Taiwan: Central bank to stay put

- 12 September 2018

- China Taiwan

We expect Taiwan's central bank to leave rates unchanged 21 June for an eighth straight quarter amid concern the economy could be affected by trade wars between China and the US (through the supply chain of China's export goods.) The already low policy rate provides little room for a cut

Taiwan electronics industry at risk

Taiwan is caught in the middle of the US-China trade war and is deemed to face increasing risks of an economic slowdown via its electronics industry. This sector has served as part of the supply chain for Mainland China's smart-device manufacturing. If the US imposes tariffs or another sanction on Chinese smart-devices, Taiwan's electronics industry will suffer.

The most likely scenario is that Mainland China buyers will ask for lower prices for parts. And buyers will possibly buy fewer parts if they expect lower export volume due to the tariffs. Put simply, Taiwan's electronic producers could face lower selling prices and sales volume if the US imposes 25% tariffs on Mainland China's high-tech goods.

GDP growth to edge lower

Even though the government has put together some policies to restructure the economy, we cannot see a new growth engine arising. The economy is still very dependent on electronics. As a result, GDP growth will likely peak in 2Q18 at 3.1% year on year from 3.0% in 1Q, followed by growth of 2.4% and 2.0% for 3Q and 4Q18, respectively.

The central bank will stay put

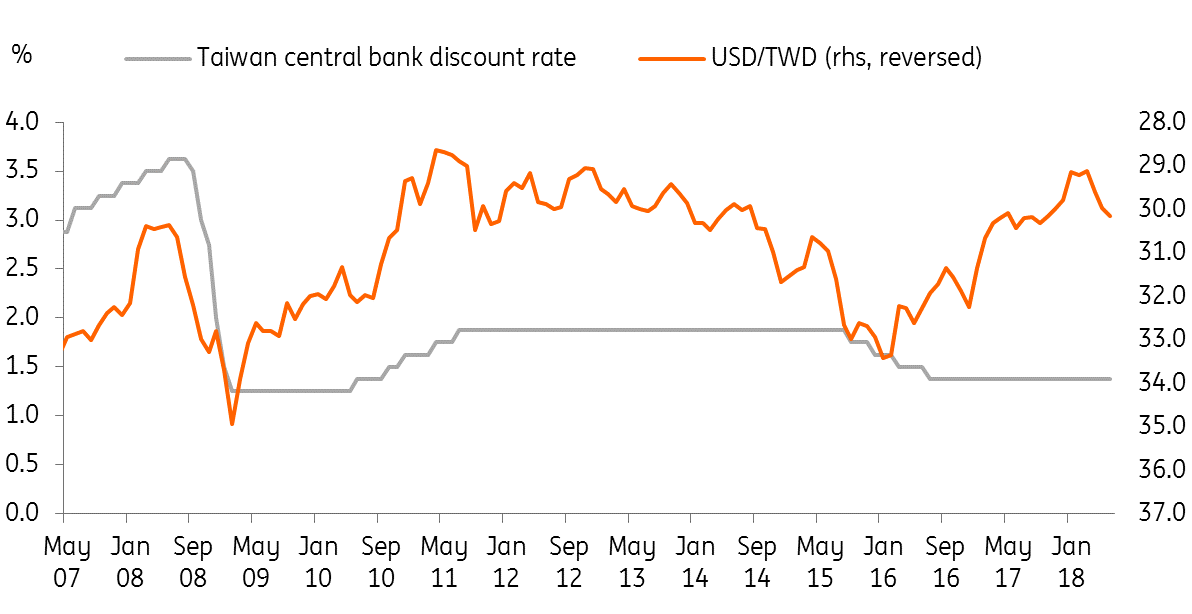

As the economy faces higher risks from global trade wars, the central bank won't be raising interest rates. But it's not good timing to lower rates either. The policy rate is already at a low level of 1.375% and cutting it would do nothing to reduce the risk of a trade war. The Taiwan central bank, just like the economy, is now trapped by escalating tensions between Mainland China and the US, and as such, we don't expect any policy rate change in 2018.

Even with a pause, TWD would weaken

With a possible negative effect on the electronics industry, previous capital inflows into Taiwan's stock market could turn to outflows in the second half of the year. Together with a strong dollar from escalating trade tensions and European political uncertainties, we expect the Taiwan dollar (TWD) to weaken against the US dollar through the rest of the year to 30.60 at the end of 2018, that is equivalent to a 2.5% depreciation of TWD against the USD.

The Taiwan central bank, just like the economy, is now trapped by escalating tensions between Mainland China and the US

This would support exports, but only slightly. If the US were to impose a 25% tariff on Chinese high-tech goods which affected parts produced in Taiwan (thus lowering prices and sales volumes), a marginally weaker currency wouldn't change Taiwan's weaker growth trend.

We expect TWD to weaken even as central bank stays put

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 21 June 2018

- This bundle contains 3 Articles