November rate hike possible for Swedish Riksbank despite negative growth

- 30 October 2023

- Sweden

Sweden's economy performed worse than expected over the summer. Despite this and signs of weakening in the labour market, the Riksbank remains focused on the currency. Further SEK weakness could unlock a rate hike at the end of November

Sweden’s Riksbank is beginning to stand out as a hawkish outlier in an environment where the Federal Reserve and the European Central Bank (ECB) appear to be at the top of their tightening cycle. In minutes from the recent monetary policy meeting, Governor Erik Thedéen suggests further tightening may be necessary to ensure inflation comes down – and went out of his way to say that the Riksbank is in a different category to other central banks when it comes to further rate hikes. Another hike in November is looking increasingly plausible against a backdrop where the trade-weighted value of the krona remains close to multi-year lows.

Where that trades between now and the 23 November meeting will overwhelmingly determine whether the central bank follows through with another rate hike. Remember that – unlike the Fed and the ECB – Sweden’s central bank stages fewer meetings per year, and doesn’t have one scheduled for December. The scheduled opportunities to change policy are more finite.

Away from the currency, recent data casts more doubt over the need for further tightening. The economy continues to prove vulnerable, with third-quarter GDP coming in flat. We think it’s likely that we’ll see negative growth in the fourth quarter, following a particularly weak September GDP figure.

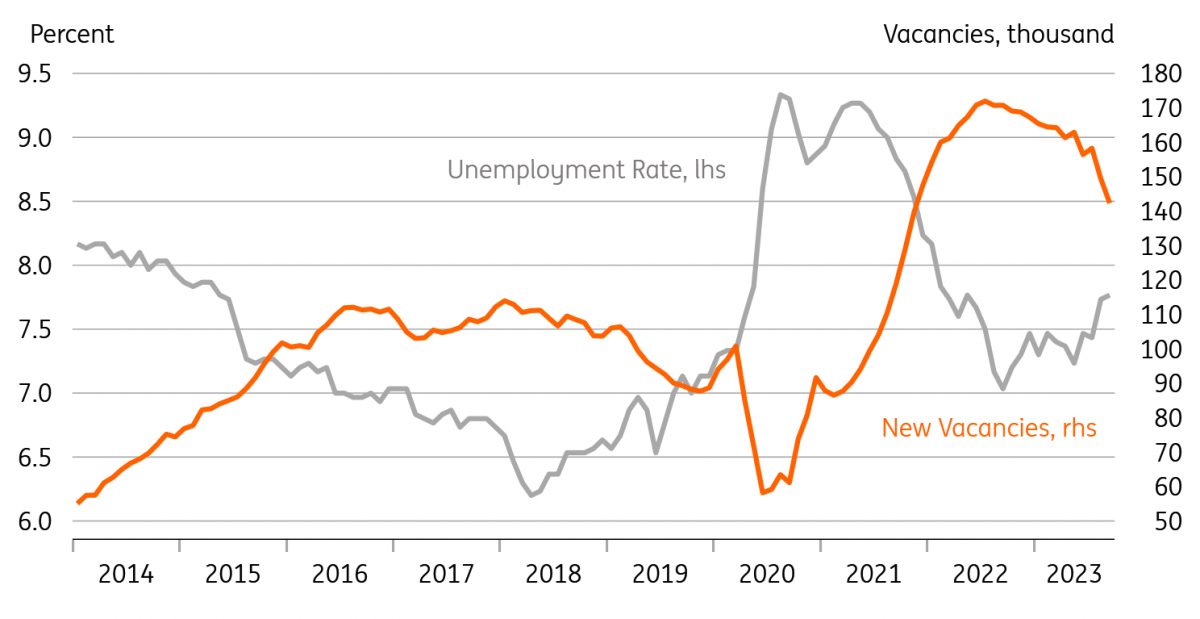

The number of vacancies per unemployed worker

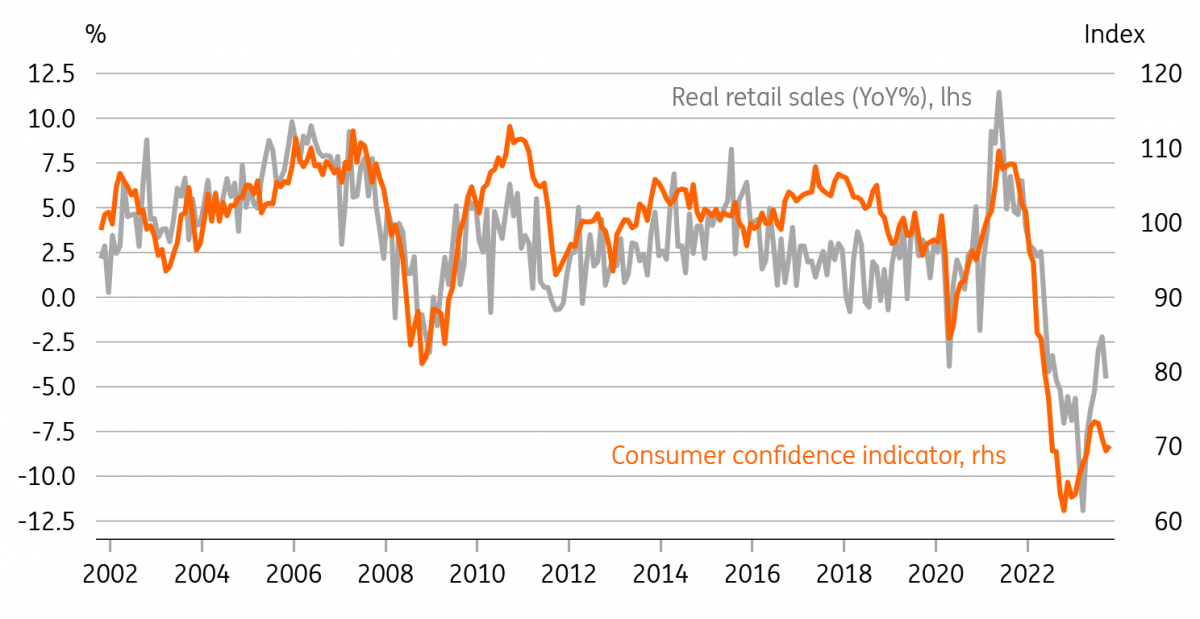

Admittedly, away from the growth figures the story doesn’t look quite as bad. Consumption of services has held up well over the summer and consumer confidence has stabilised, albeit at low levels. The labour market has also remained surprisingly tight, though is starting to show signs of weakness with the number of layoffs spiking up in September. Swedish households also remain very sensitive to short-term interest rates, with large chunks of mortgage lending done at floating rates. That will start to take up bigger portions of their disposable income, and further house price weakness seems likely. We therefore still expect household consumption to fall further as unemployment rises.

In short, the Riksbank has a difficult balancing act of bringing inflation under control and bolstering the krona without putting the economy into a deeper economic downturn. The committee is also acutely aware that services inflation is still at its highs, despite surveys pointing to less aggressive price rises. For now, we’d expect the Riksbank to prioritise the currency over a weakening labour market and economic backdrop.

A 25bp hike in November is possible. But by next summer, like many of the other central banks, we think the Riksbank will be in a position to begin gradually cutting rates back towards a more neutral footing.

Retail sales vs consumer confidence indicator

FX: Riksbank hike may turn out to be more important than FX sales

The deteriorating economic outlook in Sweden has been a long-term depreciating force for the krona. However, the recent interference in the FX market by the Riksbank in the form of FX reserve hedging operations has influenced SEK’s performance more than data and the monetary policy outlook. As discussed here, before FX hedging data began being reported, we didn’t think that the impact of the FX hedging operations would be very long-lasting, and it would have ultimately been down to external factors and the Riksbank’s tightening via rates to drive SEK sustainably higher.

Recent SEK moves have confirmed our suspicions, and an acceleration in FX sales in the second week of hedging has fuelled speculation the Riksbank may be running out of firepower to support SEK via FX sales (in our view). We still see another hike by the Riksbank as a necessary step to take the krona back on a re-appreciating path, that we expect to materialise in full in the second half of 2024 once risk sentiment improves on the back of Fed cuts.

In the shorter run, with strong US data delaying a decline in US rates and new sources of geopolitical uncertainty rising, we think SEK remains vulnerable along with other procyclical currencies – even if the Riksbank FX hedging places it in a slightly more shielded spot than others.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more