7 reasons why Europe can deal with a gas shock better than in 2022

- 11 March 2026

- Commodities, Food & Agri Energy

Events in the Persian Gulf and the resulting LNG supply disruptions will give many in Europe flashbacks to 2022. However, we believe Europe is better placed now to weather this supply shock

Persian Gulf energy supply shock sparks flashbacks to 2022

Europe had just about shaken off memories of the 2022 energy crisis. Global energy markets were set to be well supplied through 2026, suggesting weaker energy prices this year. But this view has been upended by developments in the Middle East. While the supply impact from the disruption in Persian Gulf energy flows is significant, particularly if we are to see prolonged supply issues, we do not think this is a repeat of 2022 for Europe - the impact is expected to be lower.

We do not believe European gas prices will trade to the peaks seen in 2022; global gas markets are relatively better supplied, while a large pipeline of LNG export capacity is coming onto the market in the years ahead. That said, clearly, how high prices go will ultimately depend on how long supply disruptions in the Middle East persist. Expectations that gas prices will not reach the elevated levels of 2022 also suggest that electricity prices will be more contained.

In addition, Europe is relatively less exposed to the gas market, with the region having reduced its reliance. EU gas demand is 16% below pre-Russia-Ukraine war levels. Furthermore, the EU would have learnt invaluable lessons from the 2022 energy crisis, which leaves it better prepared to navigate any future supply shocks.

Here are seven reasons why we believe things are different this time for Europe.

The current energy shock should be temporary, 2022 was more structural for Europe

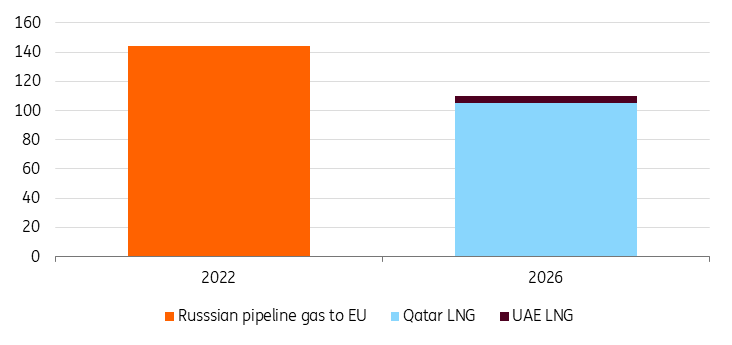

The amount of LNG disrupted by developments in the Persian Gulf is significant. Between Qatar and the UAE, roughly 110bcm of annual supply is currently affected, which is 20% of global LNG trade. The volumes are significant but still less than the 144bcm of Russian pipeline gas, which was at risk heading into 2022.

However, the key difference is that current supply disruptions are temporary. Yes, there is plenty of uncertainty about the duration of the disruption, but ultimately, supply will return. This is different from 2022, when the market was of the view that we were set to see a more structural shift in gas supply to Europe. Essentially, the market had the view that a loss in Russian gas supply would be final, with a very low probability that flows would ever resume.

2022 vs. 2026 gas supply disruptions-annual supply (bcm)

Europe faced a perfect storm in 2022

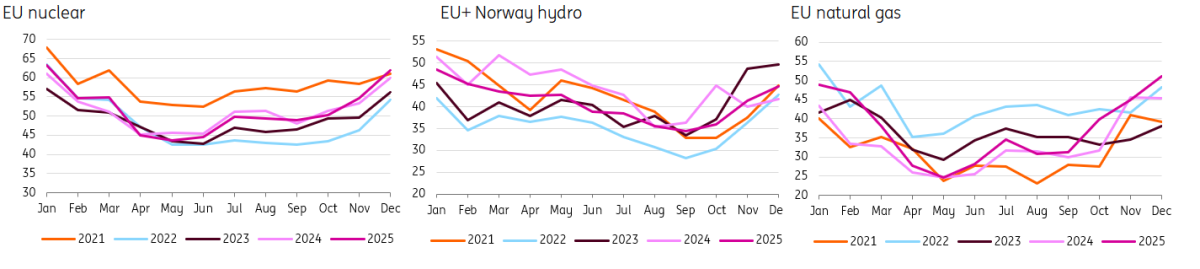

In 2022, it seemed that almost everything that could go wrong for Europe did. Not only was the region dealing with reduced gas flows from Russia, there was also uncertainty over further losses. But other sources of electricity generation also struggled.

The largest nuclear power producer in the EU, France, saw significant maintenance work carried out through much of the year due to corrosion issues, resulting in annual nuclear output falling to its lowest level since 1988 and 30% below the annual average over the last 20 years. Similarly, Europe was also having to deal with lower-than-usual hydro power output.

Lower nuclear and hydro meant the power sector had to lean more heavily on fossil fuels, including natural gas, for generation needs, at a time of significant supply uncertainty.

European power generation by selected source (TWh)

Installed renewables capacity in the EU has grown significantly

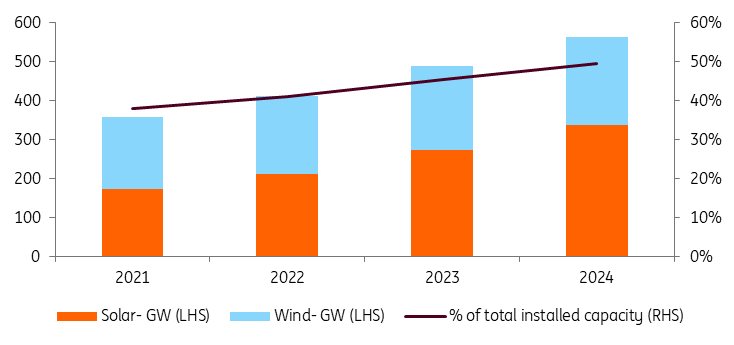

Renewables' capacity in the EU has also grown strongly since the end of 2021. Bloomberg New Energy Finance numbers show that installed capacity for solar and wind has surged by 57% between 2021 and 2024. Estimates suggest that capacity increased by a further 15% in 2025. This would have been supported by REPowerEU, the European Commission’s plan to support energy transition and reduce the EU’s dependence on Russian fossil fuels.

However, under the marginal pricing system in electricity markets, the highest-cost source of power sets the price, which is usually natural gas. This means stronger gas prices can still cause electricity prices to surge, even if gas power generation makes up a smaller part of the electricity mix. The European Commission is considering reviewing the system, though several member countries are pushing back against changing the current mechanism.

Installed renewables capacity has grown in the EU

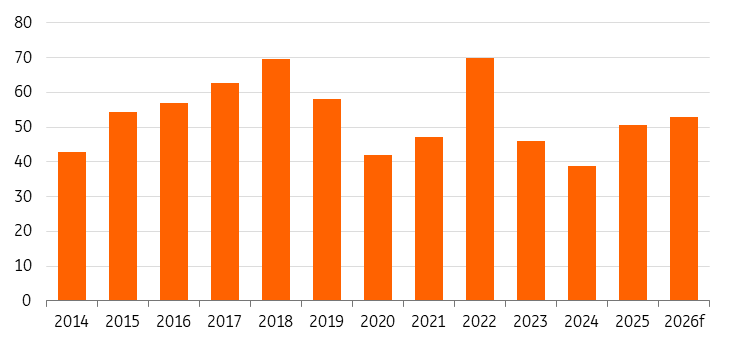

Europe has reduced its reliance on natural gas since 2022

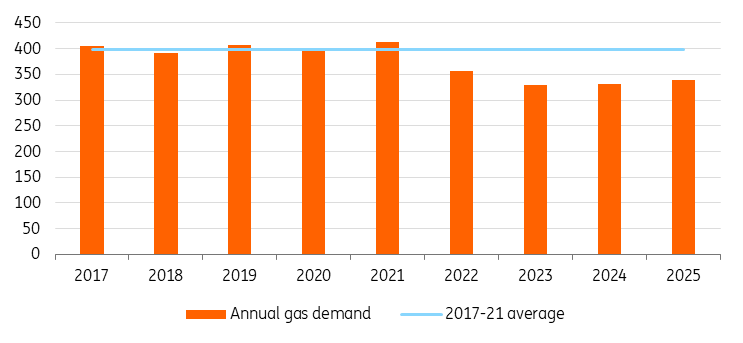

From a demand perspective, the EU is also less reliant on natural gas supplies than it was prior to Russia’s invasion of Ukraine. We have seen permanent demand destruction when it comes to natural gas following the energy crisis of 2022, and while gas demand has slowly edged higher since 2023, it is still 16% below 2017-21 levels.

The permanent loss in demand from the EU would be partly due to the ambitions of REPowerEU, but also to the lack of competitiveness of energy-intensive industries in Europe because of high energy prices. For example, the chemicals sector has seen production capacity fall by 9% since 2022.

EU natural gas demand well below pre-Russia-Ukraine levels (bcm)

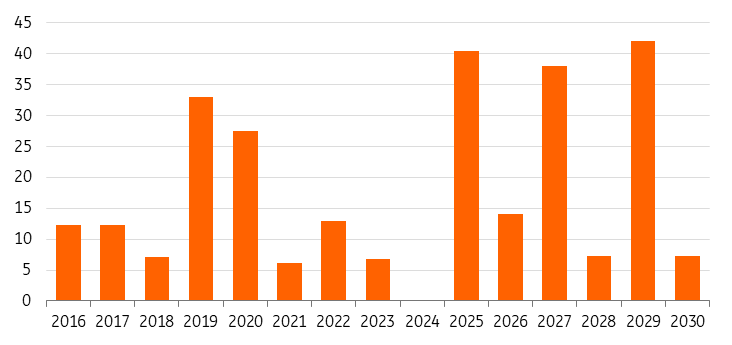

The pipeline of LNG export capacity is significant, a big change from 2022

The shift we saw from Europe in 2022 away from Russian pipeline gas towards LNG tightened up the global market significantly, leaving very little slack in the system and increasing competition for spot LNG supply. In addition, the pipeline of new LNG export capacity from the US was very thin around that time. Between 2021 and 2023, only around 25bcm of new capacity came online.

Currently, the loss of Persian Gulf LNG supply leaves the market tight. However, we do have a lot more LNG supply ramping up. Once again, this is driven by the US, where between 2025 and 2027, we have 93bcm of capacity additions. There is also around 42 bcm of capacity set to start up from Qatar by 2027. Although developments in the Persian Gulf mean that some of this capacity, which was set to start up in late 2026, will likely be pushed into 2027.

Significant US LNG export capacity additions in the years ahead (bcm)

Europe has learnt a significant amount from the 2022 energy crisis (we hope)

One of the key drivers behind the surge in European natural gas prices in 2022 was the rush by European buyers to secure supplies, essentially buying gas at any cost. This led to the EU seeing significant net injections through 2022, in the region of 70bcm, compared to a 2017-21 average of around 55bcm. This was to ensure that the EU hit its 90% storage target by 1 November.

The EU has learnt important lessons from the 2022 energy crisis, and we are unlikely to see European buyers chasing the market higher to the degree we saw to ensure supply. Already in 2025, the EU made storage targets more flexible. While the 90% storage target remains, it can be achieved between 1 October and 1 December, and in unfavourable conditions, it could be as low as 75%.

EU net injections in 2022 hit record levels, unlikely to see a repeat in 2026 (bcm)

Joint gas purchasing should reduce internal competition

One of the issues in 2022 was not only that Europe was having to compete with other regions for LNG supplies, but European buyers were competing with each other for supply, which only added further upside to European gas prices.

As a result, the EU launched AggregateEU in April 2023, which essentially led to a more coordinated approach to gas buying; EU gas demand was pooled and then matched with supply offers. According to the EU, between April 2023 and March 2025, close to 100bcm of gas demand was matched with supply through the platform. However, this does not mean that European buyers bought this amount of gas, given that bilateral negotiations would have taken place outside the platform after matching.

The European Commission sees it as a useful tool in pooling demand, reducing price volatility, increasing bargaining power and reducing internal competition for supplies, given that the mechanism is now permanent, and since July 2025, it has operated under the EU Energy and Raw Materials Platform.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more