Thailand: Unanimous consensus to keep rates near record-lows

- 27 March 2018

- Thailand

We're struggling to find strong reasons to change our view of no change in the Bank of Thailand policy in 2018

| 1.5% |

Bank of Thailand policy rateUnchanged since April 2015 |

The Bank of Thailand (BoT) Monetary Policy Committee has another policy meeting tomorrow (28 March), but it hasn’t changed rates since the 25bp rate cut to 1.5% in April 2015.

There is unanimous consensus that the central bank will not do anything at this meeting either which is why most analysts are likely to concentrate on the BoT policy statement for future policy move clues. And this is also why we're struggling to find strong reasons to change our view of no change in the BoT policy in 2018.

Weak economic fundamentals persist

Firmer exports and manufacturing growth so far in 2018 may provide a further lift to the central bank’s growth optimism in the policy statement even as underlying fundamentals continue to be dogged by weak domestic demand which is also evident in persistent low inflation.

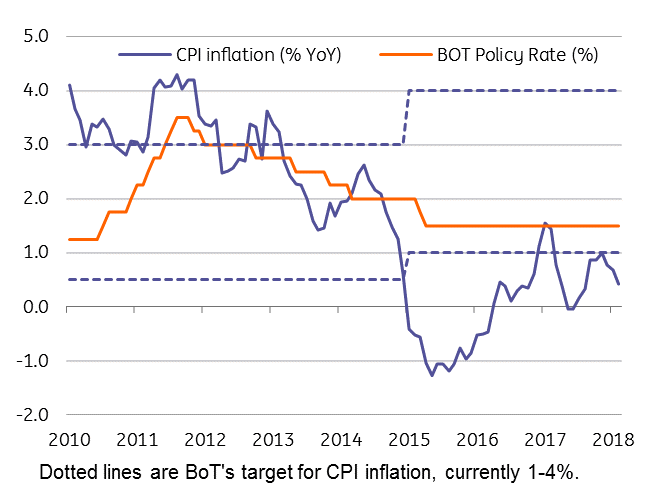

The central bank’s optimism on improving inflation trend this year also seems to be unfounded. The 0.7% year-to-date inflation in February was down from 1.5% a year ago. The BoT’s inflation target of 1- 4% remains at risk of not being achieved again this year (see chart). Therefore, it would hardly come as a surprise if the BoT moves to cut the inflation target itself.

Inflation and the central bank policy rate

Thai baht re-pricing

The currency appreciation slowed in the last two months, but the Thai baht (THB) hasn’t been displaced from its top performing spot among Asian currencies with 4.6% year-to-date appreciation against the USD.

Strong currency will continue to dampen inflationary pressures from rising global commodity prices, especially oil price.

We believe re-pricing for narrower external surplus and lingering political uncertainty surrounding timing of general elections will weigh on the THB performance going forward, which is why we forecast a tight range trading of USD/THB around 31 in the next 12 months.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 28 March 2018

- This bundle contains 1 Articles