THINK Ahead: Europe needs more than Cupid’s arrow to woo investors

Investors are flirting with Europe this Valentine's Day; stock markets are surging. But we know that Europe can be an unreliable life partner, and there's not much love for the continent's economic prospects. Still, ever the romantic, James Smith looks at how love could blossom again ahead of a big politics-fuelled week across the region

How Europe can rekindle its romance with investors

If you’d asked me on the eve of Donald Trump’s re-election in November where European stock markets would be right now, I, for one, wouldn’t have guessed they’d be surging. And yet, here we are. Germany’s DAX 40 is up a whopping 17% since election day.

Maybe I’m missing something; I’m just a simple economist, after all. But having spoken to a load of UK-based investors this week, there's still not a lot of love in the air when it comes to the European outlook.

Perhaps it’s the macro data, which hasn’t been as dreadful as first feared. Maybe ECB rate expectations have fallen. It could be renewed hope for 'peace' in Ukraine. It might even be the fact that US equities are now so expensive that even Europe now looks more appealing - the stronger dollar helps.

And this raises an interesting question: Are we past peak pessimism in Europe, and if not, how can we get there?

I put this question to Carsten, our Head of Macro, and it won’t surprise you that much hinges on President Trump and whether Europe can escape the worst of a US trade war. Do take a read of our team’s detailed look at the continent’s options. But to cut a long story short, Europe won’t escape tariffs, and its ability to do a quick deal is questionable.

Sure, there are quick wins. Lowering the tariff Europe charges on American-made cars is an obvious starting point. But ultimately, the US administration needs revenue, and its trade-related grievances with Europe appear deeply rooted. And it’s not at all clear that the continent’s leaders have much sway over American officials, as this week’s US-Russia talks appear to demonstrate.

The substance looks tricky, too. On LNG – a key interest of the Trump administration – Europe already sources 40% from the US. Is there really much scope to ramp that up, especially given the EU itself can’t speak on behalf of buyers?

Then there’s NATO, which is what a lot of this boils down to. Europe will more than likely commit to greater spending – perhaps upwards of 3% of GDP annually. As for where the money comes from, well, good question.

We don’t detect much appetite for pan-European borrowing right now, though Carsten reckons bolstering the European Defence Fund or using the European Investment Bank (EIB) could come back into fashion after the German elections. Either way, national governments will need to do the heavy lifting at a time when investors are already flapped about budget deficits (*cough* France).

But if Europe really is going to surprise us this year, then fiscal policy surely has to be part of the story. And let’s face it, only Germany has the room to go big. Much hinges on next week’s election outcome, but once a government is in place, Carsten reckons stimulus is coming. He points us towards Sunday’s TV debate for further clues on relaxing the infamous debt brake.

But forming a coalition is easier said than done. A negotiation involving several parties - more likely if the FDP and others meet the 5% electoral threshold – could take quite some time. You only need to look at Austria, where coalition talks are back to square one after several months, to see how challenging this process can be. No coalition means no meaningful German fiscal boost.

I’m guessing that, so far, I’ve not exactly filled you with optimism. So try this instead: how about a renaissance of the European consumer?

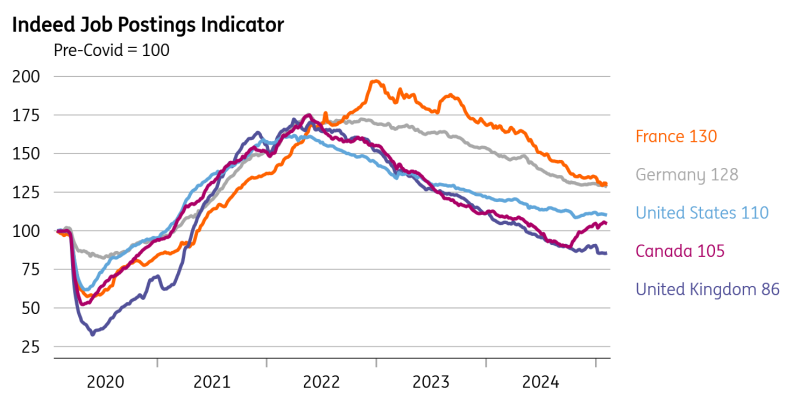

Wage growth is still north of 5%, where inflation is close to 2%. Yes, the ECB expects pay growth to slow considerably this year. But what if it doesn’t? After all, on some metrics at least, the European jobs market remains more buoyant than the US. Vacancies are still 30% up on pre-Covid levels in France and Germany, versus 10% in the US, according to the same set of data from the hiring agency Indeed.

The European savings ratio is also higher than average, whereas the US is below. Whether that buffer gets deployed is another question, listening to Carsten, given relatively weak consumer confidence. But if that changes, it could just be the tailwind Europe needs this year to escape the gloom.

I’m not saying that’s our base case, though. And despite what might be happening in stock markets, ‘peak pessimism’ in financial markets could still be yet to come. Our FX team expect EUR/USD to hit parity in Q2 before drifting higher thereafter. Their latest forecasts are out today. And my Rates Strategy colleagues think investors remain sensitive to the downside risks in Europe. They see a decent chance that markets could briefly price the ECB’s terminal rate as low as 1.5%, even if we don’t expect officials to take things quite as far as that in practice.

Whatever happens, if Europe's going to win back investors' hearts in the long run, good news needs to come from somewhere. Let's hope the equity folk know something we don't.

Chart of the week: European vacancies are still well above pre-Covid levels

THINK Ahead in developed markets

United States (James Knightley)

- The data calendar is light in a holiday-shortened week, meaning President Trump’s announcements/social media comments/media soundbites will be the most likely drivers of market sentiment. The momentum behind tariffs is building and markets continue to struggle to work out whether this will be more impactful on inflation or growth. In terms of the data it will hit the inflation figures first.

Eurozone (Bert Colijn)

- PMI (Fri): The eurozone PMIs increased more than expected in January but still only correspond to broad stagnation compared to late 2024. This should curb expectations about a strong improvement in growth at the start of the year. Inflation expectations are important as input costs have been on the rise again and while the ECB seems adamant that inflation is under control, businesses have recently been indicating that they are looking to price through to the consumer. The manufacturing sector remains under pressure as tariff concerns come at a time of already weak global demand for eurozone goods and increasing energy costs. Don’t expect a quick turnaround for the moment.

United Kingdom (James Smith)

- Jobs report (Tue): The unemployment is set to notch higher, though remember these figures are suffering from long-running quality issues. But the supposedly more reliable payroll numbers have been showing weaker private-sector hiring and we expect that to continue. Wage growth is proving stickier, but should come lower over coming months.

- Inflation (Wed): Services inflation is set to bounce back after some airfare distortions in December and that will drag overall headline CPI closer to 3%. Those headline numbers will edge higher later this year, though service-sector pressure is set to ease in the spring.

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

- Industry (Thu): Although recent PMI readings give some ground for optimism, industrial activity remains subdued and the ongoing recession in Germany is weighing on Polish manufacturing. Industrial output remains stagnant with annual changes swinging from positive to negative, depending on the calendar effect. We forecast a slightly negative reading for January. At the same time, PPI deflation is moderating, and we should see growth in producers’ prices in the coming months.

- Labour market (Thu): Wage growth fell below 10%YoY in December and we expect pay in the enterprise sector to continue rising at a single-digit pace in 2025 after three consecutive years of double-digit growth. The hike in the minimum wage this year was visibly lower than in the previous years, while lower inflation tames wage demands and weaker profit margins give less scope for pay increases. Employment continues to decline slightly as the working-age population shrinks, but unemployment remains at a record low. January's labour market report brings an update of the statistical sample of enterprises (firms employing at least 10 persons), generating more uncertainty regarding our employment forecast as it also reflects the trend from the previous year.

Czech Republic (David Havrlant)

- Inflation (Mon): Industrial price growth likely gained pace in January when compared on a monthly basis, driven by increasing wage costs and a weaker Koruna against the dollar. Meanwhile, annual growth softened at the beginning of the year due to a high comparison base with the preceding January. It is difficult for firms to pass the increasing input costs on to their customers, as the lukewarm demand across Europe combines with already stringent price competition.

- Sentiment (Fri): Consumer confidence likely marginally improved in January, correcting for the previous slump. However, the notion of economic difficulties for European industry means that the Czech export base will remain restrained, keeping a lid on consumer sentiment. Meanwhile, business confidence likely remained unchanged, flying further below its long-term average.

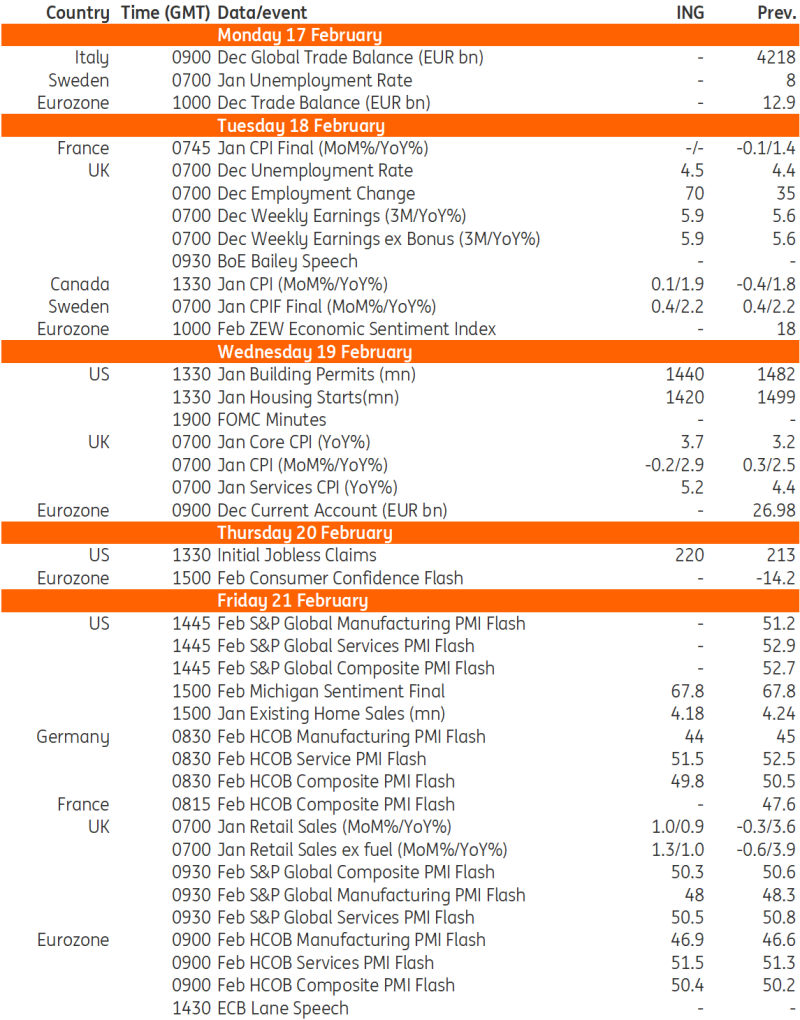

Key events in developed markets next week

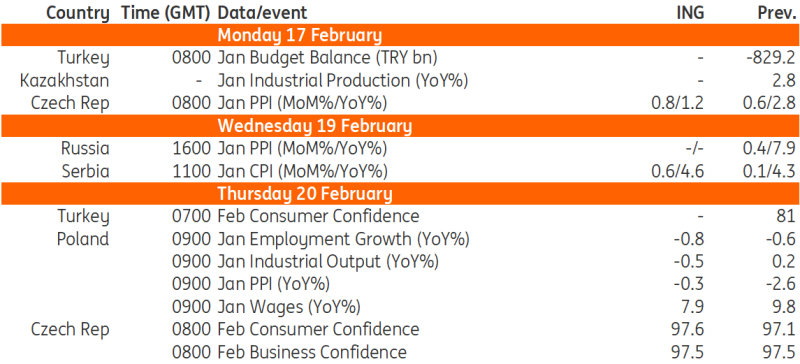

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article