THINK Ahead: Beware of economic showers from the west

Europe has been basking in sunshine, literally and metaphorically. But pesky April showers keep moving in from the west, writes James Smith. Bring your umbrella as we forecast next week's market moves

THINK Ahead: Europe's cold April shower

Are we all becoming too optimistic about Europe?

Bet you didn’t expect to see those eight words printed this year, did you? Neither did I, if I’m honest. We European economists don’t know what to do with ourselves; we simply aren’t programmed for these levels of unalloyed positivity.

But two things can be true at once. The wave of fiscal activism unleashed by Germany’s spending splurge could genuinely lift the continent out of its decade-long malaise. It could also make next to no difference to the growth story in 2025.

Maybe I’m being overdramatic (an economist, dramatic? Never!). However, it was notable how my colleagues made only minimal changes to their 2025 growth forecasts. Put simply, the impending trade war still looks like a much bigger deal for the eurozone economy this spring and summer than any boost to government budgets.

Remember that we’re little more than a week off the publication of the Trump administration’s varied investigations into unfair trade practices and deficits. And for all the flip-flopping on Canada and Mexico tariffs since inauguration day, we think sweeping and potentially long-lasting tariffs on Europe are just days away. Our trade expert, Inga, explains more in her latest video.

All of this explains why I’m still having a hard time seeing European growth taking off in quite such a meaningful way this spring. Certainly the activity data we’ve had so far this year hasn’t been scintillating.

It seems the ECB agrees. I’m struck by how even some of the more hawkish members of the Governing Council aren’t ruling out another rate cut in April.

That’s not our base case, but speaking to our ECB guru, Carsten Brzeski, he reckons a hold at the next meeting certainly isn’t a done deal, not least if Europe finds itself in the midst of a rapidly escalating tit-for-tat trade war.

As for that massive €500bn infrastructure fund, the question lingering in the back of my mind is how quickly the cash can land in the German economy. Certainly, the political incentives are there to get things moving; Carsten reminds us that there are crucial state elections next year.

But if it’s anything like it is here in Britain, finding the proverbial shovel-ready projects can take time. I'm reminded of the infamous car tunnel under London’s River Thames, which has cost upwards of £1bn, taken several years, and not a single ton of earth has yet been shifted.

Maybe woeful infrastructure deployment isn’t the only cautionary tale Britain has for the rest of Europe. In many ways, the UK is six months ahead. It unveiled big changes to its fiscal rules and a sizeable budget boost last October. The rise in bond yields and Bank of England interest rate expectations will be eerily familiar to anyone tracking eurozone borrowing costs right now.

But those market moves are forcing a partial rethink upon the Treasury. More money on debt interest means less for everything else. Spending cuts are widely expected at next week’s Spring Statement and we think further tax rises are inevitable come the next budget in Autumn.

Despite sweeping changes to the European Commission’s budget rules, something very similar risks happening elsewhere. Bond yields are higher than they were a month ago and will keep rising, judging by our team’s latest forecasts. Higher defence spending could ultimately necessitate cuts elsewhere, just as we’re seeing in Britain.

If that happened, then my concern is that the growth impact would be asymmetrically negative. Austerity hits the economy today. Higher defence and infrastructure won’t, either because of domestic production constraints (for the former) or potentially long lag times (for the latter). I'm obviously getting ahead of myself a bit here, but it’s another reason to be wary about a big upswing in European growth this year.

It’s not all bad, of course. Europe’s jobs market remains a bright spot. As does consumer spending though, as Bert Colijn says, a lot hinges on an improvement in confidence. Speaking of confidence, next week’s Purchasing Managers’ Indices will give us an early sense of whether companies are quite as jubilant as their soaring stock market valuations imply.

Europe is bathing in sunshine – literally and metaphorically. But don’t be fooled: cool April showers are only just around the corner. Happy weekend!

THINK Ahead in developed markets

United States (James Knightley)

- Sentiment (Tue): The US calendar is focused on the consumer, with sentiment and spending numbers set to be released. Consumer confidence has been sliding as households worry about the impact of Department of Government Efficiency spending cuts on jobs and entitlements. Meanwhile, the threat of tariffs is prompting concerns about higher prices that could squeeze spending power and lead to a deterioration in the standard of living. Falling equity markets are adding to consumer fears for the economic outlook.

- Inflation (Fri): Fed Chair Powell has downplayed the softer sentiment prints, saying that these “readings have not been a good predictor of consumption growth in recent years”. As such “we do not need to be in a hurry [to alter monetary policy], and are well positioned to wait for greater clarity.” February personal spending numbers will therefore be closely watched given that January’s figure fell 0.2%MoM in nominal terms and –0.5% in volume terms. We expect to see stronger +0.7% and +0.4% prints this time, but consumer spending in general is likely to soften further in the months ahead, which would help leave the door open to a September Federal Reserve interest rate cut.

United Kingdom (James Smith)

- Inflation (Wed): Expect headline CPI to dip fractionally, but generally,y the trend is upwards this year. Energy prices are increasingly no longer a drag on overall inflation, and that’s largely why CPI is set to peak close to 4% in the second half of the year. Services inflation should show more progress, though. We expect a slight fall for February and further improvements through the Spring.

- Spring Statement (Wed): Following a rise in debt interest costs, the Chancellor needs to find modest savings to make the fiscal rules add up once more. Despite all the noise, the impact of these changes won’t be huge either on the economy or the Bank of England. But it does set up some difficult decisions in the Autumn. We expect further tax rises later this year. Read our full preview

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

- Retail sales (Mon): February data readings from industry and construction were weak. The retail sales report should bring in a positive annual figure, confirming that consumption remains the main engine of economic growth in Poland. Slower annual growth in February as compared with January is linked to a negative calendar effect.

- Unemployment (Tue): Unemployment remains low and stable despite a continued decline in employment due to weak supply of workers stemming from demographic trends. The labour market remains tight as the net inflow of migrants is not as big as the first wave of refugees from Ukraine after Russian invasion. We expect the registered unemployment to run close to all-time lows in 2025.

Hungary (Peter Virovacz)

- Interest rates (Tue): The new era is about to begin, as the upcoming rate-setting meeting will be the first under the new leadership of Mihály Varga. Although there is a new sheriff in town, we expect the same result as in the last five months. Well, it is the same "town" after all. With the inflation outlook deteriorating, we see no room for anything other than a hawkish hold. Talk of rate hikes will also be premature as the NBH will most likely want to see the longer-term results of the recently introduced price curbs.

Czech Republic (David Havrlant)

- Interest rates (Wed): The CNB bank board will likely vote in favour of no change in the base rate as the policymakers are approaching the fine-tuning phase of establishing the appropriate capital cost landing runway. With headline inflation more potent than the CNB expected from the onset of the year, stronger wage growth, and a more buoyant economic outlook, we see reasons for a hawkish stance. Still, there is some space to ease the overall monetary conditions, yet this will be executed cautiously when a new fully-fledged forecast is available.

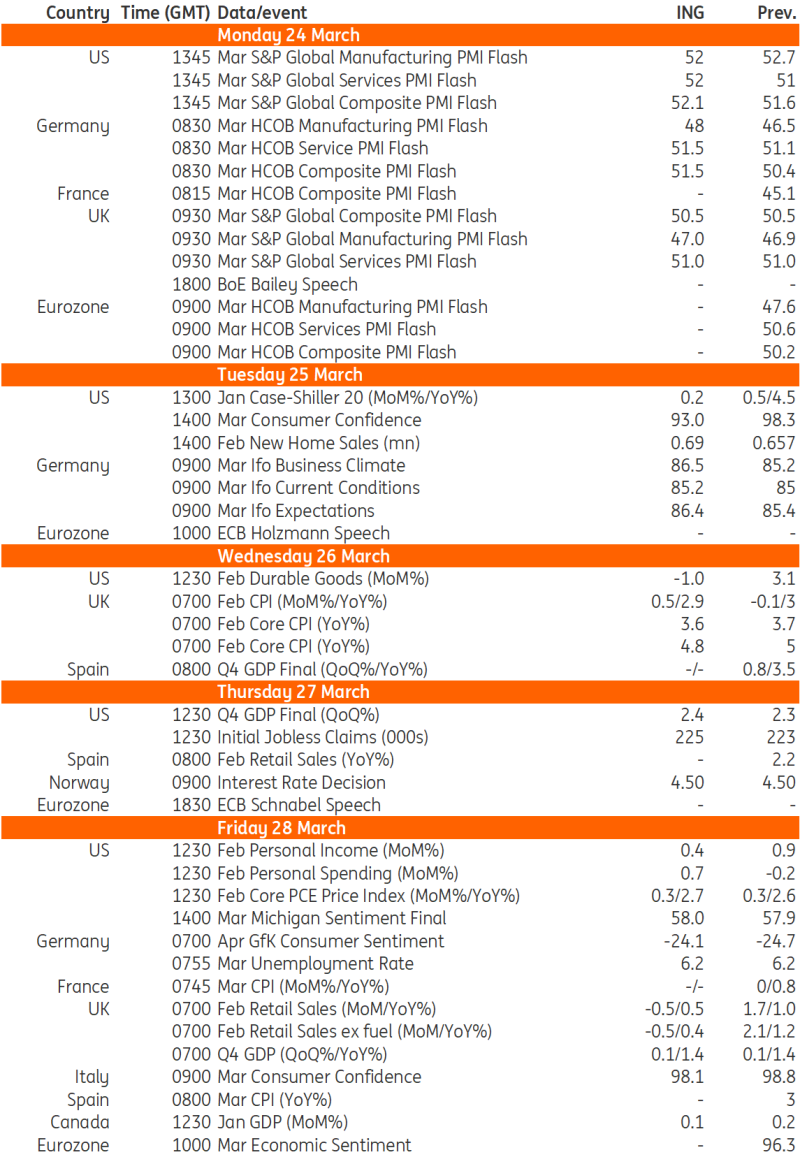

Key events in developed markets next week

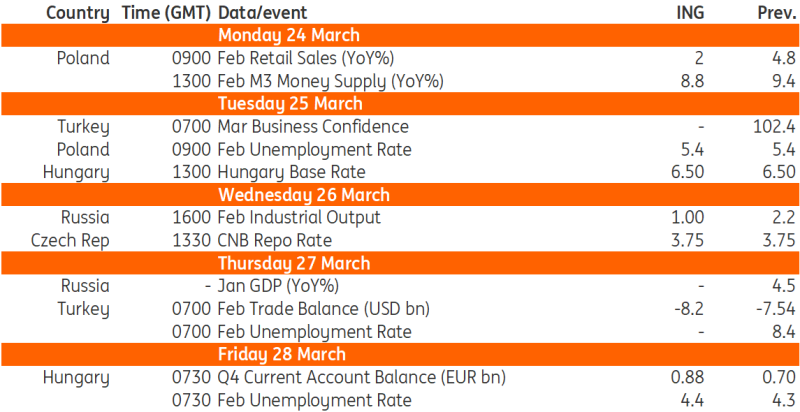

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article