THINK Ahead: No football? Watch these market fixtures instead

- Published 11:30

- Key Events

Fill the World Cup-shaped hole in your diary with James Smith's guide to a hot summer in financial markets. From central banks to inflation, it's a line-up promising upsets and maybe even the occasional own goal…

Seven summer fixtures for markets

The World Cup is over. Well, it is for England anyway. And if, like me, you’re still coming to terms with yet another World Cup disappointment, the BBC had some advice this week: Focus on the wins!

Not helpful if you’re German or Dutch (there just weren’t very many – sorry guys!). And perhaps best not to mention “there’s always next time” to the Italians – for whom there hasn’t been a next time for 12 years now…

Fortunately, markets have their own summer fixture list to fill the World Cup-shaped void. Central banks, data, politics: it’s a line-up that promises upsets and, dare I say it, the occasional own goal…

20 July: Britain’s new prime minister

The summer transfer window is open and Britain’s getting a new prime minister on Monday. Disgruntled football fans aren’t the only problem Andy Burnham inherits. Inflation is set to edge closer to 3.5% this summer, keeping borrowing costs elevated and chipping away at his fiscal wiggle room.

We don’t know much about his plans for the Autumn Budget yet, but it’s likely some of his bolder ambitions will get parked in favour of easier – and cheaper – initiatives on the cost of living. The knock-on effects for the Bank of England needn’t be huge.

This is all fairly consensus now, speaking to investors recently. But British politics has taught us to expect the unexpected. A big budget can’t be ruled out – and personally I don’t think a snap election can, either.

23 July: European Central Bank decision

The ECB isn’t one for surprises. And with less than a 10% chance of a rate hike priced in at next week’s meeting, it’s hard to see Frankfurt rocking the boat.

Yet energy prices, particularly gas, are dragging the ECB closer to its June base case again. Those forecasts envisaged core inflation above target for the foreseeable future, even with one further rate hike.

My colleague Carsten Brzeski argues there is a case for acting sooner rather than later. Still, a move in September is much more likely, and that’s our base case.

30 July: US core PCE inflation (and 12 August for CPI)

This week’s US inflation figures were super benign. Core CPI was flat on the month for the first time since 2021. And it’s well-timed; even prior Fed doves like Christopher Waller have been setting the scene for rate hikes.

One reading doesn’t make a trend. Officials are clear that several months of better data are needed. And the Fed’s preferred PCE inflation gauge could come in a tad hotter than CPI later this month, boosted by measurement differences for air fares, medical care and portfolio management fees.

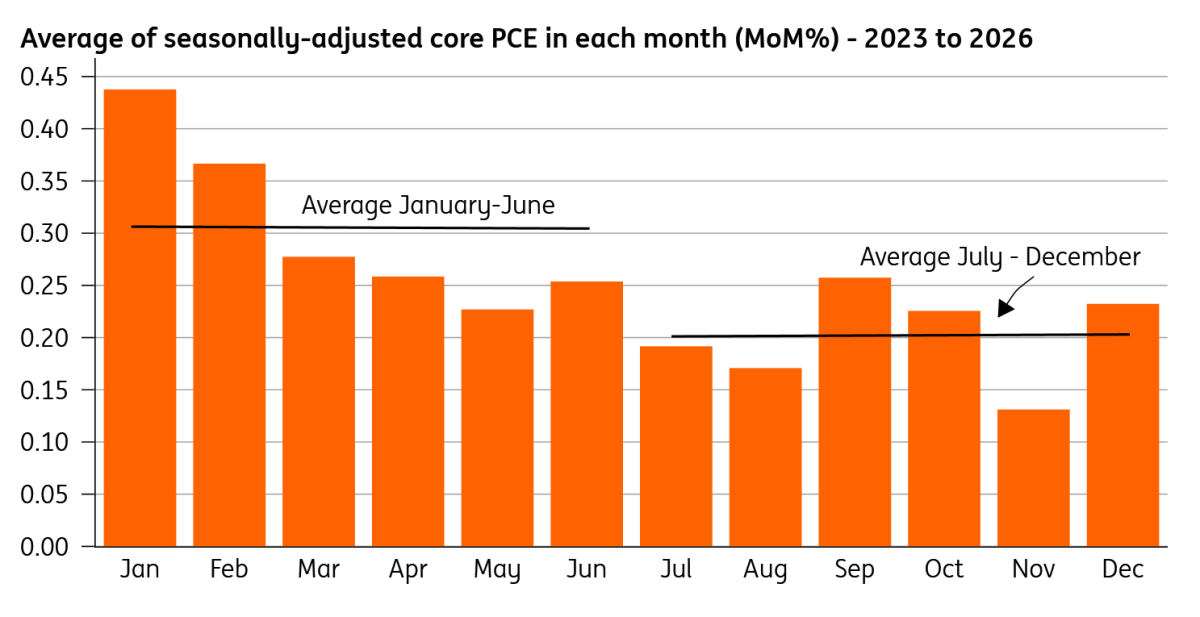

Still, our man in the US, James Knightley, is optimistic. He sees four reasons why inflation should start to turn a corner: limited upside from gasoline prices (barring another big spike in crude), subdued wage growth, falling rental growth and the end of tariff inflation. I’d add a fifth: core PCE has repeatedly been softer in the second half of the year since 2023, hinting at lingering seasonality issues. Check out the chart below…

US core PCE inflation tends to be more benign later in the year

30 July: Bank of England decision

I think a rate hike is still unlikely this summer, even if inflation is still a worry. Officials said last summer that it’s more problematic when headline inflation goes above 4%. And we’re still some way off getting there. Plus, services inflation is set to edge lower next week. Private sector wage growth has further to fall, having already dipped below the 3.25% level the Bank says is consistent with a 2% inflation target over the longer term.

July’s meeting may therefore look much like June’s, when policymakers voted 7-2 to leave rates unchanged. I do not expect hikes this year and still think cuts will return in 2027.

Seeing out the match rather than launching a fresh attack… Thomas Tuchel for Bank of England governor?

31 July: Eurozone inflation

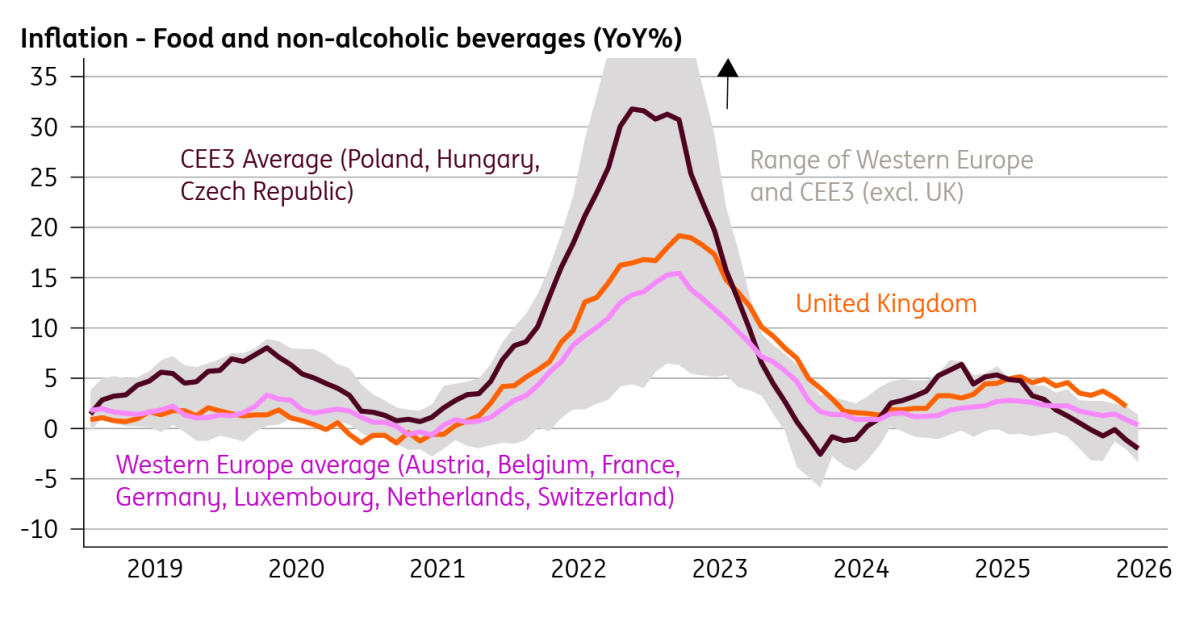

Better-than-expected June inflation is another reason the ECB can afford to be patient this month. Energy is helping, but food inflation is a real surprise. It’s below ECB forecasts, and remember this is where so-called second-round effects of higher energy prices are supposed to show up. They still might – this won’t be settled for several months, but for now the news is promising.

The more pressing question is what happens to core inflation. The ECB expects it to edge up in the third quarter and it would presumably take both a meaningful downside surprise and lower geopolitical tensions to derail a September hike.

European food inflation has surprised lower

7 August: US jobs report

The whole reason the Fed is singularly focused on inflation right now is because the jobs market appears to have turned a corner. Yet it’s a mixed picture. Last month’s payrolls data featured big downward revisions. And some vacancy measures dispute the uptick we’ve seen in the official numbers.

Participation – the share of the workforce either employed or seeking work – has fallen, raising questions about why people are moving to the sidelines of the jobs market. That’ll be a key question for the August decision.

That all said, James Knightley is tentatively looking for a 75,000 increase in July’s payrolls. That’s unlikely to rock the boat for the Fed.

27-29 August: Fed Jackson Hole conference (plus 29 July Fed meeting)

Kevin Warsh has been more hawkish than most expected. But is that because he genuinely thinks rates need to rise as nine of his colleagues did last month, or is it just tough talk to keep markets on his side? We suspect it’s more likely the latter – the central bank equivalent of keeping possession and running down the clock (that one doesn’t even make sense, does it?).

But Warsh’s preference for saying little means we might not learn much more this summer. His big thing is abolishing forward guidance, though nobody seems to have told his colleagues. Last week’s Fed minutes and a speech by Christopher Waller were both surprisingly clear about what the Fed needs to see to avoid a rate hike.

That means it’s the data – particularly those inflation figures – that will do the talking. One inflation clean sheet is encouraging; two or three start to look like a winning streak. My US colleagues don’t expect rate hikes this year.

THINK Ahead in developed markets

United States (James Knightley)

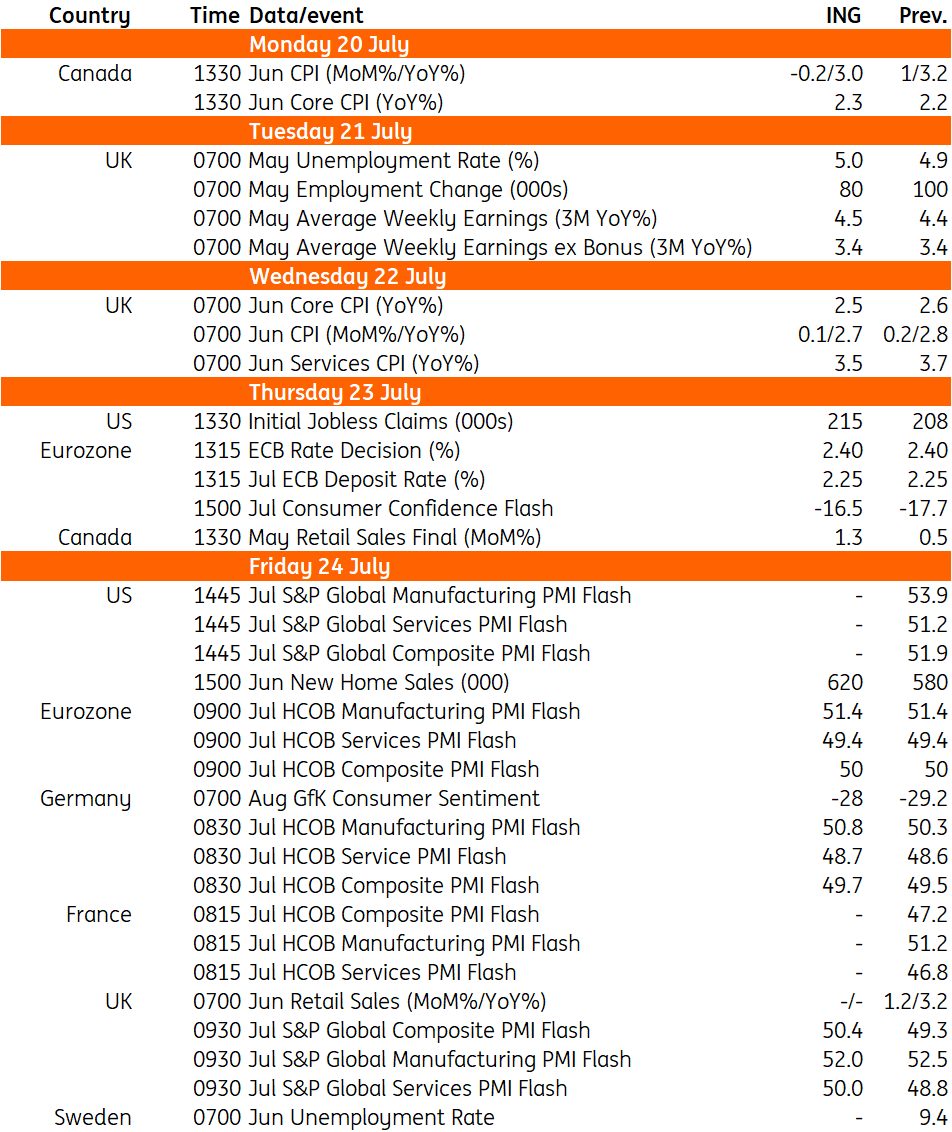

The Federal Reserve has entered its quiet period ahead of the July 29 FOMC meeting. Market expectations for a potential rate hike receded following the June CPI, PPI and Beige Book reports that all pointed to softer-than-anticipated inflation pressures. Pricing suggests just a 10% chance of a hike on 29 July, whereas before those inflation prints, it was seen as a coin toss. We continue to argue that lower energy prices, weak wage growth, slowing housing rents and a diminishing influence from tariffs will keep the disinflation trend in place and the Fed won’t need to hike rates.

Next week’s data calendar is also light, with home sales the most notable release. As such, markets will remain focused on Middle East developments and the price of oil, together with a heavy calendar of corporate earnings numbers, with several of the big tech companies set to report next week.

Eurozone (Bert Colijn/Carsten Brzeski)

- European Central Bank (Thurs): While we expect the ECB to stay on hold next week, a surprise hike should not entirely be ruled out. Read our full preview

- Purchasing Managers Index (Fri): Last month’s PMI didn’t fully incorporate the reopening of the Strait, but this month’s will likely have already missed the most optimistic take on things. With the conflict flaring up again, immediate hopes of a swift reopening are thrown into uncertainty. This leaves a cautious view of the economy as the most likely outcome. Perhaps a bit more positive than last month, but the timing of answering the survey will remain key. Underlying, economic growth seems set for very muted growth in the short run. So no expectations of miracles yet.

United Kingdom (James Smith)

- Jobs report (Tues): The UK jobs market remains under pressure and recent payroll data has shown little sign of a turnaround, particularly in the embattled consumer services sector. Private sector pay growth is biased lower in the near-term as a result.

- Inflation (Weds): Lower petrol prices should help headline CPI nudge slightly lower. Services inflation is set to fall too. Inflation is set to rise in July as household energy bill hikes kick in, but we still expect it to peak below 3.5% this summer.

THINK Ahead in Central and Eastern Europe

Poland (Adam Antoniak)

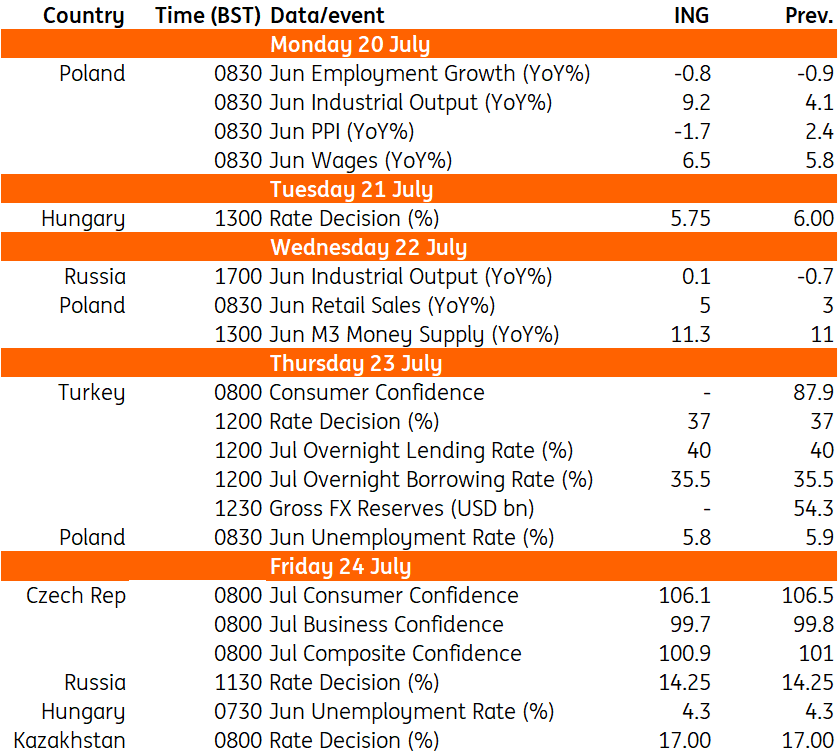

- Industrial production (Mon): Even though the June manufacturing PMI disappointed, we still expect solid growth in industrial output. The calendar effect is more favourable, with one additional working day year-on-year, and the base effect is supportive, as June 2025 was particularly weak in several volatile manufacturing sectors. We forecast that PPI remained positive in annual terms after many quarters of deflation, although inflation likely moderated as producer price growth came to a standstill on a month-on-month basis in June.

- Construction output (Mon): Polish construction activity is catching up after a weak start to the year caused by adverse weather conditions. Combined with a favourable calendar effect and a strong investment pipeline for 2026, we would not be surprised to see another solid year-on-year increase in June. Civil engineering should continue to benefit from robust public investment, while growth in building construction may be somewhat constrained by the weak performance of residential construction, as this segment of the market appears oversupplied.

- Wages & Employment (Mon): Wage growth is generally moderating, but the higher number of working days likely pushed the annual growth rate slightly above the levels recorded in the previous two months. Even so, the cooling labour market and the absence of significant wage pressures following the strong increases in compensation seen over the past three years mean that wages are becoming less of a concern for monetary policy as a potential source of inflationary pressure. Employment in the enterprise sector continues to decline in annual terms, although we expect a seasonal increase in the number of jobs compared with May.

- Retail sales (Wed): Following the initial hit from the surge in petrol prices, consumer confidence has improved in recent months. As a result, we expect solid demand for durable goods. Recent volatility in retail sales has been driven by the timing of Easter-related purchases and fluctuations in fuel demand amid soaring oil prices. Following the mid-June announcement of measures aimed at containing retail fuel prices, including lower excise duties and VAT rates combined with a price cap, demand for fuel likely increased sharply in the second half of the month as motorists anticipated higher prices ahead. Indeed, fuel prices rose noticeably at the beginning of July.

Hungary (Peter Virovacz)

- Base rate (Tue): This time, there is no need to outsmart or overthink anything or anybody. National Bank of Hungary Governor Varga announced the 'mini rate-cut cycle' for the summer in June, and nothing we have seen so far has knocked the plan off course. Against this backdrop, we anticipate a 25bp reduction in the base rate, bringing it down to 5.75%. Looking ahead to the remainder of 2026, we forecast further easing, with three or four additional rate cuts following July's move.

Czech Republic (David Havrlant)

- Consumer and business sentiment (Fri): Both consumer and business sentiment likely softened marginally in July, reflecting renewed geopolitical tensions in the Middle East, with significant implications for both energy prices and uncertainty. That said, Czech manufacturers and consumers have shown considerable resilience so far.

Turkey (Muhammet Mercan)

- Central bank decision (Thur): The policy outlook has shifted in recent days, both because of geopolitical tensions which have pushed oil prices above US$80/bbl, and a decision to gradually unwind a sliding scale tariff mechanism, which reduces the room to absorb the impact of higher oil prices, despite measured regulated price hikes. This backdrop will likely lead the central bank to be more cautious in easing liquidity conditions. We expect the policy rate and corridor structure to stay unchanged at the July MPC meeting and the bank to continue funding from the upper band of the corridor, in the near term.

Kazakhstan (Dmitry Dolgin)

- Base rate (Fri): We expect the National Bank of Kazakhstan to hold the policy rate at 17.00%, as, following the surprise cut in June, CPI showed no material decline and remained in double-digit territory at 10.3% YoY, while forward-looking indicators continue to warrant caution. The strength of the KZT remains a disinflationary factor, though declining state support for the local FX market is something to watch.

Key events in developed markets

Key events in Central and Eastern Europe

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more