Taiwan quarterly: Coronavirus and politics take a toll

- 21 February 2020

- Taiwan

The hit to Taiwan's economy from the coronavirus comes not just from consumption and trade but also from chaotic politics, which could be a hurdle to implementing timely and appropriate policies to help corporates survive. This is why our outlook is more dismal than the government's

Taiwan economy amid Covid-19

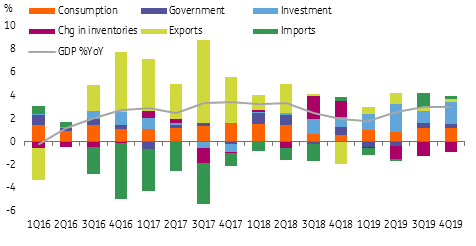

Every economy that's been hit by the impact of Covid-19 has seen its consumption industry suffer. Taiwan is no different.

But the economic relationship between Mainland China and Taiwan is bigger in terms of production than consumption, which means factories that rely on Mainland China’s products and parts for Taiwan’s own production, could be hit harder.

With production expected to fall, exports and imports will decline too, hurting yet more sectors such as trading and logistics.

Taiwan GDP growth composition

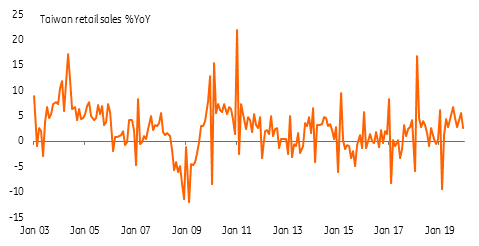

Consumption will be hit by domestic spenders and tourists

Unlike in Hong Kong and Mainland China, where workers have been encouraged to work from home, workers in Taiwan are still largely heading into the office, suggesting less disruption to the service sector. But consumers have avoided going to public places wherever possible, so consumption has still been affected.

Tourism has taken a hit, too. Chinese tourists make up just under a quarter (24.4%) of all tourists in Taiwan, and tourism activities account for 2.3% of the country's GDP. This is a relatively small contribution to GDP and could lead the government to underestimate the economic damage from the Covid-19 epidemic. But we project that the coronavirus could lead to a fall in retail sales from 2.75% year-on-year in December to -2% YoY in January and even slower, to -4%YoY in February.

Taiwan retail sales growth %YoY

Production will be hurt by supply chain disruption

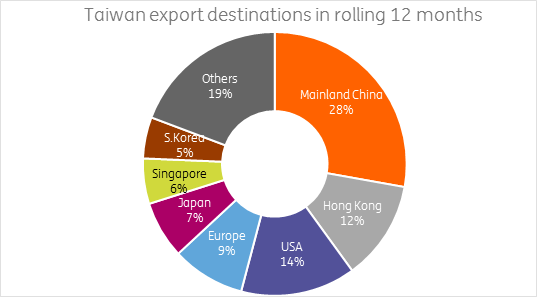

Mainland China and Taiwan have a close relationship in terms of manufacturing. Taiwan's exports to Mainland China accounted for 23% of Taiwan’s nominal GDP in the fourth quarter. This demonstrates the strong ties between the economies on trade and manufacturing, as most of the trade between the two is electronics-related parts and products.

The delay in the resumption of factory work in Mainland China will affect Taiwan’s manufacturers, which rely on those parts and products for their own production. The supply chain could create a negative feedback loop as global manufacturers rely on Taiwan-made products and parts, and therefore Taiwan’s exports to non-Mainland China economies.

It's not just parts and products that will be disrupted, revenue of Taiwan's affected manufacturers will also feel the effects.

This will, in turn, affect wages and employment, and therefore domestic consumption, though this will partly be offset by the Government's stimulus programme.

We don't know when Mainland China’s factories will resume work at normal capacity, but it is unlikely to be in the first quarter.

Taiwan export partners

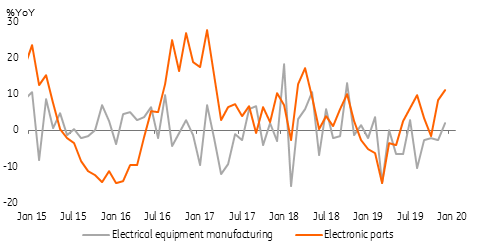

Electronic production will be affected by the broken supply chain

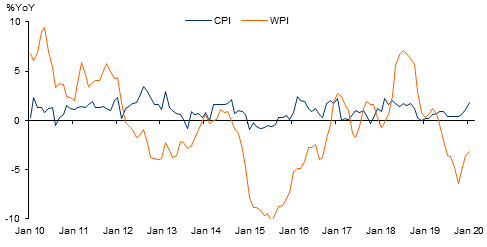

Risk of deflation

With consumers increasingly staying at home, prices of consumer goods and services are likely to drop in the first and second quarters.

CPI inflation was 1.85% in January 2020, of which services CPI inflation was 1.97%. The good news is that CPI inflation was very low at around 0.4% in the first half of last year, so there is a low base effect which should prevent CPI inflation turning negative, even though prices are, in fact, falling on a monthly basis.

The worrying point here is that the technical base effect could mask the risk of deflation, which could lead to an underestimation of the economic situation by the government.

Chaotic political environment doesn’t help

Even after Tsai Ing-wen was re-elected as President of Taiwan, the chaotic politics in Taiwan have not stopped.

Before the start of the Hong Kong protests, Tsai suffered low approval ratings due to inadequate and inefficient economic policies. GDP growth slowed at one point (1Q19) below 2% YoY. However, cooling sentiment towards Mainland China, which resulted in the Hong Kong protests, saw her popularity increase, allowing her to win the presidency.

Tsai is now fighting against Covid-19, possibly by handing out a stimulus package. But when it comes to economic policy, her track record is viewed by some as unimpressive. And she is, in fact, still leveraging on anti-Mainland China emotions from Covid-19 to lift her approval ratings. This may not last long, as we doubt the effectiveness of any forthcoming stimulus package.

Fiscal stimulus planned to offset Covid-19

On 27 February 2020, the executive branch of Taiwan's government, the Executive Yuan, will propose a special budget of TWD60 billion (equivalent to 0.3% of nominal GDP in 2020 at TWD19,576.7 billion forecast by the government) for consideration by the Legislative Yuan. This includes TWD2 billion of consumption coupons for designated spending after the epidemic ends, together with loan repayment extensions for one and a half years for some corporates. There are already debates between the parties of DPP and KMT on stimulus details, e.g. the effectiveness of consumption coupons to boost retail sales.

Even if the package can pass the Legislative Yuan, it is difficult to see it offsetting much of the damage caused by Covid-19 because:

- part of the damage from Covid-19 comes from linkages of the supply chains between Taiwan and Mainland China factories. If Mainland China factories continue to delay the resumption of work, that will continue to hit Taiwan's economy via production and exports. And the timing of such is uncertain.

- the peak tourism period in spring will be missed, and consumption coupons will not be able to make up the loss of revenue in the tourism and airline industries.

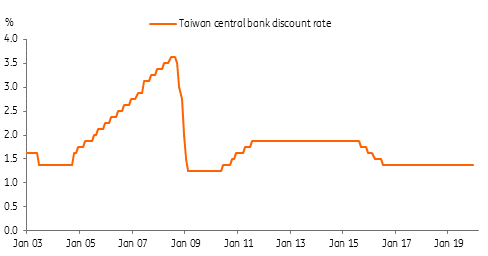

Monetary policy is not going to help a lot

There is very little room for monetary policy to support the economy materially. The policy rate has stood at 1.375% for a long time because it is already at a low level, and the central bank would like to leave room for an event that really warrants an interest rate cut.

Is this the moment for a rate cut? We don’t think so. A lower interest rate can't do very much for corporates which have outstanding loans, or would like to draw a loan for an emergency. We believe fiscal stimulus would benefit corporates more if the stimulus was bigger and targeted emerging liquidity needs.

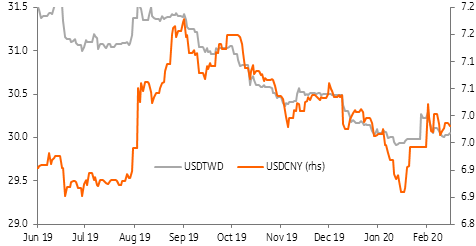

USD/TWD shares the same trend of USD/CNY

Since the outbreak of Covid-19, the Taiwan dollar and Chinese yuan have almost moved in tandem.

The co-movements of the two currencies were not obvious previously but increased after news of a possible trade agreement between the US and Mainland China, with capital inflows into Taiwanese asset markets supporting the TWD.

Following news of delayed factory production in Mainland China, with no immediate solution for Taiwan's manufacturers, the Taiwan stock market began to lose momentum and so did the currency.

We expect that the Taiwan dollar will continue to weaken if Mainland China's factories are slow to resume work. Our forecast for USD/TWD is 31.00 by the end of the first quarter and 30.00 by the end of 2020.

TWD and CNY trends

GDP forecast

The government has downgraded Taiwan’s GDP forecast for 2020 to reflect the impact of Covid-19, but only slightly. It calls for growth of 2.37% from November’s projection of 2.72%, mainly because of slower export growth at 2.85%, from November's 3.12%.

But we are less optimistic. Our forecast on Taiwan GDP growth is 0.8% for 2020, mainly because:

- the Taiwan government largely expects damage from Covid-19 only in the first quarter, and expects a recovery starting from the second quarter, but we expect a meaningful recovery to start nearer to the end of the second quarter;

- uncertainty about the timing of the resumption of work at Mainland China's factories will affect Taiwan's production and exports. A weaker currency can't compensate for the contraction in exports;

- consumption coupons post-epidemic are unlikely to compensate for the loss in retail sales.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 24 February 2020

- This bundle contains 3 Articles