulated since the Covid pandemic. That’s where the recent equity weakness could be particularly influential for the US macro outlook.

For the Fed though, the base case looks more like stagflation – a slowing economy coupled with rising inflation. And the policy response to that isn’t straightforward. A lot hinges on whether the tariffs, which ultimately are a one-off rise in the price level, turn into a recurring source of inflationary pressure. James K points to cars, where higher new vehicle costs could easily fuel used prices, as well as repair and insurance.

Fed officials seem to have been particularly alarmed by the recent rise in consumer inflation expectations. We’ll get another look at those next Friday courtesy of the University of Michigan’s survey. And more importantly, we’ll get consumer and producer price data for March next week too.

That data predates all of the latest tariff news, but it could still show some impact. There’s plenty of evidence showing that firms have been pre-emptively raising prices in advance. And if that doesn’t show up in next week’s numbers, James K reminded me this week that the washing machine tariffs from President Trump’s first term hit consumers within just two or three months.

Bottom line: yes, the Fed is likely to resume rate cuts, perhaps at a faster pace than we’d previously thought. But James K thinks this is still more likely a story for later this year.

In the meantime, the real question is how long the tariffs are going to stay in place. The working assumption of many within financial markets is that Trump is much less sensitive to market turmoil than he was during his first term.

After all, a lot of political capital has been invested in reshoring activity to the US. Then there's the revenue; the extra tax dollars brought in by tariffs help the administration win over the deficit hawks in Congress as it bids to extend the 2017 tax cuts.

That’s not going to happen overnight, though, and it suggests these tariffs will stay in place for a while – or at the very least, kick in as planned over the coming days. Don't forget, further tariffs on chips and pharmaceuticals look imminent.

But the truth is nobody truly knows what comes next. What if, after all, the tariffs are a short-term maximalist tactic designed to unlock rapid concessions from US trading partners? An early test, as Lynn Song wrote this week, will be whether a deal on TikTok – should one materialise – is enough for China tariffs to be reeled in. Even then, it’s still hard to see others, like the EU, finding enough common ground to bring the tariffs lower.

Whatever happens, needless to say, the uncertainty alone is a major challenge for the global economy. Remember all that optimism surrounding Europe’s fiscal splurge? That feels like a long time ago now. Tariffs dominate the short-term outlook, and as Carsten and the team wrote this week, they may well push the ECB to take rates a little lower, a little faster than previously thought.

Just like a blockbuster movie, financial markets need a superhero. And that's the problem, maybe there isn't one... Or at least not yet. Unfortunately, trade wars rarely result in a neatly packaged Hollywood happy ending – more like a final showdown with no real winners.

Happy weekend!

THINK Ahead in developed markets

United States (James Knightley)

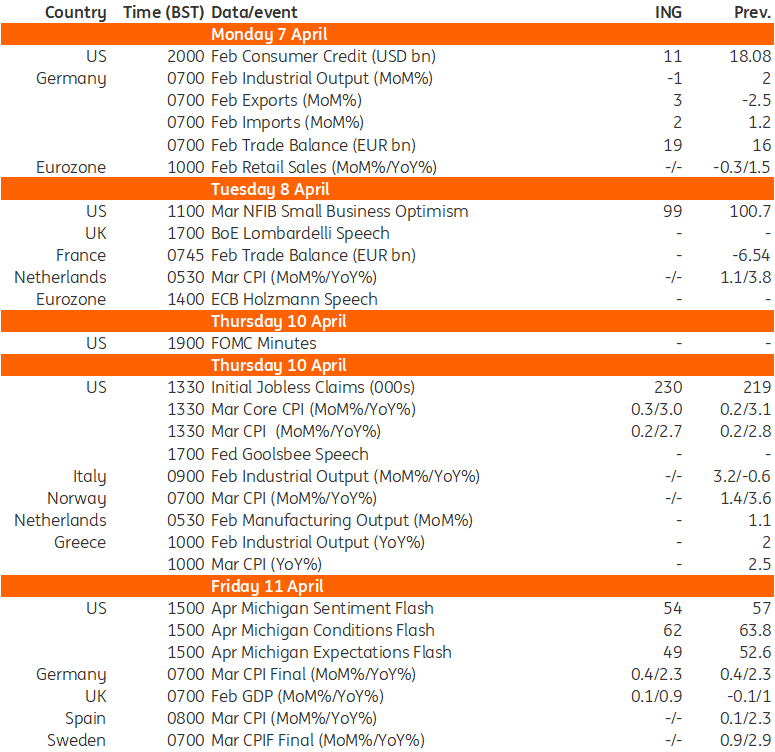

- Dark clouds are building over the US economy as President Trump’s new trade regime raises fear over higher prices and weaker economic activity. Sharply higher tariffs, borne by the importing company, risk squeezing profit margins and prompting weaker consumer spending power at a time when fears over potential joblessness are increasing and equity markets are sliding. Markets are increasingly pricing Federal Reserve interest rate cuts, but another elevated core CPI and PPI outcome next week may make the Fed hesitant to deliver on those expectations, at least in the near term.

- We will also be keeping a close eye on consumer confidence, which could lurch even lower in the wake of recent developments. We'll also be looking to see if DOGE-related government spending cuts are yielding any improvement in the fiscal numbers

United Kingdom (James Smith)

- February GDP (Fri): After a sluggish January, we're looking for a slight rebound in February's monthly GDP. These numbers do tend to bounce around, and after a more subdued end to 2024, we think the outlook for 2025 still looks okay, despite the latest tariff news. The UK government is substantially ramping up spending this year, and that will keep growth supported – though weaker activity in the US and the eurozone threatens to become a major headwind later this year and into 2026.

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

- Current account (Fri): February's balance of payments data is expected to push the 12-month rolling current account balance into deficit (-0.3% of GDP) from a balanced position. In February, exports in euro-terms were at a similar level as in February 2024, while imports have risen by 7.4% since then. Expanding domestic demand, a rebound in fixed investment, and military equipment purchases should boost imports, while external demand remains rather weak. We expect the current account deficit this year at 1.3% of GDP vs. a surplus of 0.2% of GDP, and a negative contribution of net exports to economic growth at -1.5 percentage points.

Hungary (Peter Virovacz)

- Retail sales (Mon): After a surprisingly strong retail performance in January following a disappointing December, we expect the rollercoaster ride to continue in February. We expect retail sales to fall on a monthly basis, mainly due to inflation concerns and a general weakness in consumer confidence. The surprise could come from the non-food sector on the positive side.

- Inflation (Fri): In our view, services inflation will remain hot due to seasonal increases in other services (mainly banking and insurance). The usual spring increase in food prices will be tamed as the newly introduced price cuts on 30 basic food items will find their way into headline inflation (only partially, but fully in the April print). We still expect core inflation to be hot, which means that Hungary still faces too much underlying price pressure.

Romania (Valentin Tataru)

- Interest rates (Mon): We expect the National Bank of Romania to keep the policy rate unchanged at 6.50% at its 7 April meeting, citing (amongst other things) uncertainties regarding the future fiscal policy stance, a blurry outlook to economic activity, increased risks for commodity prices stemming from trade protectionism and other main and regional central bank stances.

- Inflation (Fri): The March inflation print will likely justify a cautious policy stance, as we expect the headline inflation at 4.9%, visibly above the NBR's 4.6% estimate. Overall, the 2025 inflation picture remains fragile, exposed to fiscal, energy and geopolitical developments.

Czech Republic (David Havrlant)

- Industrial output (Mon): Output likely continued to fall in year-on-year terms in February, in part because of a base effect following last year’s strong reading. In level terms, activity has continued to stagnate, hovering around levels recorded in 2019.

- Trade (Mon): Both the trade balance and current account likely remained in surplus in February, showing only marginal moves. The trade surplus is expected to have eased in the same month, while the current account got marginally more positive.

- Unemployment (Tue): The unemployment rate is expected to have declined marginally in March due to the onset of seasonal employment gains, such as in construction and tourism.

- Inflation (Thu): The Statistical Office is expected to confirm the early headline inflation estimate, with the detailed breakdown showing mildly softer annual core inflation, somewhat slower price growth of regulated prices, and a more pronounced yearly drop in fuel prices. Meanwhile, food prices are expected to have accelerated in March.

Key events in developed markets next week

Key events in EMEA next week

Download

Download article

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more