The FX winners and losers from the oil price collapse

- 9 March 2020

- FX

The collapse in oil prices has severely punished high beta oil exporting FX globally. In the G10, the Norwegian krone is particularly vulnerable. The Canadian dollar is also exposed vs the outperforming yen, franc and euro. In emerging markets, the Colombian peso and Russian rouble look most vulnerable while CEE FX should be the relative outperformer

The sharp drop in oil prices and resulting grim outlook for crude in the months to come (see The OPEC+ break-up) sent shockwaves throughout markets. Here we look at the vulnerabilities of G10 and EM currencies (Figures 1 and 4) and potential winners and losers from the change in the oil prices dynamics, in an environment where the global growth outlook is being revised lower and risk assets are under heavy pressure.

Constructing the vulnerability scorecard

We look at three channels which are likely to impact G10 and EM currencies and create the vulnerability scorecard (Figures 1 and 4):

- Exposure to oil (based on IEA data), with currencies of oil exporting countries being vulnerable. Here, the fall in oil prices will have a negative effect on domestic economic prospects, the country’s terms of trade (which is one of the key variables within our BEER fair value model) and it could also have an impact on the domestic monetary set up (i.e. the potential for further easing which tends to be FX negative).

- Sensitivity to risk appetite, as those currencies with higher beta to global equities are likely to suffer, with higher beta oil exporters (NOK and RUB) in particular being at risk as the negative exposure to faltering risk assets exaggerates the currency’s downside.

- Current account balance. Here, the currencies of countries with a C/A deficit (and thus a constant need for external financing) are vulnerable to outflows in the current flight to quality environment.

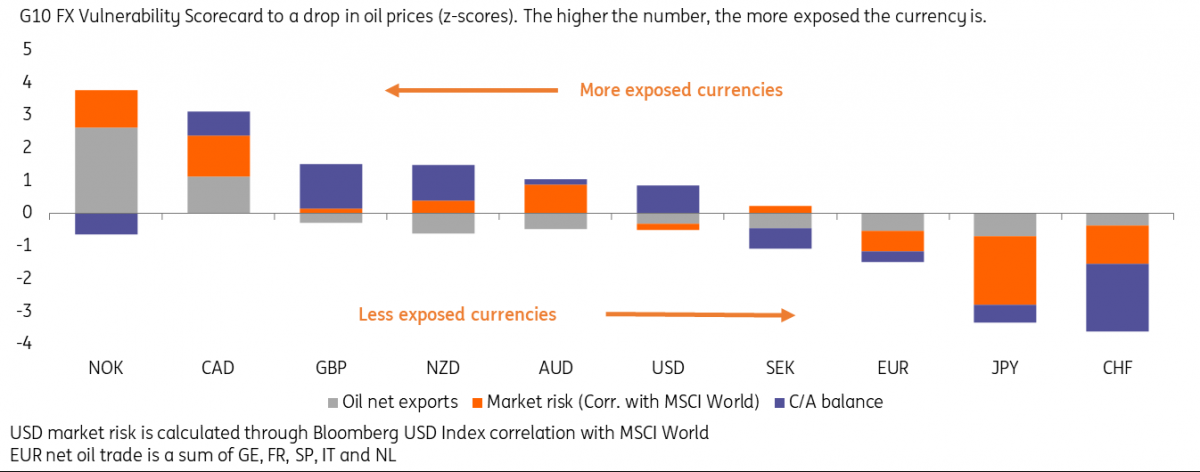

Fig. 1 - G10 Oil Vulnerability Scorecard

G10 FX: Running away from NOK

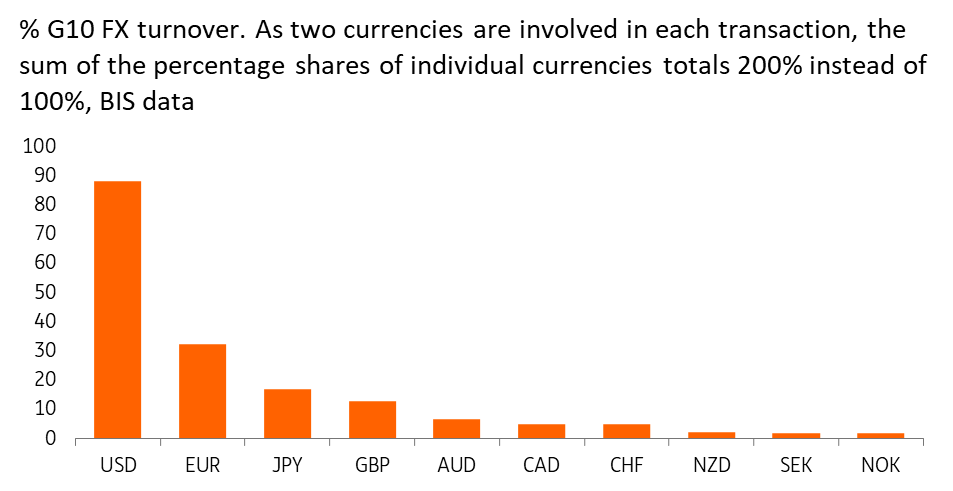

Unsurprisingly, and in line with the price action today, the oil exporters (NOK and CAD) look most vulnerable (Figure 1). In particular, we underscore NOK’s downside risk in the context of the low liquidity of the currency (based on the BIS data, NOK is the least liquid currency in the G10 FX space – Figure 2) which in times of stress introduces the risk of an exaggerated fall in the krone. Indeed, NOK’s meltdown vs EUR today provides a case in point.

Fig. 2 - Gauging G10 liquidity

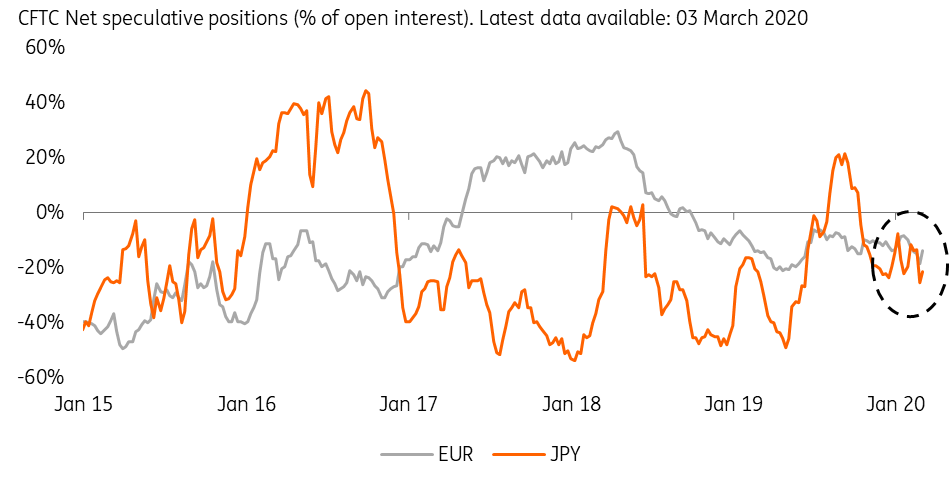

In contrast, the two usual safe havens of the Swiss franc and Japanese yen, as well as the euro, screen favourably. In terms of relative EUR prospects vs USD in the current risk-averse environment, the euro not only benefits from lower exposure to the oil price, but also from its meaningfully better current account position, limited scope for the European Central Bank to ease monetary policy aggressively and what have been persistent EUR/USD speculative shorts (Figure 3 – along with JPY).

Fig. 3 - EUR and JPY persistent short positioning

EM FX: Losing oil exports, winning CEE FX

Within the emerging markets, the Colombian peso and Russian rouble screen as the most vulnerable (Figure 4), with the rouble being heavily punished by its reliance on oil while the COP shows a more balanced negative exposure to each of the risk factors (oil, risk and current account). EM Asia and Central and Eastern European FX currencies look less vulnerable as these are net oil importers.

Fig. 4 - EM Oil Vulnerability Scorecard

In fact, we see CEE FX as winners in the current environment given their low beta / low yielding nature, low exposure to the oil price and, very importantly, a positive exposure to the rising EUR/USD - which is lifting all the boats in European FX. Also, we don’t see an urgent need for imminent aggressive emergency interest rate cuts in Central Europe, providing an additional anchor to CEE FX vs its EM peers globally.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more