Thailand’s economy on a very slow recovery path

- 30 September 2020

- Thailand

Latest activity data suggests the recovery is coming along slowly. However, tourism is still non-existent and until that returns, positive GDP growth will remain nowhere to be seen. That's why we revise our end-2020 USD/THB forecast from 31.50 to 32.00

| -9.3% |

August manufacturing growthYear-on-year |

| Better than expected | |

Firming manufacturing

Thailand’s manufacturing output expanded again in August, though there is still some way to go before output reaches the level seen before the pandemic.

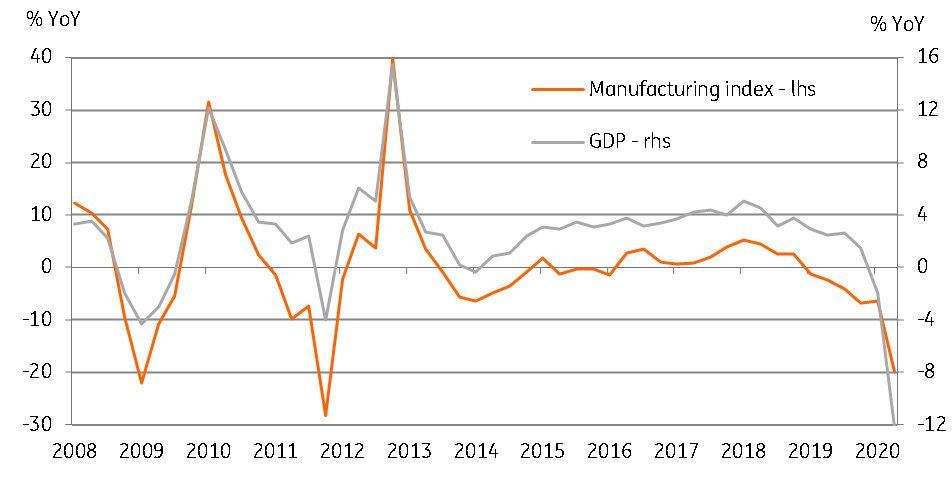

The manufacturing production index rose by 4.8% month-on-month in August - the fourth straight monthly rise following 5.3% in July. This still leaves the index almost 12% below its pre-Covid level in March and 9.3% below a year-ago level. The year-on-year fall is, however, the smallest since March and follows July’s 12.9% fall. The moderate fall here is consistent with what we saw in exports whose 7.9% YoY fall in August was shallower than July’s fall.

Weak domestic demand has been a bigger drag on manufacturing than exports. This with continued large unused manufacturing capacity should ensure no imminent inflation pressure in the near term. The capacity utilisation improved to 60.7% in August from 57.6% in the previous month but was still well below the 67.7% pre-Covid level.

Manufacturing drives GDP growth. Average July-August manufacturing fall of 11% YoY foreshadows continued negative GDP growth in the third quarter. We forecast -8.2% GDP growth in 3Q (-12.2% in 2Q).

Where manufacturing goes, GDP follows

Wide current account surplus

Also released today, the balance of payments data for August reinforced the persistent trend of big trade and current account surpluses.

The $3 billion current account surplus in the last month was bigger than our estimate of $2.4 billion and consensus of $2 billion. It was also wider than the $1.8 billion surplus seen in July.

No prizes for guessing that the large goods trade surplus continued to offset net services outflows in the last month. At about $5.4 billion, the trade surplus in August was the third-highest ever, thanks to persistently weak domestic demand. Even as exports shrank by 8.2% YoY in the last month, imports plunged even more, by 19.1%. The services account posted another $2.4 billion of net outflows in August, owing mainly to the weak tourism sector.

Revising our USD/THB forecast

This brings the cumulative current account surplus in the first eight months of 2020 to $12.9 billion, which is down from $24 billion in the same period last year. A trend of narrowing current surplus has been a source of the THB underperformance relative to its Asian peers so far this year. The THB ended another month today as an Asian underperformer - a status it is likely to hold over the remainder of the year.

On that note, we revise our end-2020 USD/THB forecast from 31.50 to 32.00 (spot 31.66). This risk to this forecast is tilted to the upside amid rising political risk along with anti-government protests.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 1 October 2020

- This bundle contains 3 Articles