THINK Ahead: Inflation confidence shifts to caution

Last summer's fleeting confidence in inflation has long since evaporated at the Federal Reserve. Tariffs aren't helping, but are they really a gamechanger for inflation? Well, it depends and there is at least one reason why US officials can still be optimistic. Read on as James Smith and the team tackle another busy week ahead

Somewhere on LinkedIn, a man celebrated his seventh work anniversary this week.

It’s been a tough journey, notes the obligatory social media post. Pandemics, market chaos, bank collapses, he’d dealt with it all. He glosses over the fact that he and his boss don’t always see eye-to-eye anymore. But he ends by saying how the past year in his job was probably one of his best.

The man, of course, is Federal Reserve Chair Jerome Powell. And no, I doubt he is a LinkedIn kind of guy either. But it’s perfectly true that for a few glorious months last summer, he and his comrades at the Fed enjoyed a rare moment of confidence. Inflation was becoming more predictable, giving officials the much-needed courage to start cutting rates.

That confidence has, unsurprisingly, diminished. Stickier inflation numbers and tariff threats have prematurely put the brakes on the Fed's ambitions to get interest rates back to neutral. And despite this week’s fireworks at the White House, our US team still thinks tariffs are coming. Long-running trade grievances with Europe and China are likely to be the key focus come April’s reports into unfair practices.

But for all the hype, are tariffs really a big deal for inflation? A new report from the Boston Fed concludes that 25% tariffs on China/Mexico and 10% on China, had all of that happened, would add less than a percentage point to core inflation. And that’s before considering any offset from the hit to consumer demand. Our US guru James Knightley reached a similar conclusion in a report last year.

Those aren’t big numbers in the scheme of things, but as that Fed paper makes clear, it really comes down to how firms respond. Small changes to retail margins can make a surprisingly big difference.

A quick glance at the producer price numbers show that those margins massively expanded during Covid and haven’t really been hacked back since. But are firms still well positioned to pass on the full costs of higher tariffs? Speaking to James K, the jury’s out on that one.

Consumer spending still looks decent – next week’s weather-battered retail sales not withstanding – and presumably will get a boost as shoppers front-run tariffs. But surveys on selling prices haven’t actually changed all that much recently, considering all the noise. Time will tell on who’s going to shoulder the heavy burden.

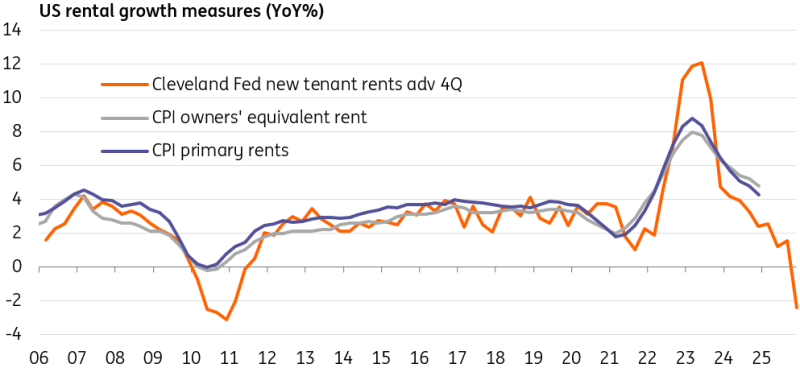

Away from tariffs, and good inflation news can still be found if you know where to look. Rents have been a major driver of core inflation for a long time now. But check out the chart below. Rents are actually falling, according to Cleveland Fed data on new tenant agreements. If that’s true, then that could be a massive underappreciated source of disinflation later this year.

Chart of the week: US rents are plunging

None of this is to say inflation won’t remain elevated this year; James K thinks it will. But I suppose what we’re saying is don’t blow things out of proportion just yet, not least because it's far from clear how inflationary the president's plans on tax and migration will end up.

Over here in Europe, policymakers face a different challenge: higher natural gas prices. Headline inflation is creeping higher and European surveys on selling prices have started to rise again.

None of this seem to be faze the European Central Bank, who unlike the Fed, still seems plenty confident in the road ahead for inflation. Safe in the knowledge that wage growth is set to fall this year, further rate cuts are essentially a done deal.

But listening to the Bank of England this week, it’s clear that the ghosts of the 2022 gas price shock are still haunting officials. The recent pick-up in household energy bills is nothing like what we saw back then. But in an environment of sticky wage growth and stubborn services inflation, policymakers are seemingly worried that it wouldn’t take much to stoke the fire once again.

I’m less convinced about that. And for all the debate about inflation, it’s growth that we really need to talk about. Nobody is in any doubt about the issues Europe is currently up against. Even the US faces a mounting number of headwinds later this year.

That's why my US colleagues are still expecting three more rate cuts in Powell's final period in office – a time which, let's face it, is going to be anything but smooth. At least he'll have plenty to write about in next year's LinkedIn post...

THINK Ahead in developed markets

United States (James Knightley)

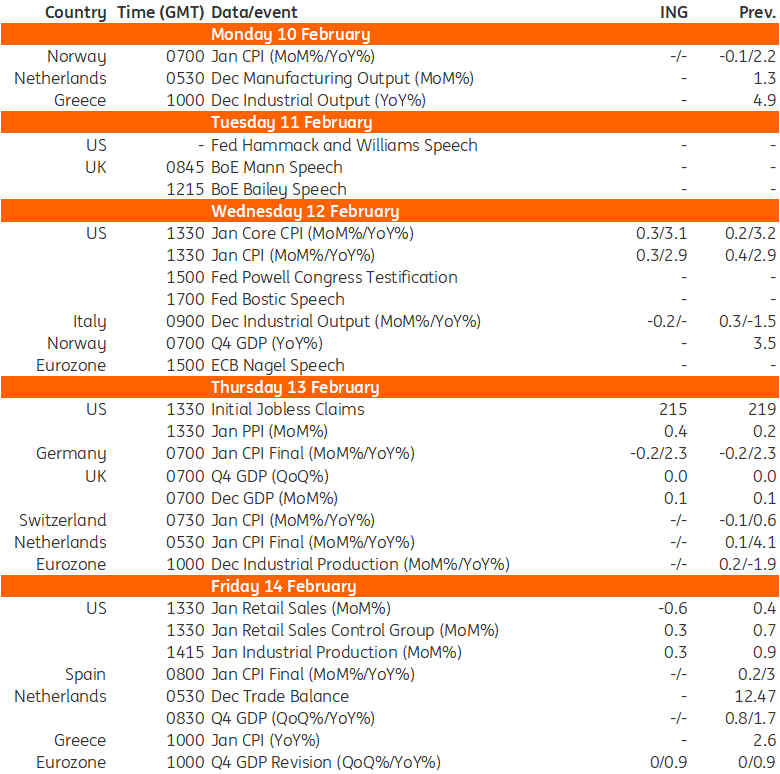

- Inflation (Wed): US President Donald Trump’s ability to surprise markets with new announcements on a multitude of topics will continue to keep participants on edge. That said, we have a lot of “traditional” macro drivers too. US inflation will make early headlines next week, with the risk that we see 0.3% month-on-month prints for both headline and core measures. Food prices (egg prices in particular) and energy costs have been rising while vehicle prices are grinding higher and housing costs remain sticky. While Trump has pulled back on tariffs in recent days, there is still a sense that we are likely to see the introduced in the second quarter once the Commerce departments report back on trade practices employed by foreign governments. This suggests inflation is likely to remain elevated and that the Fed is unlikely to cut rates before June.

- Fedspeak (Wed): Fed Chair Jerome Powell will be testifying before Congress when the Federal Reserve releases its semi-annual Monetary Policy report. It will likely highlight significant economic uncertainty relating to Trump’s policy mix but again confirm that while the Fed is still inclined to loosen policy, it needs to the data to justify that, with little chance of an imminent rate cut after 100bp of easing in the latter part of 2024.

- Retail sales (Fri): On the activity front, we look for soft retail sales given auto purchase volumes fell more than 7% on the month. Bad weather certainly deterred people from going out and about and this too will weigh on travel and leisure and hospitality spending. Stripping out the volatile components (food service, autos, gasoline and building material), we look for the “control” group to post modest nominal growth of around 0.3% MoM. Industrial production should post a decent gain, based on a robust manufacturing ISM reading for the period, but there is the risk of disruption due to bad weather.

United Kingdom (James Smith)

- 4Q GDP (Thu): Having started strong, UK growth fizzled out in the second half of last year and it looks like final-quarter GDP was flat. The data should improve this year as the government's spending splurge comes through, but 2025 growth is likely to be significantly weaker than the 2% forecast the Office for Budget Responsibility set last year. Likely revisions are an added challenge for the Treasury's Spring Statement in March, where higher debt-interest costs have already eroded the government's already thin fiscal headroom.

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

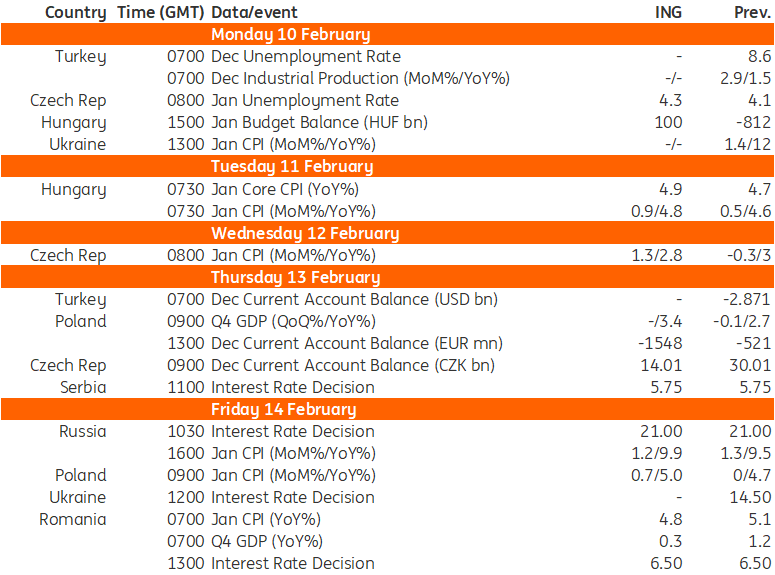

- Flash 4Q24 GDP (Thu): This should confirm that economic activity gained momentum towards the end of 2024 after a soft patch in in the third quarter. The preliminary estimate of 2024 economic growth implies the fourth quarter came in around 3.4% year-on-year after 2.7% YoY in the third. Household consumption improved, while fixed investment growth remained weak. The economic recovery is quoted by the National Bank of Poland's governor as one of the upside risks to inflation.

- January CPI (Fri): Inflation accelerated at the beginning of the year amid an increase in energy prices (higher distribution charges in natural gas bills) and more expensive fuels (gasoline & diesel). The CPI report will be preliminary and limited in scope (only the main categories unveiled) and data will be revised in March, when the StatOffice traditionally updates the CPI basket weights.

- December balance of payments (Thu): We forecast that imports rose faster than imports, translating into a sizeable trade deficit and, in turn, a negative current account balance. As a result, the 2024 external position was balanced (current account deficit at 0% of GDP). Domestic demand remains stronger than external demand and we expect the current account to turn slightly negative in 2025.

Hungary (Peter Virovacz)

- Inflation (Tue): January's inflation prints are always the most interesting, as they reflect firms' willingness to pass on rising costs to consumers. According to the latest surveys, price expectations in the retail and services sectors are booming. This partly reflects higher hard-currency input costs, the weaker forint, tax changes and rising wages. We expect headline inflation to be 0.9% and core inflation to be 0.6% on a monthly basis. So the story will be more than just some tax changes and fuel price increases. With such a strong monthly repricing, both headline and core inflation will be close to 5% YoY. That strength suggests that the recent hawkish shift in the central bank's forward guidance will be vindicated by the data.

Romania (Valentin Tataru)

- Inflation (Fri): We anticipate a marginal deceleration of the inflation rate to 4.8% in January from 5.1% in December last year, as the relatively important disinflationary base effects of non-food items have been offset by the recent increase in oil and energy prices. This will likely be well above central bank projections from last year but should not come as a surprise for markets.

- GDP (Fri): On the economic growth front, fourth quarter flash GDP should show a marginal annual economic expansion, taking the full 2024 growth somewhere close to, but likely below 1.0%.

- Interest rates (Fri): With inflation likely to remain sticky around 5.0% throughout 2025, GDP growth well below potential and a still blurry outlook for the fiscal developments, the National Bank of Romania seems prone to keep its key rate at 6.50% at least through the second quarter of the year, while maintaining the relative stability of the FX rate.

Czech Republic (David Havrlant)

- Unemployment (Mon): The unemployment rate likely increased at the beginning of the year, reflecting continued layoffs in manufacturing and seasonal effects as some tourism-related services lay low for winter. The rebound in construction likely did not fully offset these dampening effects on employment.

- Inflation (Wed): The statistical office is about to confirm an inflation slowdown in January, as suggested in its flash estimate. Meanwhile, the full scope of the consumer basket will enable the calculation of the Czech National Bank's inflation breakdown. We see potent food price growth, muted regulated prices due to lower electricity end prices, and slightly higher core inflation.

- Current account (Thu): The current account surplus likely deteriorated at year-end as imports for Christmas shopping gained traction. At the same time, continued weakness in the eurozone economy and malaise in Germany’s manufacturing base restrained Czech exports.

Key events in developed markets next week

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article