Why telecoms operators can largely shoulder higher interest rates

- 7 February 2023

- TMT

While the telecom sector remains sensitive to swings in interest rates, we're expecting to see a relatively limited impact for 2023. Interest costs are a relatively small cost item and it will take time before the legacy debt is repriced at the prevailing market rate

Telecom operators can handle higher interest costs in 2023

As interest rates rose throughout 2022 and beyond, the tailwind from central banks buying corporate credit dissipated while borrowing rates for companies increased. We expect the impact on telecom companies to be limited in 2023. We do expect that an increase in borrowing costs will impact free cash flow over time, but the effect will be gradual and relatively limited for investment-grade companies.

Nevertheless, elevated leverage compared to other sectors justifies taking a closer look at this. At 2x Net debt/EBITDA, leverage in the telecoms sector is about twice as high in our sample as it is for the broader corporate sector. The stability over time in our sample surprises us somewhat, as we have shown previously that credit ratings are also under pressure – and there is some notable dispersion within the data. Some companies have been improving balance sheets over time, while others have been happy to take on a bit more debt.

There are two key reasons that we're not too concerned with higher interest rates for 2023. The first is that borrowing costs are a small part of the total cost base; the second is that there are relatively few debt redemptions in the near term. Based on calculations from four investment-grade companies, we estimate that net financial expenses make up around 3% of total costs (including Depreciation & Amortisation). This percentage is somewhat higher for investment-grade companies with a BBB+ rating, as the sample is a mix of A-rated and BBB-rated companies. The number is even smaller as a percentage of revenues (as opposed to costs). If interest rates increase over time, we will see an impact – although it should be a very gradual one, according to our analysis.

Relatively few near term debt redemptions

Telecom operators manage their debts in such a way that they have limited upcoming debt redemptions every year. While they typically redeem notes with the proceeds from newly issued bonds, they now have to pay a higher coupon. It will therefore take some time before companies have replaced all their debts with newer, more costly debts. Based on our calculations of all telecom bonds that were outstanding at the beginning of 2023, only 7% should be refinanced this year. If funding costs were double the amount that they were in the past, it would take a couple of years for the full effects to be seen.

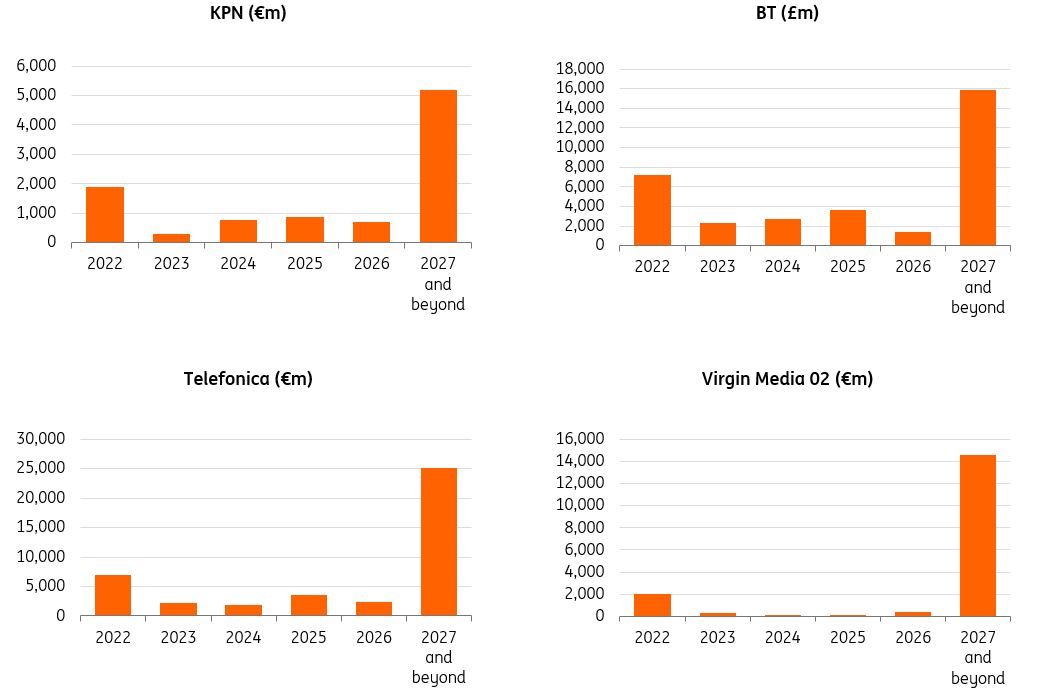

This effect is even more subdued when we look at the redemption profile of individual companies as opposed to the full European telecom bond market. Detailed in the graphs below are the debt amortisation profiles of four telecom companies, with a notable share of debt redemptions scheduled for 2027 and beyond. There is often a substantial amount of current debts, but this usually includes payables as opposed to bank debt or bonds. Telecom operators will therefore have time to adjust to the reality of higher interest rates. As can be seen in the graph below, high-yield companies (such as Virgin Media O2) have also pushed out debt redemptions.

No large debt redemptions in near term for many telecom operators

Nevertheless, interest rates are moving higher

Average corporate borrowing costs were substantially below 1% for most months from April 2019 until the start of 2022, as measured by the investment grade credit index. This provided a nice tailwind to corporates, as they were able to refinance legacy coupons with lower ones. The yield began rising in August 2021, as can be seen in the graph below. Current yields are just below 4% – a level last seen in 2012.

For benchmark telecom operators, these swings have been less turbulent. In October 2012, Deutsche Telecom issued a 12-year note with a coupon of 2.75%, while in July 2016, the coupon on a new 12-year note was 1.5%. Today, the company has a 2034 note outstanding that trades at a yield of 3.4%. The 4-year note has a 2.9% yield. These current yields are higher than the 2% that Deutsche Telecom has to pay on its existing euro notes (the average coupon). This example shows that funding costs will likely be higher.

However, the impact will come about gradually and will fit within a normal investment-grade credit profile. Given that the yield on corporate credit is now similar to the dividend yield of the broader equity universe (and relatively high given recent history), one could also argue that borrowing costs may have peaked. If investors allocate money to credit, funding costs could even decline. In that scenario, the challenge for telecom operators would be reduced even further.

Yield on investment grade bonds approaches the dividend yield in Europe

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Telecoms Outlook 2023: Navigating challenges at the speed of light

- This bundle contains 8 Articles