Sweden: Krona increasingly pricing in domestic woes

- 31 January 2023

- FX Sweden

We recently published a scenario analysis for EUR/SEK. In the past few days, a worsening domestic picture in Sweden has weighed on SEK, as markets increasingly price in housing and economic pain. Our view is that the Riksbank will manage to avert an uncontrolled property market slump, and SEK will be able to recover, also thanks to upbeat eurozone sentiment

EUR/SEK is enjoying a rather large rally at the time of writing, trading close to the 11.40 level. There is now a chance that the 2009 historical 11.68 high will be tested in the near term. Unstable risk sentiment ahead of the Federal Open Market Committee and weak domestic data in Sweden have likely been the two key drivers of SEK weakness.

After CPI figures surprised on the upside (CPIF rose to 8.4% in the December read), the Economic Tendency survey, unemployment data, retail sales and, finally, growth data all came in on the soft side, especially when compared to rather encouraging data out of the eurozone. All this has increased the perceived risk of a sticky stagflationary environment in Sweden.

Swedish growth slumped in the fourth quarter

Swedish GDP fell by half a percent in the fourth quarter, with high-frequency data pointing to ongoing weakness in consumer spending. Sweden isn’t immune from Europe’s energy crisis, despite using relatively little gas domestically, and the housing market is particularly vulnerable, given almost half of mortgages are on variable rate products, and household indebtedness is comparatively high.

Prices are already down 15% on last February’s peak, and this points to weaker construction activity this year. Add in Sweden’s exposure to the slowdown in manufacturing and fall in new orders being experienced across the developed world, and it looks like the country will be among the weakest performers in Europe through this year.

But 50bp hike by Riksbank still looking likely

For now though, the Riksbank is more worried about core inflation which has continued to climb. All-important pay negotiations are due to conclude in a matter of weeks, and all signs point to an uplift in wage growth across wide areas of the economy.

With new Governor Thedeen warning against recent SEK weakness, and the Riksbank saying in the past that it wants to stay ahead of the ECB in its tightening cycle, we expect a 50bp rate hike in February. Nevertheless, with the housing market under pressure we think we’re nearing the top for Swedish rates. We expect one further 25bp hike in April, marking the top of the cycle.

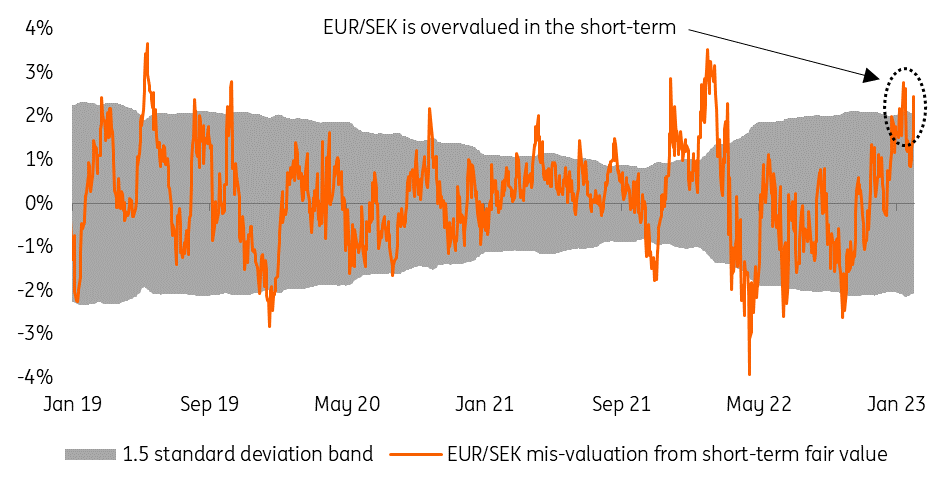

EUR/SEK is overvalued

Our short-term fair value model, which includes rates and equity-related market factors, shows that EUR/SEK is currently around 2.5% overvalued, beyond the 1.5 standard deviation upper-bound.

This suggests that a good deal of negative factors related to the domestic growth picture in Sweden have already been priced into SEK. It’s also important to note that expectations around Riksbank tightening have not fallen after the weak data releases, which means that markets are increasingly pricing in a scenario where the Riksbank is forced to hike and ultimately harms the economy.

A moderately bearish EUR/SEK scenario still likely

A particularly strong economic outlook for Sweden was never been our baseline scenario. In our recent scenario analysis for EUR/SEK, our moderately bearish base case already embeds a relatively subdued growth outlook compared to other EU countries given the vulnerability of the Swedish housing market.

It does seem, however, that markets may have started to price in a very pessimistic scenario for house prices and the Swedish economy. Our view is that the risk of a black-swan fully-fledged property and economic crash in Sweden has not dramatically increased, and SEK can have some room to recover in the coming months as markets gradually price out such risks and SEK can benefit from the improved growth sentiment in the eurozone, to which it normally has a higher beta than the euro itself.

We still expect a return to the 10.60-70 levels by the second half of this year, even though upside risks for EUR/SEK have modestly risen.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more