Thailand: Manufacturing surprisingly swings back to growth in April

- 28 May 2019

- Thailand

We don’t think the worst is over just yet and maintain our view of a central bank policy rate cut in June

| 2.0% |

April manufacturing growth |

| Better than expected | |

A pleasant manufacturing miss

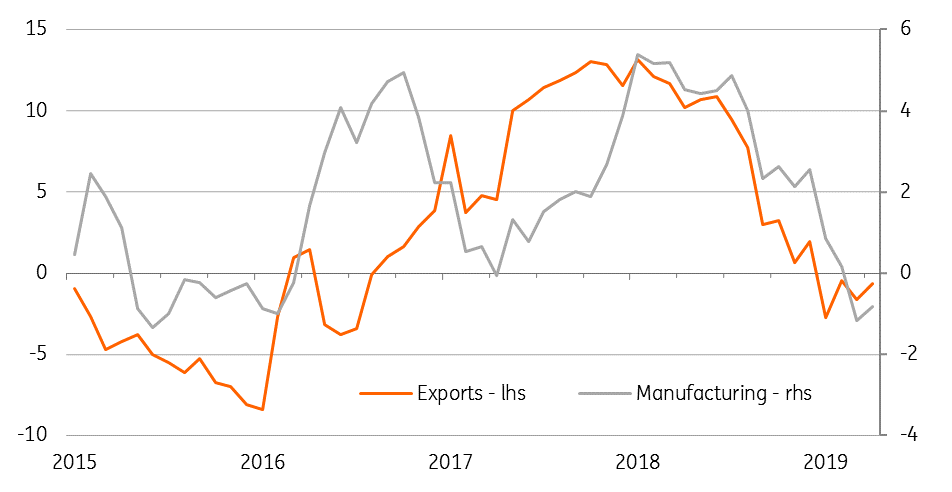

Contrary to the expectation of continued decline, Thailand’s manufacturing output rose by 2.0% year-on-year in April after two consecutive months of contraction. The consensus estimate was -0.9%, and we were more bearish at -1.5%. Meanwhile, March growth was revised lower to -2.7% from the -2.5% initial estimate.

The Songkran (Thai New Year) holiday typically dents economic activity in April. The added whammy this year was weak exports owing to all the trade noise globally, which earlier this month forced a downgrade of the official export growth forecast for this year to 2.2% from 4.1%. Despite this, the 17% month-on-month (unadjusted for seasonality) fall in the manufacturing index was the smallest fall for the month since 2010. Likewise for exports whose 13.5% fall in April was the smallest in the last three years.

Exports drive manufacturing (% YoY, 3-month moving average)

Still, a strong case for central bank easing

However, this doesn’t change the underlying story of weak exports and manufacturing continuing to depress GDP growth over the rest of the year. Moreover, inventory re-stocking had been a key driver of GDP growth in recent quarters and, absent any recovery in demand, it could turn out to be a potential drag on growth. That said our forecast of a slightly better, 3% YoY GDP growth in the current quarter than the 4-year low of 2.8% registered in the first quarter, benefits from the low base year effect rather than demonstrating any underlying improvement in the economy. We see growth remaining stuck below the government’s 4% comfort level for the rest of the year.

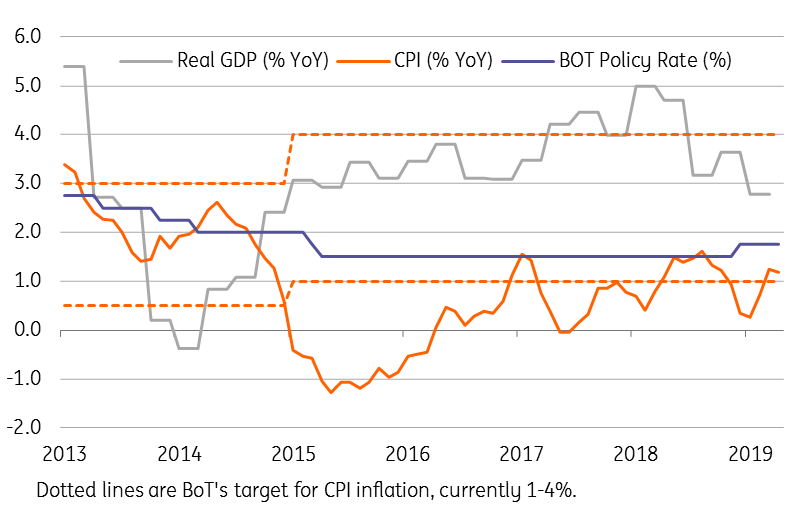

Following the dismal first-quarter GDP report earlier this month we revised our 2019 growth forecast to 3.1% from 3.8%, and also our view on the Bank of Thailand’s policy from stable policy interest rates, currently 1.75%, to a 25 basis point cut at the next meeting in June. While the policy forecast revision has put us outside the consensus, which is solidly behind no policy change this year, we believe the BoT will bite the bullet and at least reverse the December 2018 rate hike that wasn’t required in the first place. And still, with persistently low inflation, it will be left with enough policy space for future easing.

The BoT has enough space for easing

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 29 May 2019

- This bundle contains 4 Articles