THINK Ahead: Global markets and economies in Trump’s inauguration week

US markets are set to be in a state of limbo next week, but we'll find out if Europe's economy is recovering or not; don't hold your breath. Watch out for quite a few releases across central Europe as the world waits for Donald Trump's inauguration on Monday

THINK Ahead in developed markets

United States (James Knightley)

- It is a quiet week in the US with no major data reports of note and the Fed’s external communication blackout kicking in on Monday. As such, the markets will be in limbo ahead of the January 29 FOMC meeting. However, no one is expecting a rate cut on that occasion with less than 1bp of a 25bp cut priced by financial markets. Decent growth, a cooling but not collapsing jobs market, and elevated inflation prints mean the Federal Reserve is on pause for at least a couple of months after having cut the policy rate 100bp in the final months of 2024.

- Instead, the focus will be on politics and Donald Trump’s inauguration as the 47th President on Monday 20 January. Will he kick off his presidency looking to initiate tax cuts or will he focus his initial approach on implementing tariffs and immigration controls?

Eurozone (Bert Colijn)

- Sentiment (Tue) & PMIs (Fri): All eyes on survey indicators in the eurozone this week as consumer confidence and PMIs for January will shed light on whether the gloomy outlook for the start of the year gets confirmed. The PMI has not been above 50 – the neutral level – since September, which leads us to believe that the sluggish growth pace of the first three quarters of 2024 is too ambitious for the winter months.

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

- Data dump (Wed): The December set of data from the real economy should point to continued, albeit gradual, recovery of the Polish economy. Annual change in both industrial output and retail sales is expected to be somewhat stronger than in November amid a more favourable calendar (number of working days). Still, industrial output is projected to be stagnant YoY, while retail sales should continue rebounding after nose-diving in September. December sales figures should be supported by robust passenger car sales ahead of new EU regulations regarding emissions. We also expect double-digit growth of wages in the enterprise sector and a continued decline in employment. Registered unemployment most likely increased slightly on the back seasonal factors but remained close to all-time lows.

Hungary (Peter Virovacz)

- Labour market (Thu/Fri): Although we see lower wage growth in November, it will still be in double digits, ensuring continued positive real wage growth and rising household purchasing power. But it is another matter that there is no sign of a dramatic explosion in consumption as the propensity to save is still too high. One of the main reasons for consumers' lack of confidence to spend is rising unemployment, where we see a slight deterioration in December.

Czech Republic (David Havrlant)

- Confidence indicators (Fri): Consumer confidence has likely improved only marginally in January, with households still benefiting from continued real wage growth at the beginning of the year. That said, the piling and well-perceived unease in the industry accompanied by layoffs hampers a more optimistic assessment in the eyes of consumers. The lousy mood in business is set to enter a fourth calendar year in a row. Still, we expect the index to remain unchanged, as expectations of a possible turnaround linked to German elections and prospects of the EC entering into discussion with the automotive could ignite a spark of hope.

Turkey (Muhammet Mercan)

- Interest rates (Thu): Despite shifting expectations about Fed behavior going forward, we expect the CBT to continue rate cuts with another 250bp in January to 45% given recent positive signals about inflation outlook which will likely further increase real interest rate levels and lead to tightening in the financial conditions if the central bank does not act.

Azerbaijan & Uzbekistan (Dmitry Dolgin)

- The rate decision season in the Commonwealth of Independent States (CIS) continues with Azerbaijan on Wednesday and Uzbekistan on Thursday.

- Interest rates (Wed): We expect the Central Bank of Azerbaijan (CBRA to maintain the refinancing rate at 7.25%, as current CPI trends align closely with expectations. Full-year CPI growth was reported at 4.9% YoY, slightly below the recent official forecast of 5.1% but within the target range of 4% ±2. In the meantime, inflation in Azerbaijan is on an upward trajectory due to both supply and demand factors, potentially exerting upward pressure on rates in 2025.

- Interest rates (Thu): Similarly, the Central Bank of Uzbekistan (CBRU) is likely to keep the policy rate unchanged at 13.50%. Although domestic CPI growth slowed from the tariff-driven peaks of 10.5-10.6% YoY in mid-2024 to 9.8% YoY by year-end, this remains above the forecast range of 9.0-9.5% outlined in the recently updated monetary policy guidelines. In the near term, domestic inflationary risks remain elevated due to another round of household utility tariff increases, a loose fiscal stance, rising global food prices, continued depreciation of the soum, and high inflationary expectations among the population and businesses. While CPI and rates in Uzbekistan may trend downward in the longer run, we do not expect this to happen until mid-2025.

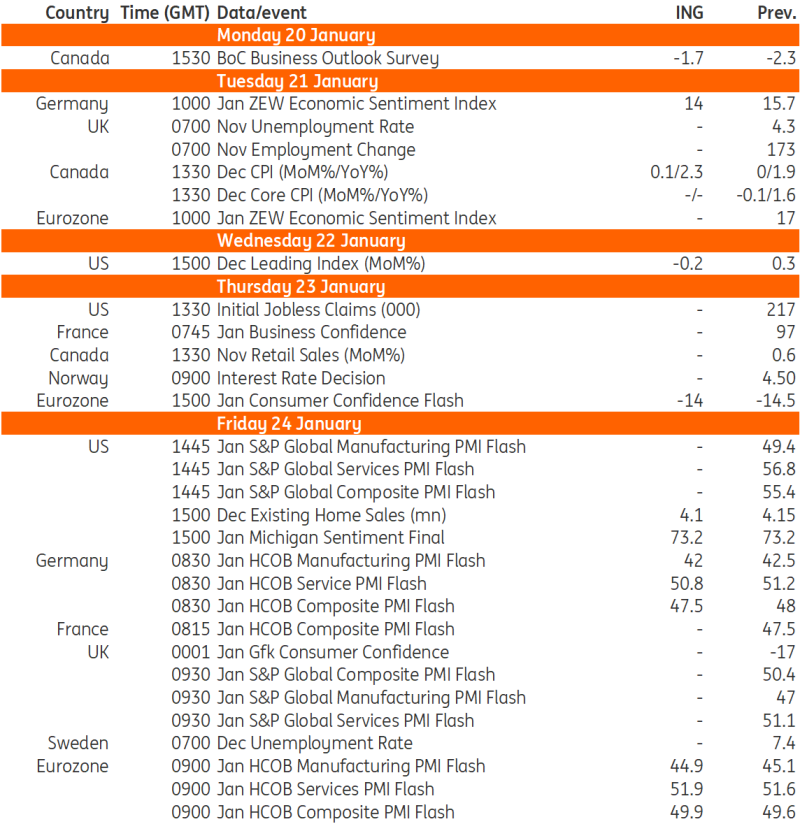

Key events in developed markets next week

Source: Refinitiv, ING

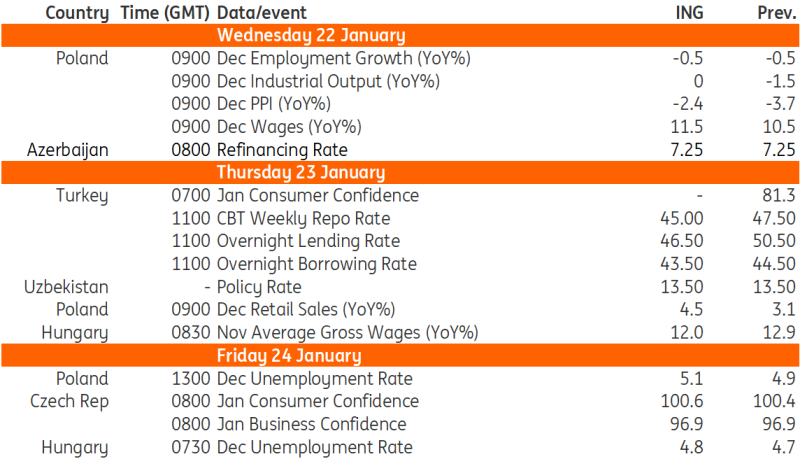

Key events in EMEA next week

Source: Refinitiv, ING

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article