The 2022 Polish budget is less expansionary than expected

- 25 August 2021

- Poland

Strong domestic activity and spending limits will reduce the deficit and limit borrowing needs but higher off-budget spending remains a risk. The government may decide to finance the investments part of the Polish Deal via the EU recovery fund

The draft budget for 2022 doesn't raise eyebrows

If we were to describe the Polish draft budget in one word, we would call it cautious.

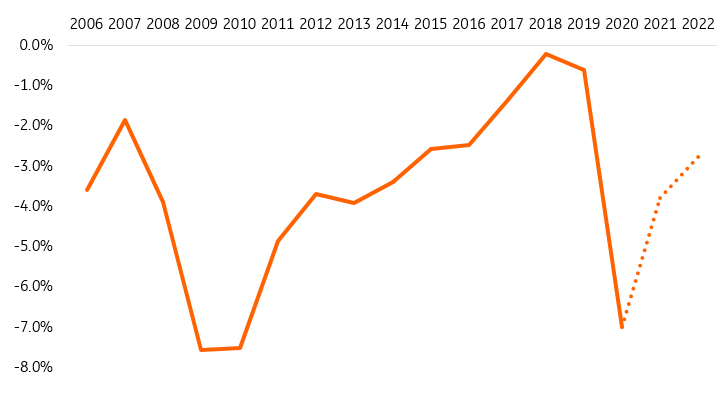

The deficit of the general government is assumed to fall 2.8% of GDP in 2022 - less than what we forecasted two months ago (3.5% of GDP) because we assumed some cost of the investments package from “Polish Deal”. It was related to BGK Strategic Investments Program, which was set to reach PLN100bn in three years – according to prime minister M.Morawiecki. The draft budget for next year presented yesterday seems to omit this element of the Polish Deal.

The tax revenues planned for 2022 are not overly optimistic, especially given that we see the potential for higher economic growth (5.0% YoY against 4.6%) and higher CPI inflation (3.8% against 3.3%) than assumed in the budget bill. The effective rates of VAT, excise duty, and CIT are similar to this year's, and the income from PIT includes the costs of the tax changes from the Polish Deal (increase in tax-free income and higher income threshold for second tax bracket).

Thus, we see no major threats to the execution of the budget bill in terms of tax revenues and expenditure of the central budget itself, unless new expenditure projects appear.

The deficit of general government in Poland

2021 deficit to be well below the original plan

Apart from the budget bill for 2022, the finance ministry has also revised it expectations for 2021 budget.

The deficit of central government is set to reach only PLN13bn (0.5% of GDP) against the originally planned PLN82.3bn. This would mean that the borrowing needs for 2021 are already fully covered, and the pre-financing for next year is well advanced (approx. 10%). This limits the supply of Polish government bonds and should support their valuations.

Risks to public finances are on the expenditure side

At the same time, we believe that non-budgetary expenses may turn out to be underestimated, e.g. under the Strategic Investments Program of the Polish Deal.

This would translate into a higher deficit of the entire public finance sector and the continuation of high issues of BGK bonds next year. The government may also use EU Recovery Fund for this purpose, but this would limit the fiscal impulse next year to support economic growth (compared to our and market’s expectations based on the government’s announcement so far).

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more