The Eurozone: Going into overdrive

- 5 January 2018

The Eurozone recovery seems to be going into overdrive. For how long can that continue?

Eurozone indicators close to historical highs

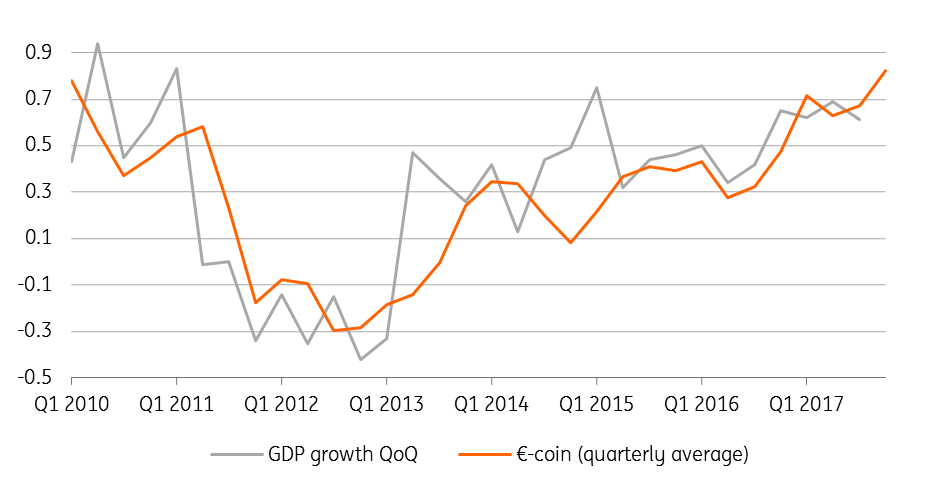

The Eurozone recovery seems to be going into overdrive. The €-coin indicator, a proxy for the underlying growth momentum, hit 0.91% in December, suggesting an above 3% annualised growth pace. While we doubt that this pace will be maintained throughout the year, we believe that GDP growth in 2018 will be at least as good as in 2017.

With employment rising 0.4% in the third quarter, consumer confidence in December hit its highest level since January 2001, boding well for consumer expenditure. Rising supply constraints and generous financing conditions are likely to continue to underpin the business investment revival. Notwithstanding the strong euro, export perspectives remain upbeat. The rebound in global investment is particularly helpful for Eurozone exports. No wonder that most cyclical indicators are close to historical highs. The PMI indicator for the manufacturing industry in December hit the highest level since the series started in mid-1997.

| +3% |

Eurozone annualised growth rate2018 growth at least as good as 2017 |

The political conundrum

True, politics could still cause upsets, but probably not enough to spoil the growth party, we believe. With the pro-independence parties still holding a majority after the regional elections in Catalonia, the problem is not going to be solved rapidly, though we don’t think that the Spanish economy will suffer significantly from the current stalemate. That said, some negative impact cannot be avoided. The budget for 2018 has still not been approved, as the Basque National Party is refusing to support the draft budget of Rajoy’s minority government, as long as the Catalan issues have not been settled.

In Germany, there is still no new government, which is quite unusual for the country. It is still unsure whether the SPD party members will give the green light to another grand coalition. The biggest problem that the current power vacuum creates is European, as in the current circumstances Chancellor Merkel doesn’t have a mandate to support. Emmanuel Macron’s ambitious reform plans for the Eurozone.

Finally, 4 March has been set as the date for the Italian general elections. For now, it looks likely that there will be no clear winner, making the formation of a workable coalition difficult, but we consider the likelihood of an anti-European coalition to be quite small (about 10%).

Eurozone growth pace continues to accelerate

Growth momentum and solid base effects

Of course, we cannot exclude sudden shocks in financial markets, which could also temper the growth momentum. Indeed, it would be a surprise if the current low volatility and depressed risk premia remained in place for the whole of the year. In that regard, it still looks wise to not to overdo the expectation of continuing above-potential growth. That said, we now believe that 2018 GDP growth will come out at an above-consensus 2.4%, on the back of a strong base effect and the current growth momentum.

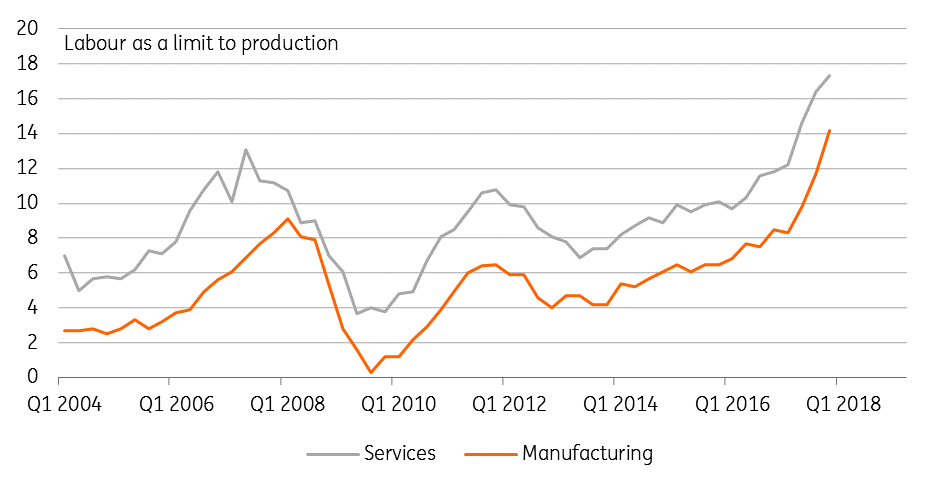

From the second half of the year growth is likely to start converging gradually towards the longer-term growth potential, which for the Eurozone is below 2%. With supply constraints getting more important, it looks as if wage growth will start to pick up in the course of 2018. In the PMI Manufacturing Survey businesses reported higher rates of inflation in both output prices and input costs as supply chain pressures increase, with average vendor lead times lengthening to one of the greatest extents on record. But even then, the European Central Bank’s consumer price inflation target is unlikely to be reached in 2018, so justifying its loose monetary policy.

However, on the back of the stronger growth and increasing inflation, the calls to end the quantitative easing (QE) bond-buying programme in September 2018 will grow louder. We maintain our belief in a short extension, but in December the net asset buying should have ended. Excess liquidity is likely to hit €2000 billion in the course of 2018 and start only to decline very slowly in 2019, keeping money markets interest rates in negative territory until the summer of 2019.

This article comes from our Monthly Economic Update. Download the full report here.

Labour could limit Eurozone production

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Where next for Europe in 2018?

- This bundle contains 5 Articles