The Netherlands: Relying on consumers’ purchasing power

- 13 January

- The Netherlands

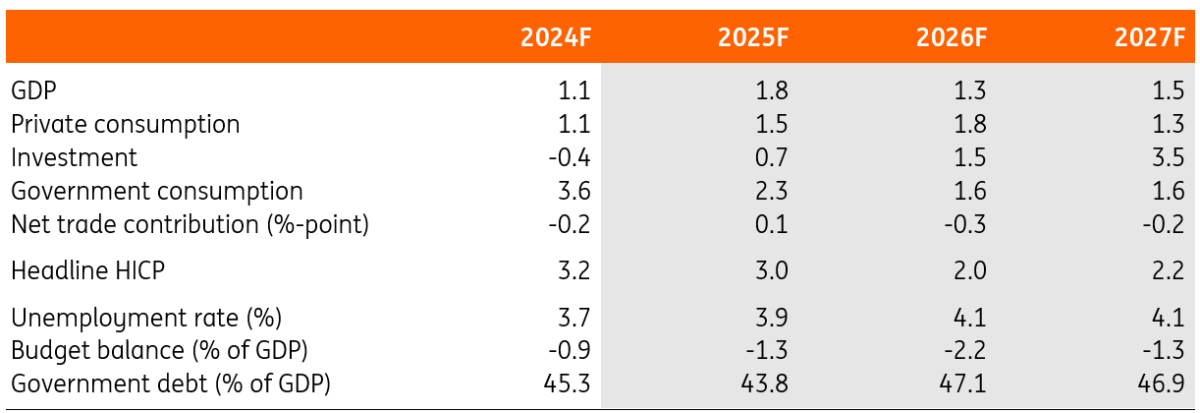

We expect the Dutch economy to retreat from 1.8% in 2025 to a more moderate 1.3% this year as exports and public consumption expand more slowly. Talks on a new government continue to drag on, so the economy is perhaps more reliant on households' willingness to spend

International developments will continue to play a crucial role in the open Dutch economy this year, as they did in 2025. While goods exports proved resilient last year despite the trade war, a stronger euro and rising geopolitical uncertainty, export growth is expected to slow in the coming year. The positive impact of front-loading ahead of trade barriers has largely dissipated, and secondary effects, such as intensified Chinese competition in non-US markets, are likely to increase. This is somewhat mitigated by the increased German infrastructure spending and higher European defence spending, providing support for international trade to expand, albeit at a moderate pace.

Weak private investment growth looking for decisive government action

Such public investment is also increasing within the Netherlands, but remains too modest to support an optimistic outlook for gross capital formation in 2026. Housing continues to be a bright spot; however, other private investment is expected to remain subdued. This weakness reflects not only low capacity utilisation in certain manufacturing sectors, but also persistent structural supply-side constraints, such as nitrogen-emission restrictions, electricity grid congestion, and labour shortages. Following the October general elections, businesses are closely watching the ongoing government formation process, hoping for a coalition that prioritises addressing these challenges. While any policy measures will take time to translate into tangible improvements in productive capacity, such an announcement could provide a near-term boost to business sentiment.

Private consumption should accelerate despite still high savings rate

Growth in public consumption is expected to slow compared to last year, reflecting the earlier frontloading of government measures aimed at supporting household purchasing power and the reduction in central government civil servants initiated by the previous administration. As a result, household consumption will remain the primary driver of growth in 2026. While we anticipate an acceleration in household spending, consumer confidence remains too subdued for it to fully offset the weaker expansion in public consumption and international trade. Consequently, GDP growth is projected to ease to 1.3% in 2026, down from 1.8% in 2025.

Household savings rates are expected to stay near recent highs, though a slight decline is possible as confidence continues to improve. Lower inflation should reinforce this trend, as high prices have been a key factor behind cautious spending. Importantly, household purchasing power will rise further in 2026, surpassing gains seen last year. This improvement will be particularly significant for pensioners, who benefit from the transition from a defined-benefit to a defined-contribution pension system, enabling faster indexation of benefits. Several pension funds implemented this change at the start of 2026, with more scheduled to follow in July 2026 and later the following year. Wage growth also continues to provide a solid boost to purchasing power, supported by a labour market that remains relatively tight.

Inflation just approaching the target

At the same time, HICP consumer price inflation is forecasted to approach the 2% target during 2026, after 3% in 2025. Selling price expectations of businesses remain elevated historically, suggesting that a final downward push requires a bit more time. Especially service inflation needs to come down further, but since wage hikes are expected to remain historically quite high, this remains a challenge for 2026. Inflation of food and housing is expected to be lower than in 2025, while energy costs are already falling and the euro exchange rate helps in keeping import inflation suppressed. But government policy is contributing to more inflation, as the VAT-rate on accommodation was raised from 9% to 21% and the fuel tax increased at the start of the year. Looking further ahead to 2027, an even larger increase of the fuel tax is still looming, which might bring inflation back just above the 2%-target that year.

The Dutch economy in a nutshell (%YoY)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more