The Commodities Feed: Further pressure on the complex

Uncertainty over the path the Fed takes this year with monetary policy continues to weigh on risk assets, including commodities

Energy – OPEC sees strong oil demand

Oil came under pressure yesterday as broader markets continue to question the Fed’s path this year when it comes to cutting rates. This is particularly after US retail sales data for December came in above expectations yesterday. As a result, ICE Brent settled a little more than 0.5% lower. Shifting views on Fed action has been more than enough to offset concerns in the Red Sea. Another commercial vessel was attacked yesterday, taking the total tally so far this week to three. As a growing number of ships avoid the Red Sea, it is clearly disruptive to trade flows. However, for now, price action in oil suggests that the market is assuming we do not see an escalation in the situation.

According to Bloomberg, oil output in North Dakota has fallen further due to freezing weather conditions with output falling by 650-700k b/d, which is up from around 650k b/d earlier in the week. Although expectations are that the bulk of this production will return in the coming days.

US oil inventory numbers overnight from the API were bearish. US crude oil inventories increased by a marginal 483k barrels last week. However, products saw large builds once again with gasoline and distillate stocks growing by 4.86m barrels and 5.21m barrels respectively. The more widely followed EIA inventory report will be released later today.

OPEC released its latest monthly market report yesterday which included its first estimates for 2025. The group left its demand growth forecast for 2024 unchanged at 2.25m b/d, while for 2025, demand is forecast to grow by 1.85m b/d. As for supply, non-OPEC output is expected to grow by 1.34m b/d this year and 1.27m b/d in 2025. As a result, demand for OPEC oil in 2024 will be 28.5m b/d and 29m b/d in 2025. This is well above the 26.7m b/d OPEC produced in December (excluding Angola), which suggests that OPEC sees the market in a fairly large deficit this year.

On the calendar today, the IEA will release its latest monthly oil market report, which will include its latest 2024 outlook. The EIA will also release its weekly US oil inventory report, as well as its US natural gas storage report. Given the colder weather seen in the US, the market is expecting US gas storage to have fallen by around 165bcf over the last week, which would be above the 5-year average of around 126bcf.

Metals – China aluminium output hits record in 2023

Primary aluminium output in China increased 3.7% year-on-year to a record of 41.59 million tonnes in 2023, data from the National Bureau of Statistics (NBS) shows. December’s production was 3.59 million tonnes, up 4.9% year-on-year, but down on a daily basis as smelters in Yunnan reduced output in reaction to the province’s limited power supply during the dry season. This marked the third consecutive year that Yunnan smelters have reduced output during the dry season. Further cuts remain a possibility.

For steel, China’s output totalled 1.019 billion tonnes, slightly higher than the 1.013 billion tonnes reached in 2022, data from the NBS shows. December’s total of 67.44 million tonnes was a fall of 11.4% versus the November figure, and the fifth consecutive month with a decrease. December’s figure was the lowest monthly total in six years. There is still uncertainty around mandatory steel curbs weighing on the outlook for steel production. After China’s steel output climbed to a record of more than 1 billion tonnes in 2020, the government responded by ordering production cuts in each of the next two years to cut back on emissions and match supply with demand. However, given Beijing's concerns over economic growth, production cuts in 2023 were less stringent than in previous years.

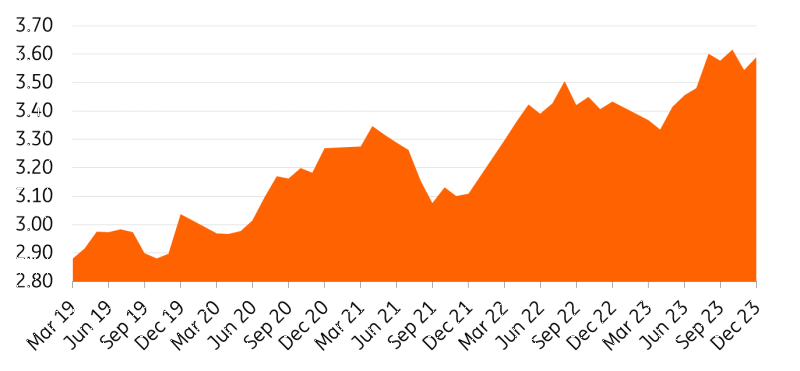

China primary aluminium output (m tonnes)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article