Weak Thai economy prompts downgrade of Asia’s weakest currency

- 31 March 2021

- Thailand

Thailand's baht ended 1Q21 as Asia’s weakest currency. We think it is prone to further weakness ahead as multiple waves and variants of Covid-19 globally delay the tourism recovery. We now see the USD/THB trading up to 31.90 by the end of 2Q21, before some consolidation towards 31.30 by the end of the year

Persistently weak activity

For February, Thailand’s manufacturing production and balance of payments figures continue to paint a weak picture of this economy.

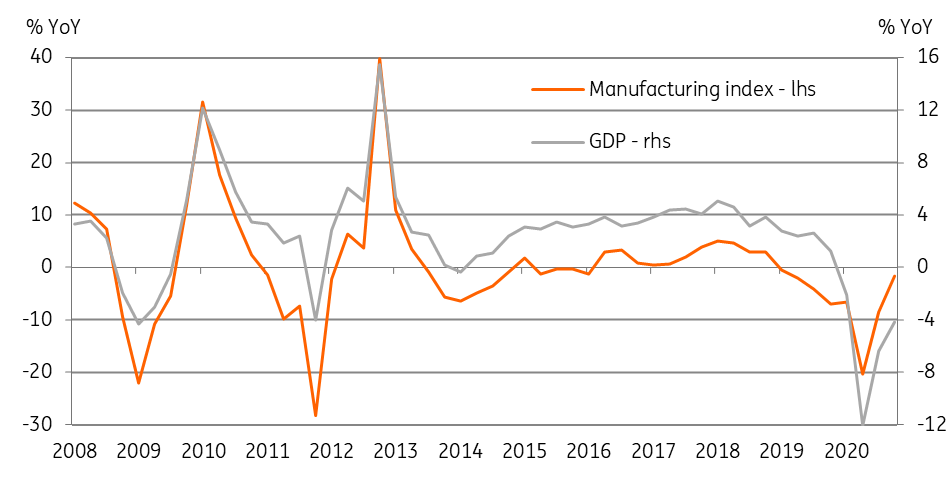

Extending its two-year-long negative growth streak further, the manufacturing production posted a -1.1% year-on-year contraction in February. The results weren't far off from our -1.8% YoY forecast for the month, though it was a significant disappointment for the consensus centred on a swing to positive growth. In slightly better news, January manufacturing contraction was revised up to -2.0% YoY from -2.8% initial print. This brings the average January-February output fall to -1.6% YoY.

The balance of payments data for February showed the current account posting the fourth consecutive month of deficit. The deficit widened to $1.07 billion in the last month from $673 million in January. Nothing surprising here given the continued weak merchandise trade balance and absence of the tourism-related services inflow.

The $1.7 billion cumulative current deficit in the first two months of 2021 contrasts sharply with the $8.8billion surplus in the same months of 2020.

An entrenched negative growth trend

These indicators reinforce a negative growth trend the Thai economy has been on since the last year.

We consider our forecast of -3.5% YoY GDP fall in 1Q21 at risk at more downside than an upside miss - and the same goes for our FY21 forecast of 2.8%.

While most Asian countries have been enjoying a vigorous export recovery since mid-2020, Thailand’s export growth has been stuck in negative territory (-1.2% YoY in 2M 2021). Although this explains some of the manufacturing weakness, the anaemic domestic demand also weighed down the output growth. Adding the lack of tourism problem to the services sector and we have one more quarter of GDP contraction on our hands. Meanwhile, a significant negative swing in the current account balance means that net trade prevailed as the key expenditure-side source of GDP contraction for the fifth straight quarter.

We consider our forecast of -3.5% YoY GDP fall in 1Q21 at risk at more downside than an upside miss - and the same goes for our FY21 forecast of 2.8%.

Where manufacturing goes, GDP follows

Be careful what you wish for

The Bank of Thailand has more reasons to ease monetary policy to support growth but has no ammunition left. The central bank's best wish has been a weaker Thai baht (THB) as necessary for the potential exports and tourism recovery. This is something they strived hard to achieve through several policy measures since late 2019 to dampen the currency appreciation but failed.

We have also revised our end-2021 USD/THB forecast to 31.30 from 29.80 previously.

Their wish is finally coming true. The THB’s 3.7% depreciation against the USD during the global risk-off in March was the steepest among Asian currencies, taking the USD/THB rate to a five-month high of 31.30. So was the 4.3% year-to-date depreciation sitting at the bottom of the Asian performance table.

We believe the THB depreciation trend has further to run as multiple waves and variants of Covid-19 globally delay the tourism recovery. We now see the USD/THB trading up to 31.90 over 2Q21 in contrast to our previous forecast of 30.00 for the period. We have also revised our end-2021 USD/THB view to 31.30 from 29.80 previously.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 1 April 2021

- This bundle contains 3 Articles