THINK Ahead: That was the week that was…

Financial markets have had their wildest week for years. But for all the drama, the outlook for the global economy looks much like it did 7 days ago. James Smith reckons the craziness doesn't stop here. Buckle up and shout if you want to go faster, as our team tries to figure out where this rollercoaster journey goes in the week to come

The week where everything - and nothing - changed

Here are just a few things that changed in financial markets this week: US 10-year Treasury yields are up more than 40 basis points. That sort of week-on-week increase hasn’t happened since the early 2000s. The dollar is almost 4% weaker against the euro. More than a percentage point of that has happened since I started typing this earlier today. The S&P 500 is almost 4% higher, too.

What’s remarkable, though, is that for all the volatility, the outlook for US tariffs looks much the same as it did a week ago.

You might argue that’s a strange thing to say, in a week punctuated by a 90-day tariff reprieve for a range of the most significant US trading partners. But here’s the rub:

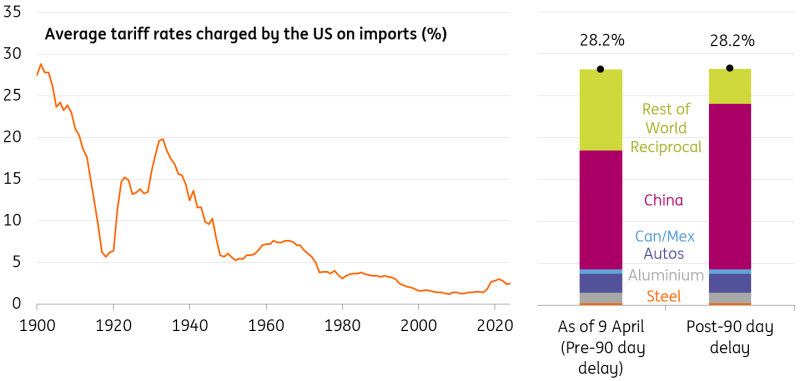

Before President Trump’s inauguration, the average tariff applied to all US imports was 2.5%. Everything that happened up until Wednesday morning – 25% tariffs on metals, autos and certain goods from Canada and Mexico, reciprocal tariffs and the last-minute additional 50% rate on China – took that rate up to 28%, if my maths is right. We have to go back to the early 20th century to find average tariff rates this high.

Wednesday’s climbdown saw a range of countries, notably in the EU and much of South-East Asia, see their tariff rate downgraded to 10%. But China, having already been hit by 104% tariffs, has now seen that rate increase to 145%, if the latest reports are accurate.

Those two changes exactly cancel each other out: The average tariff rate today is 28%, just as it was before Wednesday’s changes.

The average tariff charged by the US now stands at 28%

Admittedly, that’s a bit simplistic. Lynn Song makes the excellent point that the extra tariffs on China will have a rapidly diminishing impact. Put simply, if a US importer had the option to substitute for non-China goods, it would have done so long before rates reached 145%. And if it doesn’t have that option, then US firms and consumers simply have to pay the higher price.

Regardless, the big picture is clear. US inflation is set to rise markedly this year despite this week’s surprisingly benign consumer price data. James Knightley argues that the tariffs will hit those inflation numbers within just a couple of months. As a result, the US economy is set to come under increasing pressure, though not before we see a surge in retail sales data as consumers try to front-run the tariff rises. More from JK on that below.

That latter point is another reason to think the Fed will remain laser-focused on inflation right now. But that will start to change by the summer, and James K thinks markets are right to be pricing three to four rate cuts in the second half of this year.

As for the ECB, Carsten reckons we’re still looking at a rate cut next week. Yes, the EU was hit with lower tariffs this week than it had been expecting. But the continent’s prospects are inherently tied to the health of the US economy, just as much as they are to the tariff rates themselves. And if the US is headed for a slowdown, that can’t be good news for Europe’s export-oriented economies, whatever tariff the EU gets slapped with.

The prospect of massive government spending is still critically important, but my eurozone colleagues feel that’s more of a 2026 story. And in the meantime, it falls to the ECB to do more of the heavy lifting.

For markets, the major question – to which I don’t have the answer – is what it would take to calm things down? Is it further tariff reductions for US allies? It’s certainly conceivable that some countries will successfully negotiate carve-outs from the 10% baseline tariff. The UK might be an interesting one to watch here.

Wednesday’s drama showed that investors are receptive to signs of flexibility from the US administration. But that initial jubilation was short-lived, a recognition perhaps that further chopping-and-changing only adds to the uncertainty that’s weighing so heavily on markets and the global economy right now.

So long as the bulk of the tariffs are expected to remain for some time – and that is our base case – then that pressure may well continue.

Our bond expert Padhraic Garvey thinks Treasury yields could go higher in the near term, perhaps as far as 4.75% on the 10-year. My FX Strategy colleagues are equally wary about calling the bottom in the dollar.

This was a week where everything changed, and yet in many ways nothing changed. Next week might look much the same.

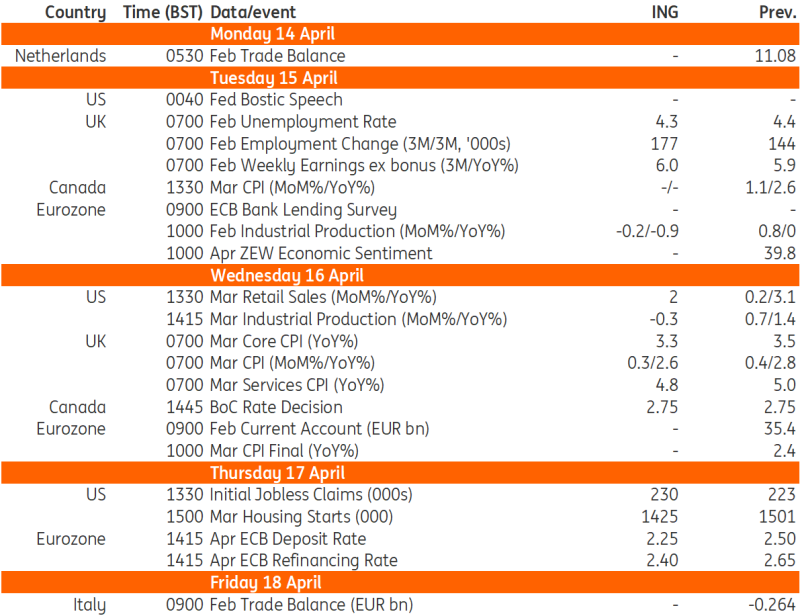

THINK Ahead in developed markets

United States (James Knightley)

- After the huge swings in sentiment seen over the past couple of weeks, we are (tentatively) anticipating a quieter macro environment in what is a shortened week due to Easter. Reciprocal tariffs have been delayed 90 days, but there are still substantial price hikes coming the way of American businesses and consumers. Moreover, we remain nervous that there are now three major headwinds for households; 1) tariffs leading to price hikes that squeeze spending power 2) increased anxiety about job losses, in part caused by major Federal government spending cuts and fears over what it means for entitlements a 3) stock market falls impacting household wealth that are making consumers more wary of making big ticket purchases.

- Retail sales (Wed): That said, March retail sales numbers should be very strong as consumers anecdotally went out and made major purchases ahead of the imposition of tariffs. Auto volumes jumped 10.6%MoM based on Wards data while credit card spending figures also suggest firm demand for appliances and electronics. This should be enough to prevent GDP growth from contracting in 1Q, but we still fear weakness will be renewed in the coming months.

- Industrial production (Wed) will also be a number to watch, given President Trump’s desire to see more reshoring. However, business surveys suggest the lack of clarity on the trading environment due to tariffs and fears of potential foreign reprisals and potential consumer boycotts of US exports is causing nervousness. We will also be closely following Fed commentary. Market rate cut expectations were for 107bp worth of cuts before President Trump backtracked on April 9. They suddenly dropped to 75bp, but given the belief that the US is facing some major headwinds, we are back up to around 90bp of cuts being priced for 2025. We agree that three or four 25bp rate cuts this year look probable.

Canada (James Knightley)

- Interest rates (Wed): Markets and economists are split as to whether the Bank of Canada will cut interest rates again next week. There is a very slim majority that favours a no-change outcome after 25bp cuts in January and March, but it could go either way. On the one hand, recent activity data has beaten expectations, and inflation has ticked higher, and the BoC may want to keep some ammunition back, given the US tariff-related uncertainty. However, a weaker jobs report and concerns about future growth, given 75% of exports go to the US, could justify another cut that would leave the policy rate at 2.50%. We are opting for a no-change outcome, also given the proximity to the election.

United Kingdom (James Smith)

- Jobs (Tues): Will the recent hike in employers' national insurance (tax) prompt a material cooling in the jobs market? Surveys suggest it might, but so far the weekly redundancy data hasn't risen. Keep an eye out for any material drop in vacancy numbers or payroll-based employment next week, though we suspect that's unlikely.

- Inflation (Wed): A fall in petrol prices will bring the headline rate down a touch in March, but the key question is how far we'll see services inflation come down. We suspect we won't see a dramatic fall here, but we could start to see more substantial improvements in the second quarter if annual price resets are less aggressive than a year earlier. That is one of the reasons why we expect the Bank of England to keep cutting rates once per quarter for the rest of 2025 and into 2026.

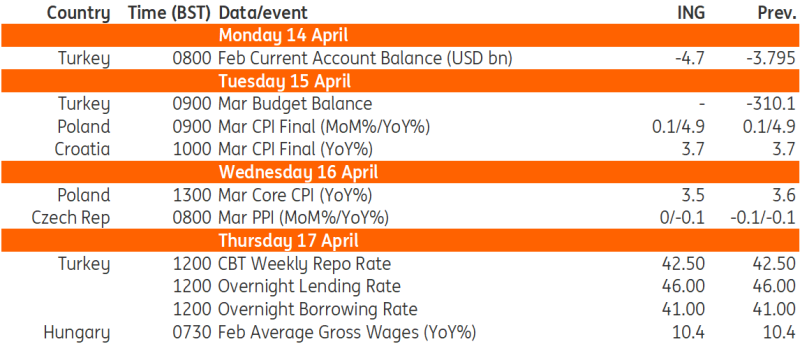

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

- CPI/Core inflation (Tue/Wed): Detail CPI data due on Tuesday should confirm that core inflation excluding food and energy prices (official data the National Bank of Poland publishes on Wednesday) continued its downward trend in March, providing one of the arguments for the Monetary Policy Council (MPC) to start monetary easing in May. In the face of the negative impact of the potential trade war on economic activity, the Council is unlikely to delay rate cuts and we see a chance of a 50bp cut in May.

Czech Republic (David Havrlant)

- PPI (Wed): The pricing in the industry remained under pressure in March, as foreign demand stayed lukewarm, and price competition was elevated. Industrial producer prices likely remained in a mild annual decline in March, also affected by declining global energy prices in the same month and a stronger domestic currency, which makes all imports cheaper.

Turkey (Muhammet Mercan)

- Interest rates (Thu): In the interim meeting following the March volatility, the CBT not only raised the upper band of the interest rate corridor (overnight lending rate) to 46%, but also turned it into the effective policy rate by tightening TRY liquidity, while keeping the policy rate (1-week repo rate) flat at 42.5%. These developments suggest that the CBT is likely to remain mute in the April MPC meeting. Benign March inflation data, with an improvement in the underlying trend, will also lead the CBT to keep the policy rate unchanged rather than hike it. However, the CBT's daily balance sheet has, in recent days, shown a continuation of the pressure on the net FX position. Therefore, we do not rule out a further adjustment in the upper band.

Key events in developed markets next week

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article