The ECB’s Dashboard: Praet’s pivot pirouette

- 11 June 2018

We expect the European Central Bank to recalibrate its bond-buying programme on Thursday. But it will have to tread carefully

Scenario analysis: How to position for the ECB

Balancing act

Despite growing uncertainty around the strength of the eurozone recovery, little underlying inflationary pressure and possible further market turmoil, the European Central Bank seems determined to focus on long-term trends.

After a speech by ECB chief economist Peter Praet last week, the only question is how much detail the ECB will be willing to present. We still don’t think the central bank will easily give away flexibility and room for manoeuvre on quantitative easing in a situation where downside risks to the economic outlook have increased and political risks (be it from Italy or later this year from Brexit) could easily reemerge.

It is a close call between trying to buy more time with hawkish words and announcing explicit details. Given Praet’s comments, we expect the ECB to announce another recalibration of QE, i.e. an extension of QE at a reduced pace of €10 billion per month at least until December 2018.

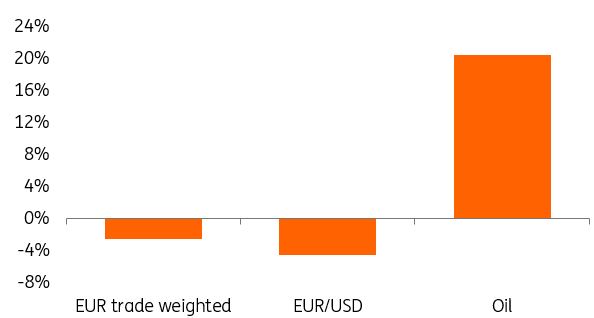

% increase since the ECB Meeting on 26 April 2018

Market reaction

What this means for FX markets: Slowing pace of QE to put a floor under EUR/USD.

The announcement of a lower pace of asset purchases over 4Q (from €30 billion to €10 billion) should be EUR/USD positive as (a) signalling-wise, it brings us closer to the eventual end of QE; (b) volume-wise, €10 billion per month is a limited amount.

Yet keeping the programme open-ended (i.e. the ECB will not commit to an end date) should mitigate the degree of EUR/USD upside. We thus don’t expect EUR/USD to break above the 1.20 level.

What this means for bond markets: Open-ended QE to dampen the immediate upside in rates.

Heading into the ECB meeting, rates remain depressed by lingering political risks surrounding Italy and ongoing fears of an escalation of trade tensions. Keeping net QE purchases open-ended should thus cap the immediate bearish reaction in rates.

However, a signal from the ECB that it remains undeterred in moving towards the exit should keep rates on course to rise back towards 0.70% over the summer.

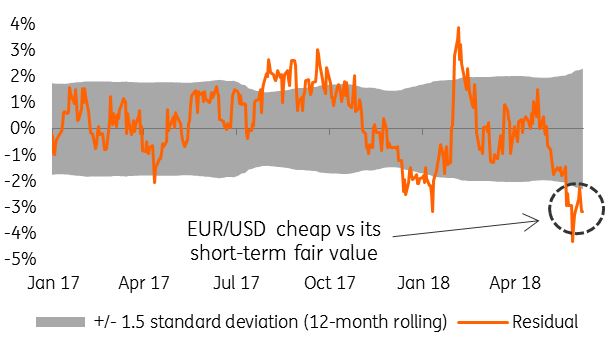

Residual between EUR/USD financial fair value and spot

Large and persistent misvaluation is a sign of a risk premium (as things other than normal drivers are affecting EUR/USD)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more