Striking trends in EUR credit supply

- 26 February 2021

- Credit

Supply in 2021 is off to a big start in euro. There have been some particularly interesting trends forming, such as the increase in Hybrids supply (as expected). We take a look at some of these trends

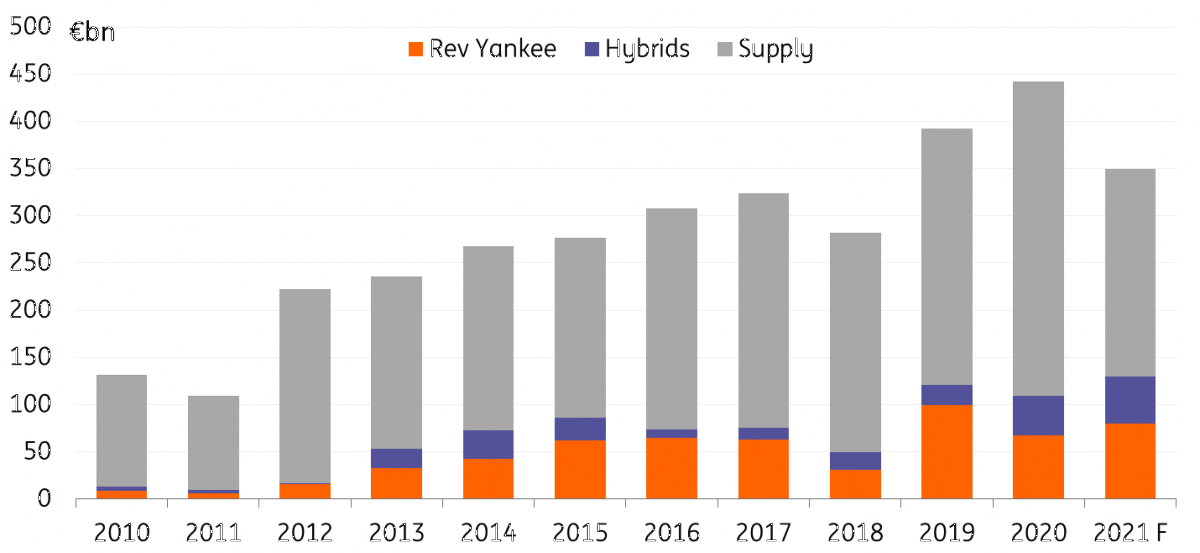

After a substantial amount of supply in January amounting to €33bn, and a further €20bn in February thus far, supply year-to-date now stands at the third-highest level on record, after the €58bn seen in the first two months of 2019 and €64bn in the same period last year. This is in line with our end of year expectations for supply to total €350bn - the third-highest amount of supply after the €393bn seen in 2019 and €442bn in 2020.

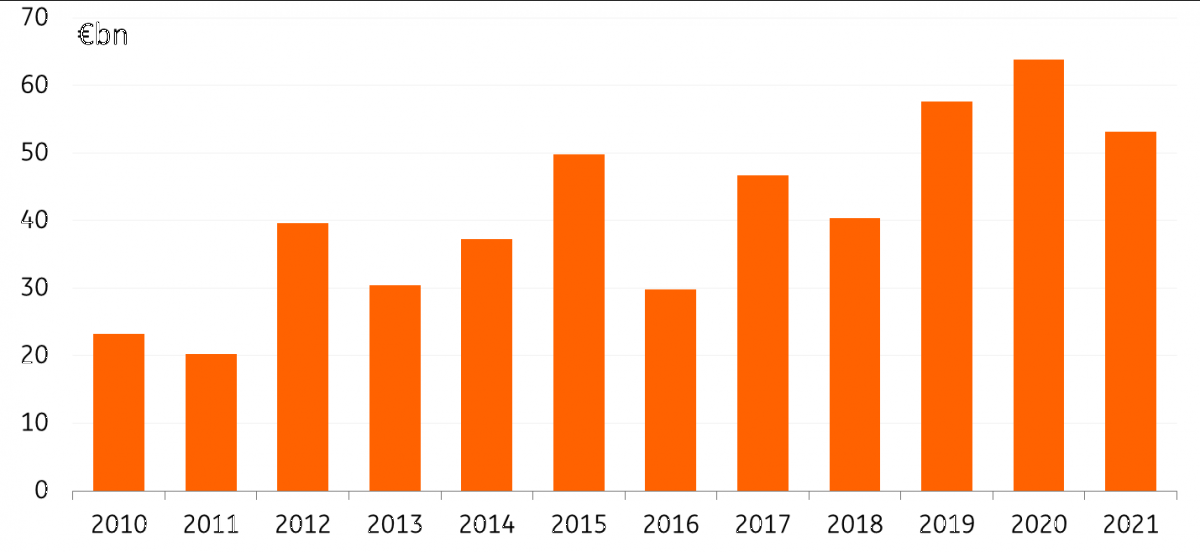

| €53bn |

Supply 2021Year-to-date |

In line with our expectations for the year

- Over the past four years, 14% of total supply for the year had been supplied by this point. Supply so far this year is sitting at 15% of our year-end forecast. We did expect larger supply in the initial months of 2021 and we are confident we can reach our target of up to €350bn by the end of the year.

- The quarterly break down for euro corporate supply will likely resemble that of 2019, whereby €100bn comes in 1Q, and another €100bn in 2Q, leaving roughly €70bn per quarter for the second half of the year.

Euro Supply per year on a YTD basis

Source: ING, Dealogic

Supply concentrates on long end | New issue premium is limited

- Most issuers have been pushed to issue at the longer end of the curve. This is a result of the current negative yield environment at the short end. In 2021, 82% of supply has been in the 6yr maturity bucket and longer while 53% has been in the 9yr bucket and longer. Nonetheless, curves are also at historically flat levels and we expect more to target the long end.

- New issue premiums have been little to non-existent this year relative to this time last year (pre-crisis) when new issue premiums were strong. Many new issues have been priced through their curves. Despite this, demand has remained strong for new bonds.

Real Estate and Energy off to a big start, whereas Consumers start slow

- The real estate sector has seen an increase this year. It is certainly the norm for real estate to do their funding at the beginning of the year. However, YTD real estate supply has amounted to €12bn, which is a big increase on the €4bn supplied over the same period in 2019 and €8bn in the first two months of 2020.

- The energy sector has also seen an increase in supply thus far, up to €14bn YTD relative to €8 and €9bn from the past two years. This however was expected as many oil & gas names required large financing. We have pencilled in a forecast of €75bn for the year.

- The consumer sector is seeing very little supply so far this year with only €2bn YTD. This is a big decrease relative to €10bn over the same period last year and €9bn in the first two months of 2019. Our forecast for consumers is €50bn, which is considerably lower than the €67bn last year.

Corporate Hybrids see a substantial start - more where that came from

- Corporate hybrids' supply is up significantly to €10bn YTD versus €6bn last year and just €3bn in 2019. We forecast hybrid supply to reach at least €50bn, if not higher. Many corporates will issue hybrids for rating defence predominantly. Additionally, first call dates rise in 2021 and remain high for the coming years, suggesting a large amount of called hybrids and refinancing is then needed.

Reverse Yankee supply slow out of the gates, but we expect a late sprinter

- Reverse Yankee supply is off to a very slow start thus far, with just €6bn in supply, relative to €20bn in 2020 and €13bn in 2019. The cross currency basis swap and 3m v 6m roll are at very tight levels at the moment which normally attracts Reverse Yankee supply. However, more important is the USD EUR spread differential, when this is wide it offers a nice cost saving advantage to US corporates to issue in EUR. Over the past six weeks, USD spreads have been tightening at a quicker rate than EUR spreads. This results in a tight spread differential. However, we do expect this to change, and see USD spreads underperforming against EUR, once more offering a very attractive cost saving for Reverse Yankee supply.

High supply from Hybrids and Reverse Yankee means less eligible supply

- Our forecast for Reverse Yankee supply is €80bn for 2021. With the addition of €50bn for corporate hybrids, the supply of ECB eligible debt will be considerably lower in 2021. This will prove supportive for eligible debt, and will likely see the European Central Bank pushed into the secondary markets.

- On a YTD basis, 11% of supply has been Reverse Yankee and 20% has been in corporate hybrids. This is a different picture to what we expect for the end of the year. We forecast roughly 23% to be Reverse Yankee and at least 14% to be in corporate hybrids.

Build up for euro supply per year

Source: ING, Dealogic

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

26 February 2021

The striking trends in US and EUR dollar supply

- This bundle contains 2 Articles