Netherlands: Economic growth relies on the absence of new lockdowns

- 10 February 2022

- Eurozone Quarterly The Netherlands

Now that the lockdown has been eased, consumption is rebounding, allowing the Dutch economy to continue its expansion. GDP is forecast to grow by 3.3% in 2022 and 2.6% in 2023, which is supported by the fiscal policy of the new government that will keep elevated inflation from falling back to pre-pandemic levels

Fall in consumer spending has not stopped economic expansion

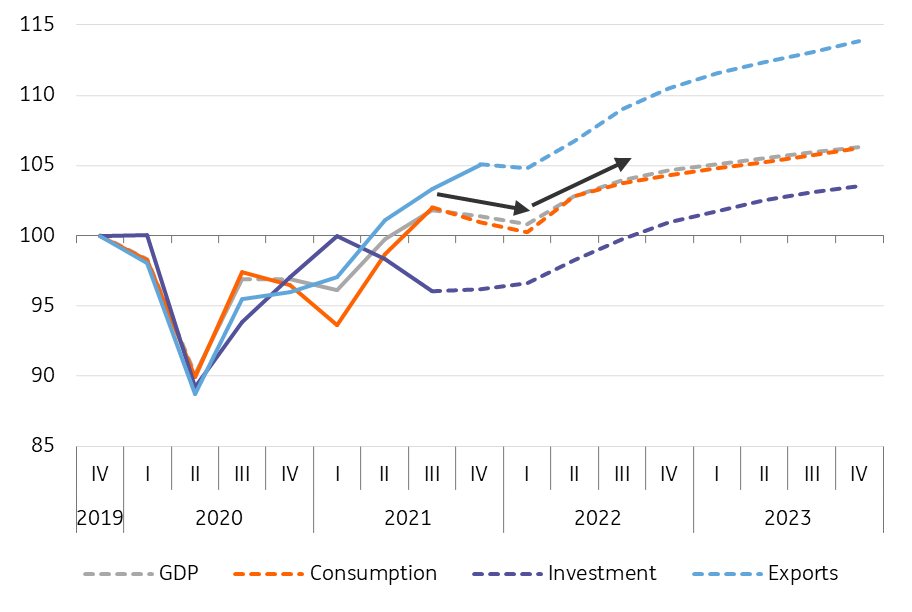

On 26 January 2022, shop opening hours were extended until 10pm, while bars and restaurants, cultural and sports venues were reopened again and events allowed. This heralded the end of the Netherlands' strict lockdown, in most cases still with distance, capacity and time restrictions. This recent lockdown caused a substantial fall in consumer spending, as observed in ING transaction data. First estimates suggest that the fall is half as large as during the lockdown of January 2021, while spending rebounded strongly at the end of January. This, combined with high energy and fuel inflation (+58% year-on-year in January 2022), implies decreasing household consumption in 4Q21 and 1Q22. As exports and investment are most likely less affected by the domestic surge in the pandemic, our gross domestic product (GDP) growth forecasts are only mildly negative (-0.4% and -0.6% respectively).

Consumption-driven setback until 1Q22; solid progress thereafter

Expenditures* as index where fourth quarter of 2019 = 100

In our base case with GDP growth of 3.3% for 2022, we assume the absence of new domestic lockdowns. This is a downward risk: uncertainty surrounding the pandemic is still significant. As available monthly data on industrial production, construction, retail sales and especially exports for the end of 2021 seems decent, a surprise to the upside can also not be fully ruled out. Overall, the outlook for the Dutch economy is uncertain but positive for the years ahead, not least because of the additional demand push of the policy measures of the coalition agreement.

Inflation substantial on energy and fuel in 2022, but also in 2023 due to policy changes

Inflation in the Netherlands is among the highest in the eurozone (7.6% year-on-year harmonised index of consumer prices change in January). In contrast to the US, wage-cost-push inflation is not yet part of the story. This is despite the fact that the Dutch labour market is very tight, with an unemployment rate of 3.8% in December (according to a revised surveying method of Statistics Netherlands).

Two-thirds of the price rise is driven by energy and fuel prices. Also, non-energy industrial goods and food are increasingly contributing to inflation on the back of elevated transportation costs, supply chain disruptions, energy cost inflation and higher world food prices. Volatile and hard-to-predict forward markets suggest that energy prices might stay high at least until the end of winter and fall thereafter, but will not necessarily return to pre-pandemic levels.

Inflation elevated both in 2022 and 2023

Change in harmonised index of consumer prices year-on-year in % and contributions in %-points

As energy inflation falls in our forecasts, the overall inflation rate will return to more normal levels (close to or below 2%) by the end of 2022. Nevertheless, we forecast inflation to stay close to 3% for the year 2023, following approximately 3.5% in 2022. This is due to specific policy changes in the Netherlands. Some stem from the ending of Covid-inspired support policies, while others result from a new coalition agreement:

- College tuition fees were halved, and these will be normalised in September 2022, which mostly affects 2023 inflation.

- Social housing corporation rents face a nominal freeze until 1 July 2022, which mostly affects 2023 inflation. Additionally, social housing rents will become more income-dependent, depressing rents for low income but raising them for higher incomes. We forecast that the net effect is more or less a normalisation of social rent increases.

- The normally liberalised rent sector currently faces temporary limited rent increase regulation (past inflation +1%-point) until 1 July 2024, which implies higher inflation in 2023 and 2024.

- The previous government lowered the energy tax (on gas and electricity) temporarily for 2022. The reversal in 2023 will have an upward effect on inflation for 2023. The new government plans to structurally lower the energy tax as of 2023, but this impact is much smaller.

- The new coalition will gradually increase the excise tax on a pack of cigarettes to €10.

- The new coalition will increase the excise tax on non-alcoholic drinks.

On top of the policy changes that directly affect inflation figures, the fiscal plans of the new government are strongly expansionary, generating upward price and wage pressure for the years to come. All in all, a positive outlook with the usual Covid uncertainty and unusually high inflation.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Eurozone Quarterly: Leaving the pandemic behind

- This bundle contains 11 Articles