Thailand’s GDP contraction moderates in 4Q20

- 15 February 2021

- Thailand

But the Thai economy isn’t out of the woods just yet. The resurgent Covid-19 pandemic since December and tighter movement restrictions have set it off to a weak start to 2021, while tourists are set to stay at home for much of this year

| -4.2% |

4Q20 GDP contractionyear-on-year |

| Lower than expected | |

Better-than-expected 4Q GDP

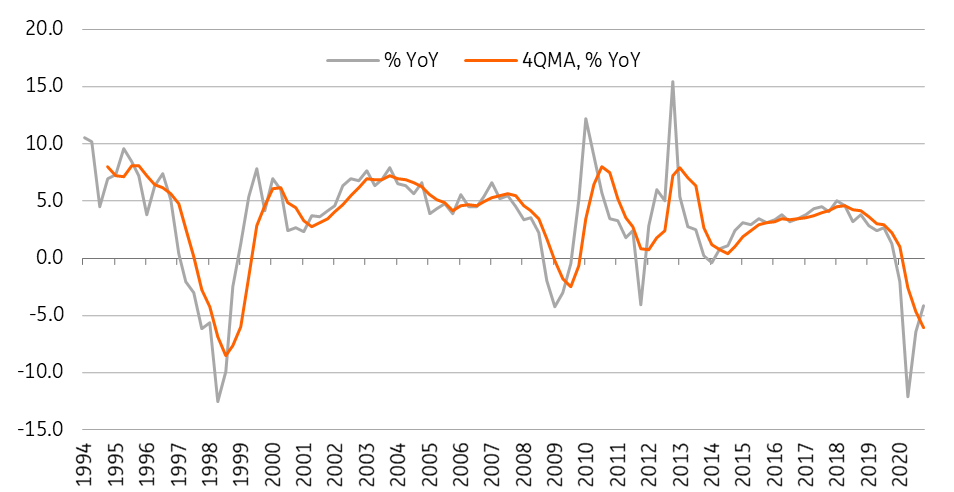

Released today, Thailand’s GDP posted a -4.2% year-on-year contraction in the final quarter of 2020. This was a slightly better outcome than our -4.7% YoY forecast and the market expectation of an over 5% GDP fall for the period. Yes, this is an improvement over a -6.4% GDP fall in 3Q20, though a sharp slowdown in quarter-on-quarter growth, to 1.3% in 4Q from 6.5% in 3Q, underscored an anaemic economic recovery.

This brings the full-year 2020 GDP contraction to -6.1% YoY, the worst since the -7.6% plunge in 1998 during the Asian crisis.

2020 was the worst year for the economy since the Asian crisis

More severe tourism dent

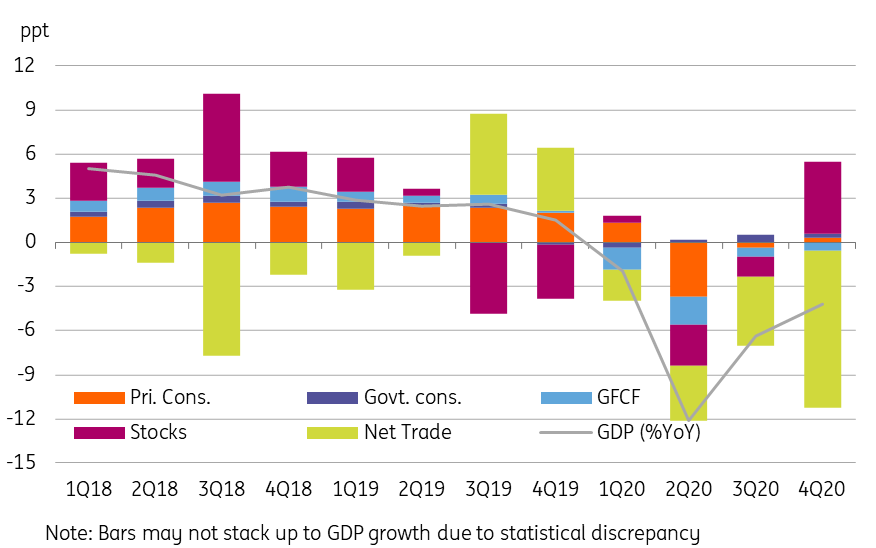

Among the main GDP components, net trade turned out to be the biggest drag on headline growth. It shaved off -10.6 percentage point (ppt) off the year-on-year GDP growth. It’s not a surprise, however. Even as merchandise exports recovered to a smaller contraction than in 3Q, the standstill tourism sector was a big hit to services exports, pulling total goods and services exports down by more than 21% YoY in 4Q, while imports shrank by only 7%. This aligns with a significant fall in the current account surplus in 4Q from a year ago.

The standstill tourism sector proved to be a big hit to services and headline GDP .

Inventory re-stocking picked up some slack from net trade, contributing +4.9ppt to GDP growth, while a 0.6ppt subtraction from fixed capital formation countered the +0.3ppt contributions from each of private and government consumption.

On the industry side, growth rates of agriculture and manufacturing output improved but services continued to lag behind. Transport and accommodation, with over 21% YoY and 35% plunges respectively, highlight the impact of tourism.

What's holding back the recovery?

2021 off to weak start

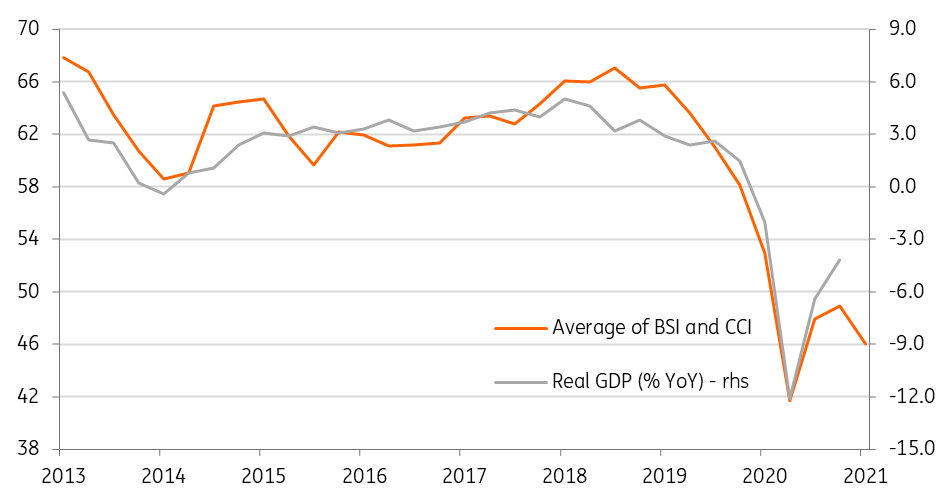

The significant surge in Covid-19 cases since December and tighter movement restrictions likely stalled the recovery this quarter. The forward-looking confidence indicators for January – the Business Sentiment Index (BSI) and the Consumer Confidence Index (CCI) – foreshadow an intensification of the negative GDP trend in the current quarter, subjecting our forecast of another -3.5% YoY GDP fall in 1Q21 to downside risk.

The low base year effect may return GDP growth to positive territory in 2Q21. However, without additional policy support this year the recovery is going to be painfully slow, in our view.

More than policy stimulus, what the Thai economy needs is the return of tourists.

More than policy stimulus, what the Thai economy needs is the return of tourists. The pandemic continues to wreak havoc. The National Economic and Social Development Council, the government’s economic planning agency, has just announced a cut to its forecast of tourist arrivals in 2021 to 3.2 million from 5 million earlier. This is still optimistic, especially with ongoing travel restrictions lasting through much of this year.

The NESDC forecasts 2.5% to 3.5% GDP growth in 2021, also a sharp downgrade from the 3.5% to 4.5% previous range. We maintain our 2.8% growth forecast for this year.

Resurgent pandemic dents confidence and GDP growth

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 16 February 2021

- This bundle contains 4 Articles