THINK Ahead: How to (not) spot a recession

There’s a lot of data next week. A lot of it won’t look good. But does that mean imminent recession? Not necessarily, argues James Smith. But hey, what do economists know about these things?

How (not) to spot a recession

What’s the probability of a recession? It’s a question we’re getting asked a lot, which is ironic really, given that we economists are famously… not very good at predicting recessions. That thing about “predicting nine out of the last five” is probably being generous.

So it might surprise you that I’m not about to predict the tenth. Recession isn’t our team’s base case on either side of the Atlantic, though I think we’d concede it’s not a high-conviction call.

Much, unsurprisingly, depends on whether China tariffs are rolled back over the coming weeks, and more importantly, by how much. Reducing those rates to 50-60% from the current eyewatering 145%, as has been touted in the press, might not actually change the picture a great deal. The majority of Chinese imports would still look uneconomical, and American firms would still be highly incentivised to find substitutes from elsewhere, with all the supply chain complexity that brings with it. Lynn Song has a nice explainer here.

Suffice to say, whatever happens, the impact is still going to be sizable. Expect to see evidence of that in next week's packed data calendar. But watch out! That also means plenty of opportunities to spot a recession where the isn’t one.

Take manufacturing. Next week’s ISM survey will serve as a reminder of the perilous situation the sector now finds itself in. It's not looked great since the immediate aftermath of Covid. And back then, when the manufacturing surveys started to fall, talk of a recession began to rise rapidly. Yet the economy powered on regardless. It was a reminder that manufacturing simply isn’t the dominant economic force in the US that it once was.

That pandemic comparison may seem particularly pertinent now, given all the talk of empty shelves and supply bottlenecks today. But it's not a perfect analogy. Crucially, that was an economy that was propelled by pandemic-era stimulus, and the insatiable demand for services that came with it, both of which have long since gone away. With savings and confidence down and delinquencies up, the consumer is less well-positioned to absorb the costs of supply chain disruption this time around.

If we're honest though, most of that has been true for a while, and we've all learned the hard way that you underestimate the US consumer at your peril.

If the past couple of years have taught us anything, it’s that households just aren’t as sensitive to higher rates as they once were. Or at least, as James Knightley often reminds us, even if lower-income households were getting squeezed, the top 20% had plenty of firepower to keep spending growing.

More than that, the mega rate hikes we saw in 2022 were essentially a massive stress test on the major economies. And with the possible exception of small banks, the system came out relatively unscathed. I bring this up because recessions are often fuelled by what economists like to call “imbalances”. Unsustainable pockets of debt, in other words, and generally that’s not the case today. Household and corporate balance sheets look OK.

As for next week though, there’s a more basic problem to contend with, which is that everything is skewed by frontloading. Everything from imports to retail has been affected by households and businesses trying to get in ahead of the tariffs. And given a lot of that was channelled into imports, James Knightley reckons first quarter growth, due next week, won't scrape in much above zero.

So if neither GDP, nor manufacturing, nor loan delinquencies, are particularly reliable recession metrics right now, what is? The answer is probably the jobs market. Recessions often start and end with shifts in unemployment, after all.

Even here though, there’s scope to be misled. March saw an alarming spike in layoff announcements, which were highly concentrated in government. And perhaps we’ll see more of it in next week’s April data from Challenger.

But it’s a bit like the manufacturing point earlier – is what’s happening in the public sector completely abstract from the private sector? Perhaps. Certainly, the jobless claims data, which doesn’t include government, doesn’t point to anything particularly worrisome.

Maybe it's a moot point if the tariffs start to put serious pressure on hiring elsewhere anyway. And that looks highly likely. James K reckons we should be keeping an eye on transport/logistics for early hints of stress, now that the frontloading is done and shipments are slowing down.

Perhaps then, the true sign we're in recession would be if we start to get negative payroll readings. That's not a position we're in yet, though James is expecting more muted jobs numbers next week. Assuming these come in consistently weaker as we head into the summer, then that's likely to be the catalyst for the Fed to start cutting rates again. Rising unemployment was what finally provoked a 50 basis-point rate cut last September.

That might sound like music to the ears of equity markets. It did last year, given that the rise in joblessness we saw last summer ultimately proved to be a false alarm. But I'm not feeling too reassured. Hiring is about as backward-looking an indicator as you can find, so were the numbers to suddenly turn much weaker, there's a clear risk of the Fed finding itself behind the curve. Particularly, if rapidly rising inflation holds it back from easing policy as quickly as it would like.

As I said at the start, that's not the place we think we'll end up. But it's a reminder that for all the false signals we have to contend with, the truth is, we often don't know we're in a recession until it's too late.

Happy weekend everyone!

THINK Ahead in developed markets

United States (James Knightley)

- Sentiment (Tue): It will be a huge week for US data, which is likely to intensify fears of recession in the months ahead. Tuesday’s Conference Board measure of consumer sentiment is set to fall sharply if the University of Michigan measure is anything to go by. Households are worried about the squeeze to spending power from tariff-induced price hikes, while the fear of joblessness and potential cuts to government entitlements is fuelling concerns about income. Overlay that with falling bond and equity prices, and declining wealth is another factor that is making households more nervous and more reluctant to spend.

- GDP (Wed): The result is going to be a very weak 1Q GDP report on Wednesday. We can’t rule out a contraction due to a surge in imports in the first three months of the year, as companies brought forward foreign purchases to get ahead of feared tariffs. However, March consumer spending and investment were probably just enough to keep growth in positive territory for now. That may not be the case in coming quarters.

- Labour market (Fri): Then on Friday we have the all-important April jobs report. Hirings are slowing due to uncertainty over the economic outlook, but so far, firings are few and far between. Nonetheless, this will translate into slower payrolls growth with the risk of another small rise in the unemployment rate as labour supply outstrips labour demand growth.

Canada (James Knightley)

- Canada’s election has been turned on its head thanks to Donald Trump’s comments on making Canada the 51st US state. Support for the opposition Conservative Party has collapsed while the Liberal Party has been reinvigorated by a change of leadership under Mark Carney, the former Governor of both the Bank of Canada and the Bank of England. Whoever wins faces the challenge of dealing with the economic fallout from a trade war, whereby three-quarters of Canada’s exports go to the US.

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

- Flash CPI (Wed): We forecast that in April, headline inflation moderated below 4.5% year-on-year from 4.9% YoY in March due to the higher reference base in April 2024 when VAT on food was restored. Core inflation most likely also moderated further. Along with declining wage growth and weaker economic activity in 1Q25, this should convince the Monetary Policy Council (MPC) to cut the National Bank of Poland's (NBP) policy rates in May, potentially even by 50bp.

- Manufacturing PMI (Fri): Purchasing managers probably downgraded their assessment of business conditions in manufacturing, but we expect that the main index was still above 50pts., pointing to slow improvement in domestic industry, despite external headwinds (low activity in Germany, uncertainty linked to future tariffs).

Hungary (Frantisek Taborsky)

- NBH Meeting (Tue): On Tuesday, we will see the first meeting of the National Bank of Hungary (NBH) since April's US “Liberation Day” and March inflation, which saw the first decline in the headline rate this year. Although a lot has happened since the March meeting, nothing is likely to change for the NBH in terms of its forward guidance, and rates are likely to remain unchanged at 6.50%.

- The Hungarian economy has been shifting in a dovish direction since the March NBH meeting, driven by lower inflation, government measures, and heightened downside risks to an already fragile economic outlook. However, we believe it is too early for any reversal in forward guidance. The governor has reiterated that the focus is on domestic inflation and warned of the inflationary impact of US tariffs, clearly signalling that rate cuts are off the table. But at least for now, we believe that the possibility of a rate hike may fade from the discussions given some stabilisation on the domestic front and reduced FX volatility. We continue to see rates unchanged this year and have the first rate cut in our forecast for March next year.

Czech Republic (David Havrlant)

- GDP (Wed): This year's first take on the overall economic performance is set to show continued economic expansion at a solid pace. While the detailed GDP breakdown will not be at hand, we see continued robust household spending and hope for some rebound in suppressed investment activity. The economy had a good start to the year, while the recent reshuffle of the global trade constellations and the undermined conviction about global growth prospects could act as a drag in subsequent quarters.

- PMI (Fri): The same factors will drag down the Manufacturing PMI in April, breaking the upward trend. Meanwhile, the fog surrounding the impact of global trade negotiations, including how the EU could shield itself from export dumping, is making the industrial base more cautious and may result in postponed investment.

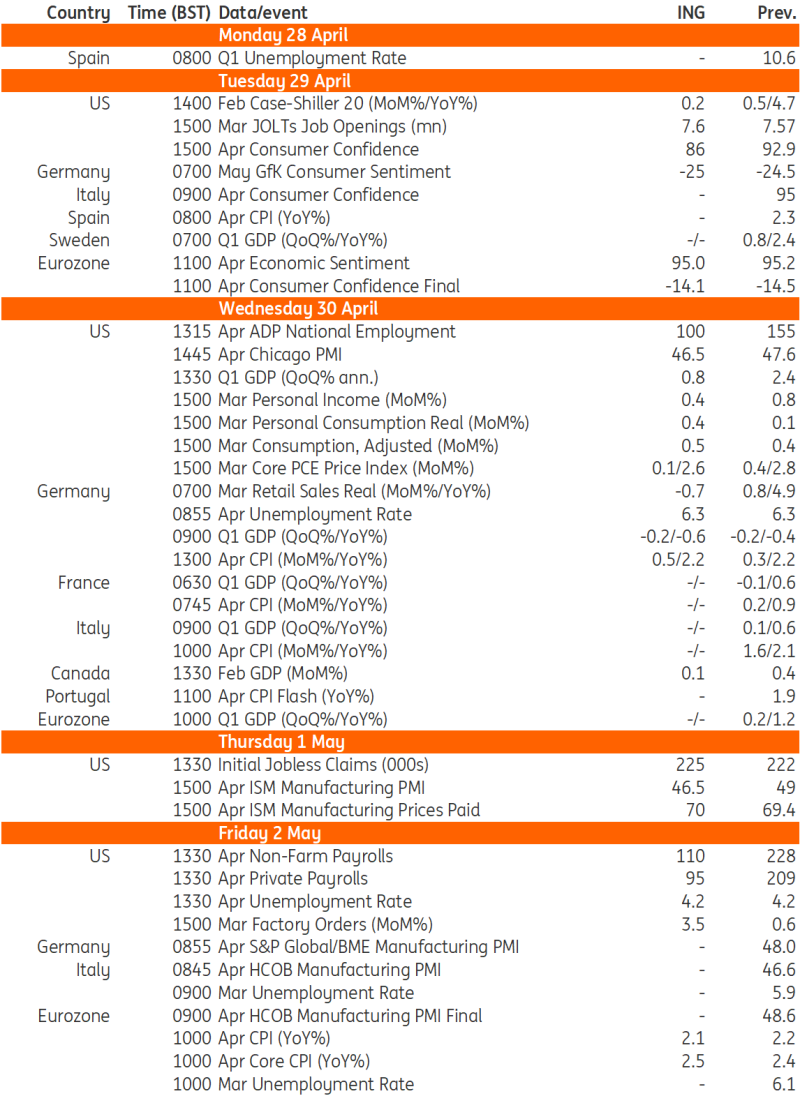

Key events in developed markets next week

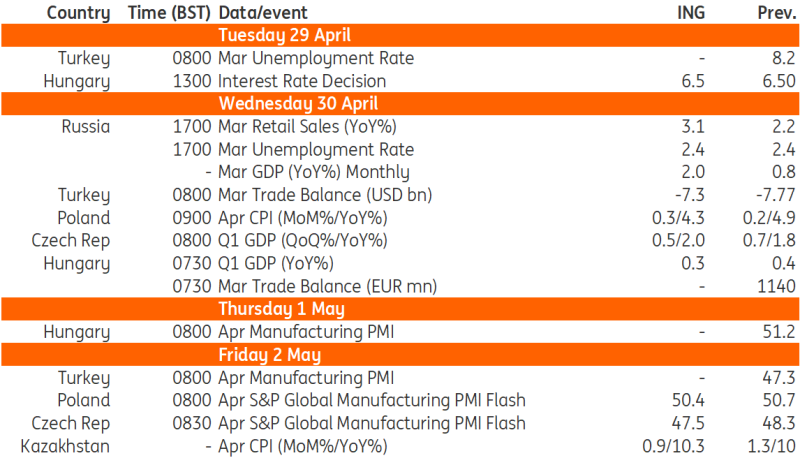

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article