THINK Ahead: Tariffs, US jobs, and the ECB in focus

It's set to be a pivotal week for markets, as trade tariffs on imports from China, Mexico, and Canada are due to kick in. The US jobs report for February and a decision from the European Central Bank will also keep investors on high alert

THINK Ahead in developed markets

United States (James Knightley)

- This week promises to be significant for the US, with potential trade tariffs on imports from China, Mexico, and Canada coming into effect while there are some very important data releases, including the February jobs report.

- President Trump has moved the date around, but at the time of writing trade tariffs are set to start from 4 March. He claims that foreigners will pay thanks to a stronger dollar nullifying the impact on US consumer prices while leading to a loss of purchasing power for foreign trading partners. However, we are sceptical and expect price increase for consumers, just as we saw with washing machines in 2018. Consumer confidence is already weakening on concerns about consumer spending power and government austerity measures, and more headlines about tariffs won’t help the situation.

- Regarding the data, the ISM reports are expected to confirm that the soft start to the year for growth is continuing. Regional manufacturing surveys point to a small pull-back in the national measure, while the services ISM is subject to downside risk based on evidence seen within other business surveys. This sense of caution among corporate America as President Trump looks to change the nation’s trading platform with partners is likely to mean another subdued increase in payrolls. We think the cuts to federal government jobs will take at least another few months to become apparent in the data.

Eurozone (Bert Colijn)

- Interest rates (Thu): In the eurozone, all eyes will be on the European Central Bank next week, which will receive another inflation report before deciding on interest rates on Thursday. While a 0.25% cut seems like a done deal, inflation could be in for another uptick in February before it starts to ease again. With hawks on the governing council more vocal these days, that makes the discussion around the terminal rate for the eurozone all the more interesting.

- Unemployment (Tue): Also keep an eye out on unemployment. While PMIs indicate that businesses have started to shed workers in recent months, the unemployment rate is holding steady at the historic low of 6.3%. We don’t expect an immediate turnaround, but any turn in the slow-moving eurozone labour market will be relevant in determining how low the ECB can set interest rates.

THINK Ahead for Central and Eastern Europe

Hungary (Peter Virovacz)

- Industry / Retail sales (Thu): While next week is a busy one, we believe that the January industrial production and retail sales data could be the most decisive. Although the 4Q GDP data could give us some clues for 2025 via the carry-over effects in consumption and investment, for example, January's sectoral performance will be more crucial. And here we expect a rebound. We see production picking up in the wake of longer-than-usual year-end shutdowns in industry. An unusually long holiday season is likely to have had a negative impact on the retail sector, so we also see sales picking up at the start of the year. But there is also hope that some of the coupon payments from retail bonds have found their way to the cash registers.

Czech Republic (David Havrlant)

- PMI (Mon): The manufacturing PMI likely continued to improve in February, though moderately, and stayed in the contraction zone. The forces at play are the elevated uncertainty stemming from the recent geopolitical shakeup with respect to Europe’s security, and the rapid development surrounding possible peace talks regarding the war in Ukraine. The German election outcome and more clarity about the need for a European Plan B are also substantial factors shaping the industrial outlook, for example, in the defence sector.

- Inflation (Wed): Inflation likely decelerated somewhat in February, primarily reflecting less potent inflation in the service sector, as price dynamics in this segment may have reached some saturation, given the rapid growth during the past quarters. In contrast, price dynamics in the food segment likely drove overall consumer price trends during the same month, preventing a more significant slowdown in the headline inflation rate.

- Wage growth (Thu): Wage growth likely decelerated in both nominal and real terms towards year-end, with the malaise in the manufacturing sector possibly leading to a reduced willingness to continue with lofty wage hikes. The spike in consumer inflation, in turn, made a dent in real wages in the last quarter of the previous year. Still, real wage growth has remained solid enough to enable households to carry on spending.

Kazakhstan (Dmitry Dolgin)

- Interest rates (Fri): The National Bank of Kazakhstan (NBK) will be deciding on the base rate on Friday. The options are to maintain the current rate of 15.25% or to hike, as suggested by the previous signals. Our base case is a hold, given the recent approximately two percentage point improvement in the inflation expectations among households and businesses, as well as the 6% appreciation of the tenge against the US dollar since the last NBK meeting.

- Inflation (Mon): However, much will depend on the current CPI reading for February, which will be released ahead of the decision. A further acceleration in inflation from January’s 8.9% year-on-year reading may tip the scales in favor of a hike. In any case, the overall stance is likely to remain cautious in the coming months because of the medium-term inflation risks stemming from the ongoing tariff liberalisation and a recent proposal to proceed with fiscal consolidation through an increase in VAT. According to official estimates, if this is confirmed by mid-2025 and implemented in 2026, it could add two and a half to three percentage points to inflation.

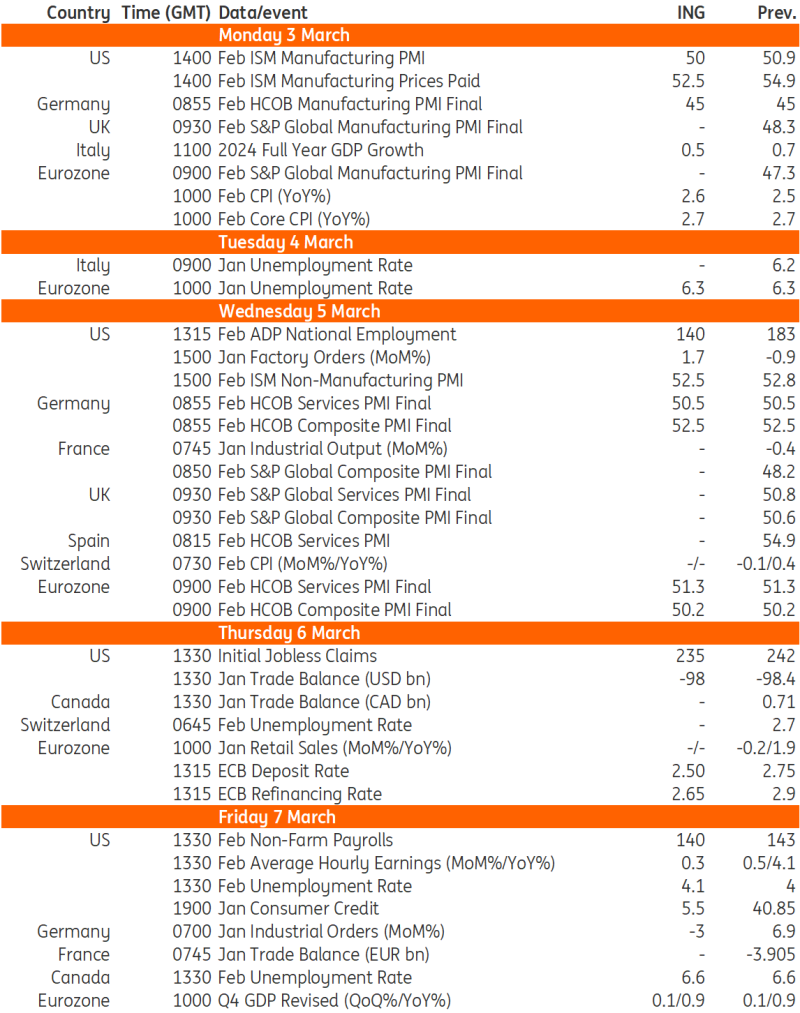

Key events in developed markets next week

Source: Refinitiv, ING

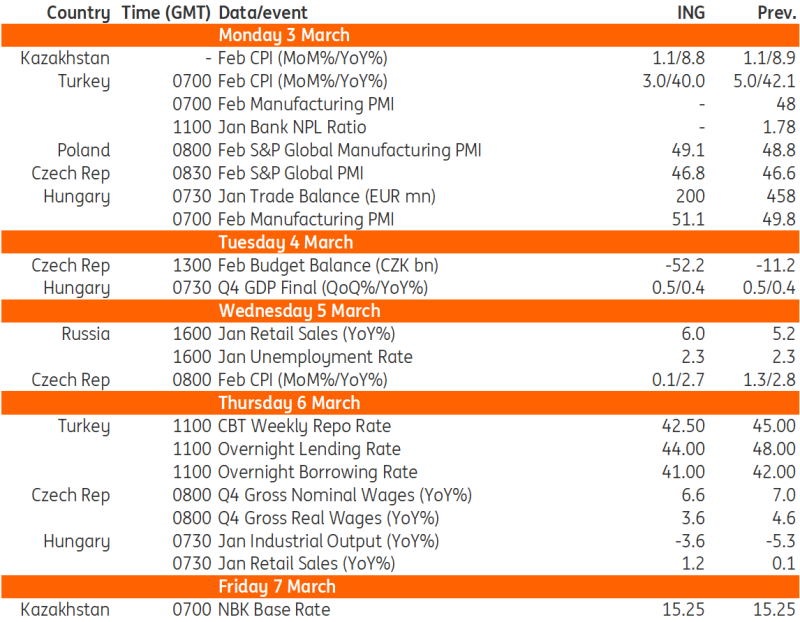

Key events in EMEA next week

Source: Refinitiv, ING

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article