Taiwan inflation cools while exports continue to beat forecasts

- 8 July 2025

- Taiwan Trade

CPI inflation fell to a 51-month low of 1.4% year-on-year amid a broad-based cooling of price pressures, while trade data continues to surprise to the upside as tech trade remains resilient

Falling inflation and stronger TWD remove impediments to CBC easing

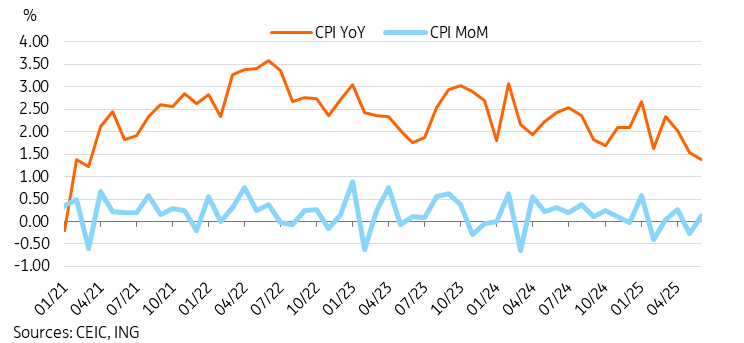

June CPI inflation bucked expectations for a slight uptick, instead dropping to 1.37% YoY from 1.55% YoY, marking the lowest level since March 2021.

The decline of inflation was broad-based, with most key inflation categories declining on the month, most notably in food prices, which fell to 2.8% YoY from 4.9% YoY the previous month. Housing price inflation also moderated for the third consecutive month, down to 1.8% YoY. The clothing and transportation categories continued the trend from recent months, remaining in deflation.

While inflation has not necessarily been the most significant consideration in recent monetary policy decision-making, inflation has been more or less near the target range for much of the past year, while only recently dropping noticeably under target. A further drop in June inflation probably won't raise the urgency to cut rates, but combined with the recent strengthening of the Taiwan dollar, these conditions create a suitable environment for the CBC to ease if it deems it necessary.

CPI inflation has been on a cooling trajectory in the past few months

Trade data continues to surprise to the upside again

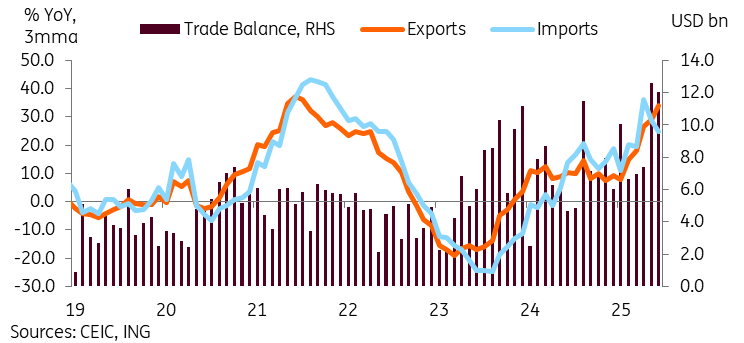

At the risk of beginning to sound like a broken record, Taiwan's trade growth continued to surprise on the upside again.

Exports grew by 33.7% YoY, which was a slight slowdown from May's 38.6% YoY growth but nonetheless clearly still a very impressive rate.

By export destination, far and away the US (90.9%) continues to represent the fastest growth market for Taiwan's exports. Exports to Japan (25.3%) and Korea (32.7%) also accelerated on the month. In contrast, we saw export growth slow to China (13.1%), ASEAN (28.2%), and the EU (-5.4%).

The breakdown of exports by product continues to show a high degree of concentration. Semiconductor exports rose 32.9% YoY, computer exports continued to see triple-digit growth at 116.2% YoY, while the broader electronics and ICT products category grew 53.0% YoY. As we've seen in the past few months, tech exports aside, many categories were quite weak, with numerous categories seeing YoY contraction.

Imports also beat forecasts with a respectable 17.3% YoY growth. While imports were also concentrated in machinery and tech-related categories, unlike the export situation, the fastest import growth for Taiwan was from Europe (35.7%) and Korea (36.1%), while imports from the US were down -5.2% YoY.

On net, Taiwan's trade surplus remained high at USD 12.1bn. Over the first half of the year, Taiwan's trade surplus surged to USD 55.7bn, which is 54.3% YoY higher compared to 1H24, and will likely contribute to Taiwan's GDP growth eclipsing forecasts in 1H25.

Moving forward, what happens in terms of tariffs could play a significant role in Taiwan's trade and growth trajectories in the second half of the year. Given the heavy concentration of exports, sector-specific tariffs could have just as much of an impact as the broad-based tariffs.

Taiwan's trade growth continues to beat forecasts for another month

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more