Strong headwinds ahead for South Korea’s housing market

- 24 May 2023

- Real estate South Korea

The Korean property market plunged sharply last year, and mortgage rates had not even reached their peak. The market seems to have stabilised recently, but we expect the downturn to continue throughout the year, especially in the non-Seoul area

Korea’s housing market has experienced a significant slump since July last year. A number of factors, including high borrowing costs, tight credit conditions, and previously stringent tax and regulatory measures on property, have created an unprecedently sharp decline in the real estate market. We believe that the pace of decline will be relatively moderate this year compared to the second half of 2022, but the slump itself will likely continue throughout 2023. The sluggish growth and financial market stresses caused by the poor housing market are expected to serve as a major reason for the Bank of Korea's rate cut at the end of the year.

Housing and construction are at the centre of Korea’s domestic economy

Since exports are the main growth engine in the Korean economy, the role domestic demand plays on growth is relatively limited due to the high dependence on external demand. However, in terms of domestic growth components, housing and construction play a major role in the economy.

In GDP terms, construction spending accounted for about 15% of total nominal GDP in 2022, including building construction and civil engineering. In industrial production, construction accounts for about 6% of all Korean industry. In the labour market, construction created more than 2.1 million jobs in 2022, equivalent to 7.6% of total employment.

In the case of the financial industry, real estate-related credit is a major part of the financial system. Household mortgage loans account for 54.2% of total household debt (as of 2022) while the real estate project financing balance stood at 112 trillion won (5.7% of GDP) as of June 2022.

The real estate market is on a rollercoaster ride

The domestic housing market has been on a rollercoaster ride for the past few years. Property prices skyrocketed between 2020-21 before plummeting rapidly in late 2022 with prices staying low ever since. There are so many variables that affect the housing market, but in our view, the major reasons for the dramatic swing are the imbalance of property supply and demand and credit conditions.

Supply and demand mismatch is a key reason for recent price swings

Housing supply moves with a long-term cycle of two to three years regardless of the short-term business cycle or external shocks, while housing demand tends to fluctuate more because it can reflect market sentiment in real time. The mismatch between demand and supply has a great impact on the housing market and prices.

New housing supply was expected to shrink during the Covid-19 pandemic, with forward-looking indicators such as construction permits and starts falling over the two to three years prior to the pandemic. Thus, the number of completed units shrank during the pandemic. Although the number of permits and starts began to pick up in 2019, those units only became available in late 2021. On the other hand, housing demand peaked in 2020 and 2021, then declined sharply from 2022.

So why did demand rocket during the pandemic? One of the main reasons was favourable financial conditions for home buyers. Due to aggressive financial and fiscal policy easing, low mortgage rates and ample market liquidity supported home buyers. Mortgage rates had remained at a historically low level for about a year and a half from early 2020. And commercial banks had eased personal loan conditions to aid the negative shocks of the Covid lockdown.

In addition, another factor to stimulate housing demand is the so-called counter-cyclical property policy. The previous government from the progressive party consistently pushed policies to curb the real estate market since the beginning of its administration, including restricting real estate investment (which means purchasing investment properties for rental purposes) and imposing heavy taxes on multiple property owners with the aim of stabilising housing prices. However, contrary to the government’s intention of stabilising house prices, the real estate restraint policy sparked demand sentiment. Fence-sitters jumped into the market all at once, judging that it would be better to buy homes quickly before the government took stricter measures on the property market and prices rose more. So, it ended up creating the herd behaviour of chasing the market and panic buying.

Market liquidity is a key driver for housing demand

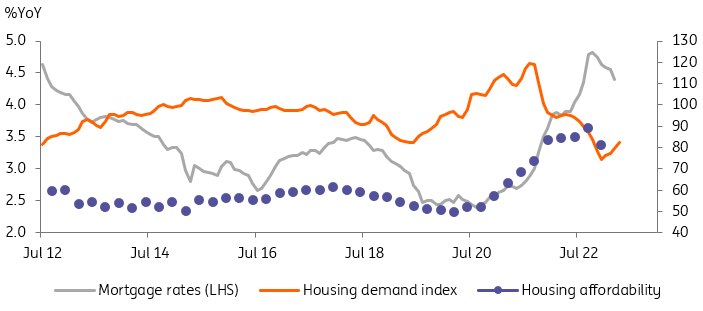

When did this panic buying end?

Based on the data, once the affordable housing index reached over 80 – meaning 80% of the appropriated household burden (about 25% of household income) is paid for by repayment of the principal and interest of mortgage loans – then demand began to be suppressed. This also coincides with the time when the government tightened mortgage conditions the most; most home buyers couldn’t leverage the banks to purchase real estate.

Demand began to decline when the housing affordability index reached 80

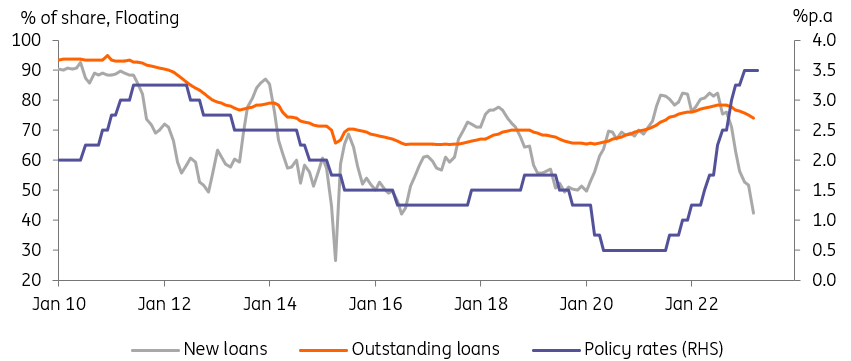

Since more than 70% of the outstanding loan balance is based on floating interest rates, a rise in market rates adds to the debt service burden, not only for new home buyers but also for existing mortgage borrowers. However, the share of floating loans for new loans has come down to 40% with government support of facility loan programmes to refinance floating rates into fixed rates.

Floating based mortgages added to the debt service burden

The housing market will likely remain weak, and regional polarisation is expected

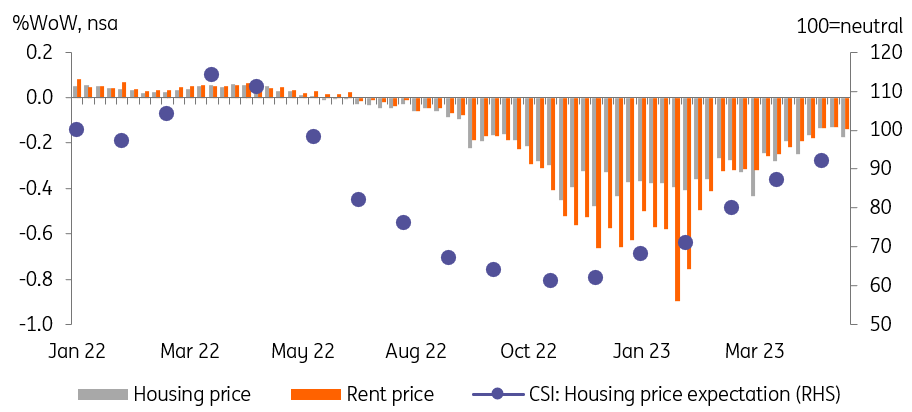

There were signs that the bottom seemed to have passed. For example, consumer sentiment on the housing market has improved since last October, when the government lifted most of its major mortgage conditions and home sales regulations, and the pick-up in sales transactions also followed in the first quarter of this year. However, we think it is a sign of bottom fishing rather than the beginning of a trend upward. Mortgage deregulation was a key milestone for stabilising the real estate market, but it was not strong enough to put the housing market back on track.

Bottom fishing as mortgage rules and other transaction rules eased

Housing transaction picked up in 1Q23 as mortgage conditions eased further

Several signs of a weak housing market in the near term

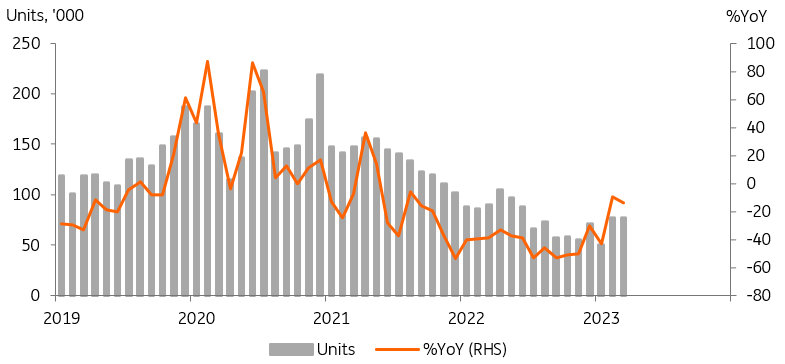

We think other market indicators still point to a weak housing market in the near term. Among several factors, we think that a short-term oversupply of housing will be the main cause of the continued housing market downturn. The number of unsold units has increased significantly over the past year, and it will likely go up further. We have seen a small decline over the past few months but that is because developers have converted some of the unsold units to rental units.

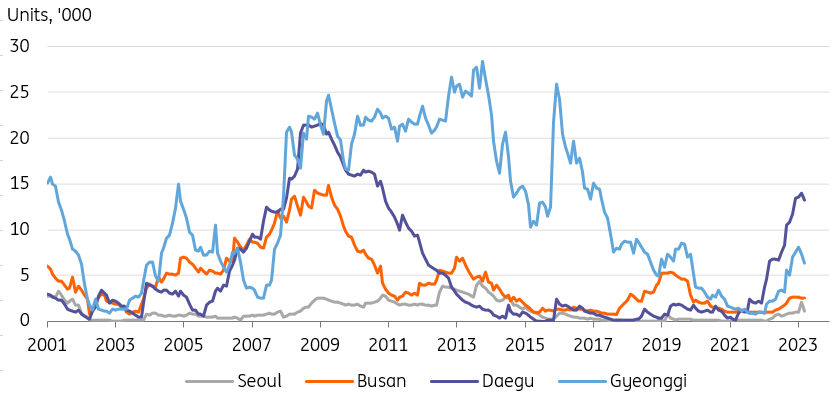

Unsold units will continue to rise in non Seoul areas

Secondly, the number of construction starts has dropped more rapidly than that of permits, which suggests that developers are holding back new development projects as market conditions deteriorate. We believe that the housing inventory should be digested first then the rebound in construction will follow. Thus, this data suggest the weak housing market trend will continue.

Leading indicators for the housing market are falling

Thirdly, the rental market is a good leading indicator to gauge the housing market outlook and it is still declining. Given the recent “Jeonse scam” issue (more on this below), rental prices are expected to stay weak for a while.

What is Jeonse and the Jeonse scam (rental fraud)? And why does it matter?

Jeonse is a unique rental system in Korea in which tenants pay a large lump-sum deposit (usually about 70% of the property value) for two years' worth of rent and landlords pay back the deposit when the contract ends. Jeonse fraud is a case where the tenant (the guaranteed creditor for the deposit) fails to receive the deposit back without a justifiable reason within one month after the termination of the lease contract, or where an auction or public sale is conducted on the property of the lease during the lease contract period, and the tenant does not receive the deposit back after the distribution. Recently, reports of Jeonse fraud filing have increased in a few specific neighbourhoods, mainly in the Seoul metropolitan area.

Usually, when house prices rise and the Jeonse market operates normally, returning Jeonse deposits does not cause major problems because it is not difficult to find new tenants, and the deposit also increases accordingly with rising housing prices. However, property prices have plunged sharply compared to two years ago, and landlords have to lower the Jeonse prices and fill the gap with their own funds. To make things worse, because Jeonse fraud has emerged, tenants are increasingly avoiding Jeonse which is making it more difficult for landlords to find replacement tenants.

Jeonse fraud is on the rise

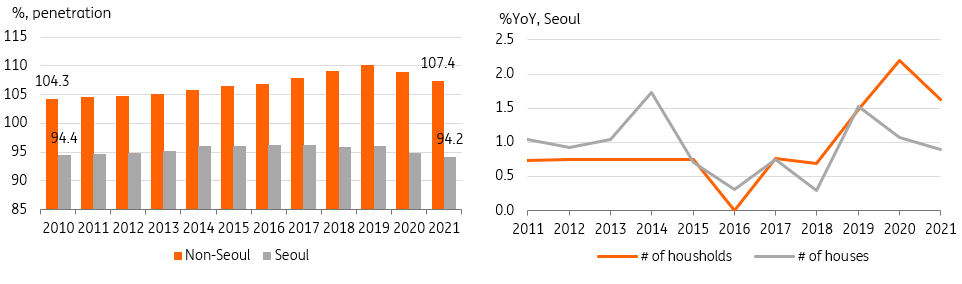

We expect the weak housing market to continue this year, but there will be regional differentiation. Nationally, the housing supply is slightly higher than the number of households in terms of the penetration ratio. It is true that the ratio began to decline in 2019 as housing supply growth failed to keep up with the increase in the number of households, but it still exceeded the 100 level as of 2021. Thus, there is a slight oversupply of housing across the country. However, if we look at Seoul, which has the largest population, the supply shortage remains as the penetration ratio fell below 100.

In terms of home ownership, there is still quite significant room for the housing market.; in South Korea, about 44% of households do not own their own homes, and when it comes to Seoul, this number goes up to about 51%. Therefore, there is still demand for home ownership.

Housing market to be differentiated: Seoul vs non-Seoul

That’s why we believe that unsold units in the non-Seoul area will be a major issue and it will take several years to digest those units. Those cities’ penetration ratios are already over 100, and excessive supply of new housing will likely deteriorate the real estate market and prices will likely decline further. The number of unsold units in Seoul has not increased meaningfully as the demand for housing is relatively strong compared to other places.

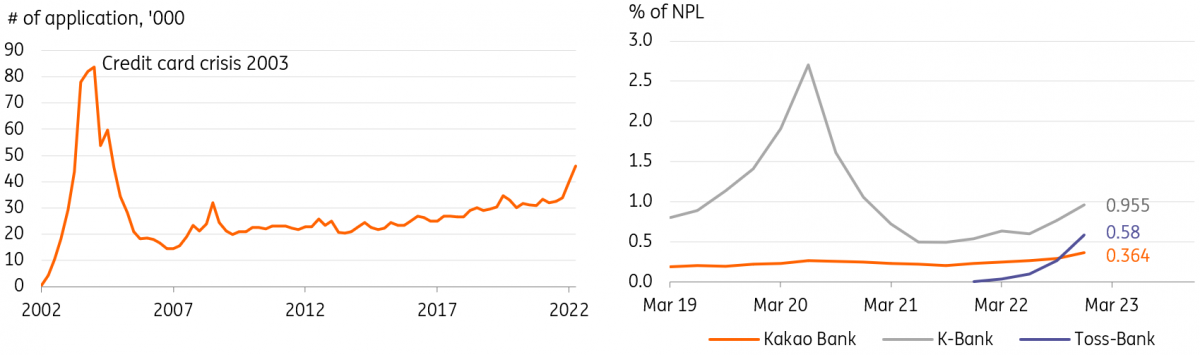

Other than supply and demand components, poor household credit conditions are another reason why we expect a bear housing market this year. The delinquency ratio has increased over the past few quarters as some of the Covid relief programmes have gradually unwound. An early indicator – the internet banking delinquency ratio – has jumped quite significantly.

As a small portion of internet banking, we do not think this will trigger systemic risk, but it clearly shows that households are suffering from tight credit conditions. Also, the number of applications for personal debt restructuring has increased more than 40% since early last year, the fastest rise since the 2003 credit card crisis in Korea. Major banks have set aside enough provisions and have preemptively managed risks, thus we think the current level is still manageable by the banks.

Household credit conditions are clearly deteriorating

The Bank of Korea is expected to react to the financial market stress driven by the poor housing market

With the rapid rise in the delinquency ratio and defaults, the Bank of Korea will likely consider financial stability a policy priority.

With a sudden drop in construction starts and permits, domestic demand growth is expected to weaken in the current and next quarters. And with household credit conditions deteriorating and PF-related stress worsening, we expect the sub-par level of growth to continue throughout 2023.

Although there are several risk factors to anchor inflation at an elevated level – utility prices, public service prices, and other cost-push-driven price hikes – we continue to believe that inflation is likely to reach 2% in the summer with rental prices declining and the negative output gap widening. Thus, the Bank of Korea will likely shift its policy stance towards neutral mid-year, before eventually beginning to cut policy rates at the end of this year.

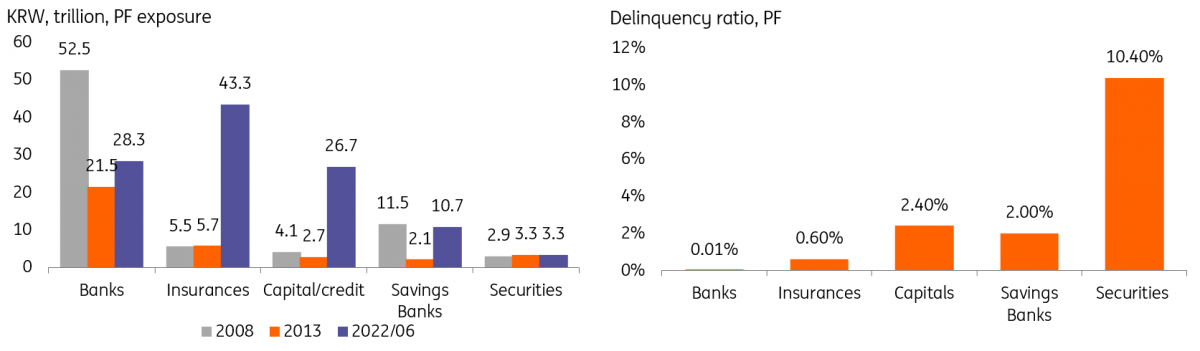

Real estate PF stress is an ongoing issue

The long-term outlook for the housing market remains promising

While we have argued that the housing market will continue to stagnate throughout 2023, we expect the next bull market to arrive in two to three years' time. As mentioned earlier, the sharp decline in current permits and starts will lead to a decline in new housing supply and by then the unsold units will be most likely cleared.

Meanwhile, on the demand side, macro conditions such as growth and financial terms are expected to normalise gradually. In addition, the underlying indicators of the housing market, such as the formation of households, homeownership, and penetration ratio, still suggest that demand for housing will pick up again. Therefore, we believe that the real estate market will thrive once again. In areas where standby demand is solid and new supply is insufficient due to a shortage of land, such as in Seoul, house prices are expected to rise relatively stronger than in other areas.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more