Sweden: What next for the Riksbank?

- 10 November 2017

- Sweden

Now that the ECB has made its move, the Riksbank will have to make up its mind in December. In the end, we think it'll not add to asset purchases but will retain a dovish bias

At its last meeting two weeks ago, the Riksbank avoided taking any major decisions before the ECB announced its tapering decision. Now that the ECB has made its move, the Riksbank will have to decide in December. The minutes suggest the committee is finely balanced.

The key concern remains the currency, with the Riksbank worried about tightening policy while other central banks, especially the ECB, are in loosening mode would lead to a rapid appreciation of the SEK, which would push down inflation in Sweden. This is why the Riksbank has kept policy so loose despite the Swedish economy outperforming the euro area over the past few years.

Divisions on the policy-setting committee

In the past, the committee has been divided on the optimal policy path. Three members voted against the last two extensions of QE (December 2016 and April this year). Their argument has been the Swedish economy is performing strongly, and policy is already sufficiently loose to bring inflation back to target. Given domestic data has continued to be strong in 2017 and inflation has now returned to the 2% target. It is hard to see these members voting for more QE in December unless there is a significant negative surprise in the data before then.

The other three members, including Governor Ingves with the tie-breaking vote, have favoured a looser stance, citing subdued inflation, currency concerns, and downside risks to the global economy to justify a looser policy stance. So the question in December largely comes down to how these three members see developments.

Key factors argue against an extension

None of the three doves are scheduled to speak before the December meeting. But ultra-dovish Deputy Governor Jansson has set out three conditions that need to be met before starting to phase out the current policy measure, which we think are a useful guide to the members’ thinking:

Inflation steady around the target: both the headline and underlying consumer price inflation with fixed interest rates (CPIF) measures have risen in recent months and are expected to remain around the 2% target. The picture has been somewhat muddled by erratic factors though, so the October and November figures will be particularly important.

No rapid currency appreciation: the trade-weighted KIX index has fallen by around 3% since August, which should provide some comfort to policy-makers. The latest Riskbank forecasts see the KIX appreciating by 3-4% from current levels by end-2018, and a further 2% in 2019. So the currency could come up a bit from current levels without triggering too much concern.

Cumulative change in KIX trade-weighted index since 2016

Clarity on ECB and Fed intentions: The Fed has delivered balance sheet reduction and is on track for another rate hike in December. The ECB’s announcement was broadly in line with market expectations in terms of further QE purchases, but the decision to keep the programme open-ended and the tone of President Draghi’s press conference remarks were relatively dovish. This makes the Riksbank’s position a bit tricky because it leaves some uncertainty around when ECB will end QE and start to raise rates.

The housing market is a downside risk

Another important factor mentioned by several committee members in the October minutes is the housing market. House prices in Sweden have grown strongly for several years, leading to a rapid build-up of household debt. The Riksbank has repeatedly warned that these trends are a risk to financial stability.

The market now looks a bit wobbly as significant increases in supply and macroprudential measures to tighten lending standards weighing on prices have fallen in the past two months. There is clear concern on the committee that these developments could affect growth and inflation next year. If there are further negative developments, this could prompt the committee to delay tightening.

We think Riksbank will remain dovish

Overall, we don’t think the Riksbank can justify extending QE in December, and is likely to leave the interest rate forecast unchanged. Only ultra-dove Jansson continues to advocate more QE and delayed interest rate hikes, despite the improvement in his three criteria. Ingves and Af Jochnick, the other two doves, appear comfortable with the current stance, while on the hawkish side Skingsley and Floden seem sufficiently worried about the housing market that they are unlikely to advocate faster interest rate hikes.

Instead, we think the committee will seek to minimise the risk of rapid currency appreciation by keeping communication dovish and emphasising its willingness to change course and loosen again if the situation warrants. It may also give concrete signals of a continued dovish bias. One possibility is that the first rate hike could be 10bp rather than the standard 25bps, which would keep the policy rate in line with the ECB’s deposit rate for longer.

Another option could be to pre-commit to reinvesting coupons and maturing bonds for a long period, perhaps the end of 2019 or until interest rates reach a certain threshold, and to establish a smooth path for reinvestments that keeps the Riksbank buying bonds in 2018 at a reduced rate.

How the Riksbank might approach reinvestments of QE bonds

So far, the Riksbank has simply stated at each meeting that it will continue to reinvest coupon and redemption payments of the Swedish government bonds it holds. Given the ECB has provided more detail on its holdings and reinvestment schedule as the Fed and Bank of England did previously, it would make sense for the Riksbank to do the same.

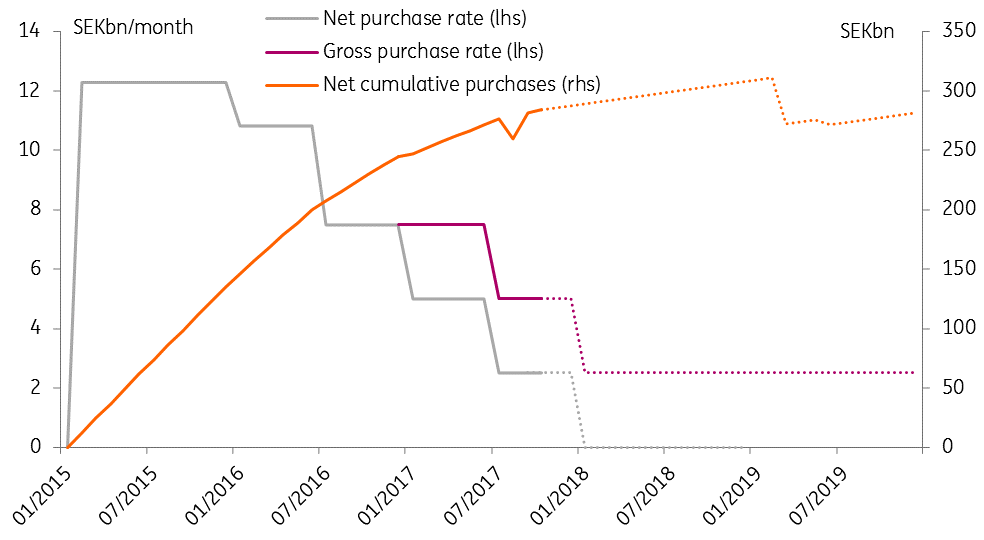

An interesting wrinkle here is that the Riksbank’s government bond holdings are very ‘lumpy’. Few Swedish bonds are outstanding, and none are maturing in 2018. So reinvestments in 2018 would be only the coupon payments and therefore relatively small (on the order of ~SEK10bn).

But there are two significant redemptions in 2019, of which the Riksbank probably holds SEK40-50bn worth (and another two redemptions for a similar amount at the end of 2020). In 2017 the Riksbank faced a similar situation with a single large redemption in August. At that time it chose to spread out reinvestments totalling about SEK30bn over the whole year, smoothing the reinvestment profile.

If it were to apply the same approach to reinvestments in 2018 and 2019, that would mean purchasing perhaps SEK25-35bn of bonds in 2018 (compared to SEK75bn gross, SEK45bn net, in 2017) and a similar amount in 2019. So the amount of bonds on the Riksbank’s balance sheet would temporarily expand beyond the SEK290bn of announced asset purchases but return to this size by end-2019.

Whether such an approach amounts to an extension of QE or not is something of a sematic question. The economic effect should be limited, given the size purchases involved are in any case small. But we think it would be a practical approach to managing the balance sheet and would help the Riksbank to start scaling back stimulus in a dovish way.

Stylised chart of the Riksbank's QE programme

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more