Hormuz oil shock tilts shipping towards alternative fuels

- 13 May

- Energy Transport & Logistics Sustainability

The current oil price shock is making alternative fuels more cost competitive in the shipping sector. LNG benefits the most, becoming even more attractive compared to conventional bunker fuels. Methanol is also becoming more viable, strengthening the case for methanol-ready vessels. Still, the emissions benefits remain limited

Alternative fuels more attractive now as oil shoots higher

The Middle East conflict and blockade of the Strait of Hormuz have disrupted oil supply and pushed shipping fuel prices, like marine gas oil (MGO), sharply higher. In this environment, fuel strategy is no longer just about cost, but also about securing supply and managing price risks. At the same time, higher prices and greater uncertainty are shifting the relative economics of alternative fuels, even as regulatory progress has slowed with the delayed introduction of a global carbon price under the IMO’s Net Zero Framework.

Prices for Marine Gas Oil spiked due to the closure of the Strait of Hormuz

MGO bunker prices in Rotterdam in $ per tonne; we’ll analyse two scenarios

Our modelling shows how the costs and economics of renewable fuels of non-biological origin (RFNBOs) – also called synthetic or e-fuels – change in a high oil price scenario, from a Northwest European perspective. The Middle East war has squeezed the supply of oil and oil products. LNG is similarly affected, but less so, as more capacity is coming online, and natural gas continues to be supplied through regional production and pipelines.

Our analysis translates the current geopolitical risk into a simple message for shipowners and cargo owners: when oil products spike and gas rises less, the relative economics of LNG and (to a lesser degree) methanol and even ammonia improve quickly, even if the absolute cost of all energy carriers rises.

Decarbonisation requires shift to lower carbon fuels

While geopolitical tensions do not alter the fundamental science behind decarbonisation, and hence emissions, they do influence the economics of the business case for different fuels. Traditional marine fuels such as marine gas oil (MGO) and very low sulphur fuel oil (VLSFO) currently generate approximately 1,900 kg of CO2 per deadweight tonne for every 1,000 kilometres sailed. This carbon footprint can be lowered by transitioning to alternatives like LNG or synthetic fuels, like methanol and ammonia. However, meaningful climate benefits are achieved only when vessels use the green or blue variants of these synthetic fuels. Just switching to grey methanol or ammonia would only worsen the footprint to 2,500 or even 4,000 kg of CO2.

LNG and blue and green versions of synthetic fuels can reduce carbon emissions from shipping

Indicative well to wake emissions for different shipping fuels in kilograms CO2 per deadweight tonnage per 1,000 kilometres (kgCO2/DWT/1,000km)

Structural changes in fuel prices can significantly influence how and when alternative solutions are adopted within the shipping industry. To assess this impact, we examine the impact of current high prices on the business case for oil and gas-based shipping fuels and synthetic fuels like methanol and ammonia. The duration of elevated fuel prices remains a subject of intense discussion and is closely tied to ongoing geopolitical developments surrounding the closure of the Strait of Hormuz, as well as the potential damage to oil and gas infrastructure in the Middle East from further conflict. You can find our most recent scenario analysis here. In this article, we set aside geopolitical factors and focus solely on how sustained higher prices affect the cost dynamics of various fuels.

When oil products remain high, LNG becomes more attractive

In the high-price scenario – the one most relevant under a continued Hormuz disruption – oil products become the big movers:

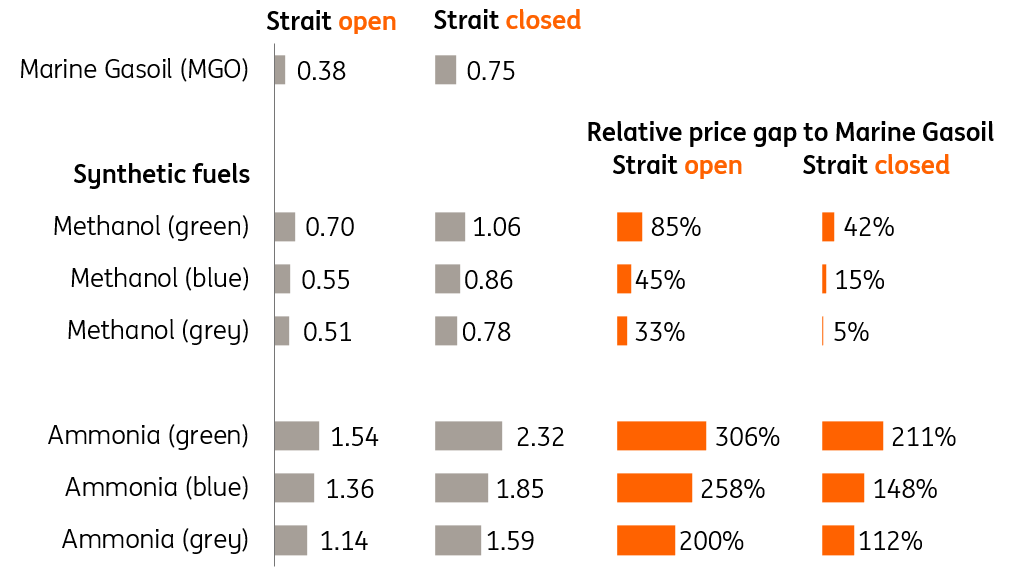

- MGO rises from 0.38 to 0.75 $/DWT/1,000km (+97%)

- VLSFO rises from 0.30 to 0.61 (+103%)

- LNG rises from 0.25 to 0.41 (+64%)

The key mechanism is that the high case hits oil products harder than gas and power inputs. LNG becomes the most attractive “available now” hedge. In other words, the Hormuz-driven oil shock makes LNG not only a transitional decarbonisation option, but also commercially the most attractive option.

Hormuz disruption strengthens LNG’s position as synthetic fuels lag on cost

Indicative unsubsidised fuel costs in $/DWT/1,000km

Methanol gains traction faster than ammonia

Over the last three years, methanol has outpaced ammonia in commercial momentum in deep-sea shipping. There are four practical reasons:

- Engine and vessel adaptation is simpler and faster. Methanol can be used in internal combustion engines with fewer “system-wide” changes than ammonia, which require more extensive redesign and new safety systems.

- Bunkering and handling are more straightforward. Methanol is a liquid at ambient conditions, which reduces complexity compared to ammonia configurations.

- A “ready now / ready later” option exists. Orders for methanol-capable and methanol-ready dual-fuel vessels have become a pragmatic bet: shipowners can run on conventional fuels today and switch as low-carbon methanol supply grows. It is also a hedge against the possibility that policy pushes faster toward low-carbon fuels than infrastructure.

- From a cost perspective, methanol is currently more attractive than ammonia.

Methanol’s CO2 footprint signals a downside; only blue and green deliver progress

Methanol still contains carbon, which is emitted as CO2 when burned. This limits its CO2 reduction potential compared to ammonia, which is carbon‑free at the tailpipe. Only blue and green methanol deliver emission reductions relative to MGO and VLSFO and even then, the emissions reduction seems to be modest compared with LNG, at least in our framework, where methanol is currently predominantly produced from natural gas in Europe, compared to biomass (as a future green alternative), or coal (common practice in China). This matches our earlier warning: synthetic fuels can increase emissions if they are produced in a non-sustainable way, because the production chain is energy-intensive and the carbon intensity of inputs dominates outcomes. The economics and climate credentials of gas-based methanol remain challenging compared to LNG, even when produced as blue or green variants.

Methanol’s biggest strategic value may be its optionality. When oil-product prices become more volatile, the value of being able to switch fuels - or at least switch procurement strategy – rises. That is precisely where dual-fuel capability becomes more than a decarbonisation story; it becomes a resilience story.

The oil shock narrows the methanol–oil price gap

Our model outputs show that higher prices for bunker fuels narrow the gap between methanol and marine gas oil (MGO). MGO roughly doubles in price, while methanol rises by about 50–60%. So relative competitiveness improves for methanol: while it is still more expensive, the distance between oil and methanol shrinks. But two important caveats remain. Oil products like MGO and VLSFO remain cheaper than blue and green methanol.

Price premium of synthetic fuels has narrowed now that oil prices are higher

Indicative unsubsidised fuel costs in $/DWT/1,000km

Why blue methanol is probably the attractive variant

Given that the green hydrogen market is still stuck in a pilot phase, blue methanol is a plausible near-term stepping stone: it scales earlier because it depends on gas plus CCS rather than small scale electrolysers. This “blue-first, green-later” pathway is also consistent with how many heavy-industry transitions unfold: deploy the imperfect-but-better option first, then upgrade as clean technologies become cheaper and renewable power becomes more abundant.

Ammonia remains on the radar: expensive now – promising in the long run

Ammonia is expensive in its blue and green variants, but this would offer strong climate benefits and real progress in CO2-reduction. Despite its challenging economics and inherent toxicity, market participants have not dismissed it as a viable option. The perception seems to be shifting from probably not to probably yes. But efficient usage is also a longer-term bet. Participants in the shipping sector now mostly refer to grey ammonia, which is already abundantly available for other purposes. But then again, this comes with more emissions, so it should not be viewed as a sustainable solution. However, overtime, blue and green variants could become more attractive if costs come down and carbon pricing is introduced.

LNG holds the best cards

LNG still looks like the stronger near-term route for ship owners, based on our numbers, because it combines lower emissions with lower costs compared to oil products. So, the Middle East oil supply crunch could accelerate a shift away from conventional fuels without necessarily accelerating a shift to synthetic fuels, like ammonia and methanol. It rewards the “closest substitute” that is available at scale, which is LNG.

That creates a strategic tension for the sector and for policymakers: energy security and cost pressures may drive faster adoption of LNG, while net-zero targets still require a ramp-up of truly low-carbon fuels like biofuels and synthetic fuels from blue and green production routes.

LNG vessels offer future flexibility for conversion to ammonia

While ammonia presents certain safety challenges, it holds significant long-term promise as a shipping fuel. The possibility of converting LNG-capable vessels to run on ammonia in the future enhances their strategic value, providing shipowners with greater flexibility. Investing in LNG-powered vessels is not only a cost-effective and lower-emission option in the near term, but also future-proof fleets, by allowing for a smoother transition to ammonia as technology and regulations evolve. As gas-propelled vessels, these ships can be adapted to operate on ammonia, supporting both decarbonisation goals and resilience in a changing energy landscape.

General momentum slowed amid policy headwinds

The total orderbook in global shipping also confirms that LNG leads as an alternative fuel. In May this year, 28% of the over 7,000 vessels on order are capable of running on alternative fuels, over half this share can run on LNG (15%). Methanol comes second, with particularly recent investments by several container liners.

After a post-pandemic acceleration, we saw orders for ships capable of running on alternative fuels slowed in 2025. During the second Trump administration, the United States shifted its policy and effectively lobbied International Maritime Organization (IMO) members to oppose the adoption of global measures aimed at advancing the industry’s climate ambitions and implementing a carbon pricing mechanism. Against this backdrop, companies – including frontrunners like Maersk - are still pursuing a diversified strategy and keeping their options open.

All eyes on IMO as shipping needs a global carbon price to decarbonise

The IMO’s Marine Environment Protection Committee is still discussing a framework to deliver on the previously agreed net-zero target (NZF) for 2050. The proposal agreed in 2025, which has since been postponed by member states, includes a carbon price of $100 per tonne of CO2 for emissions within the baseline, and $380 for non-compliance (we discussed the details here). Such a system could further narrow the cost gap with synthetic fuels and help pass additional costs along the value chain. After a year of delays, adjustments to the 2025 proposal now appear likely as stakeholders seek a compromise. However, it remains uncertain whether a final agreement will be reached.

It's important to keep in mind that shipping costs typically represent less than 5% of overall product costs that are being shipped. The high efficiency of shipping means that even if these costs increase substantially, the impact on end consumers is minimal and the price premium is barely noticeable for most products. However, this dynamic is quite different for shipping companies and charterers, which are directly affected by rising operational expenses. As such, effective policies are essential to address these challenges within the industry.

Cost, security and climate goals

In the current environment, shipping owners face significant uncertainty, as geopolitical tensions around the Strait of Hormuz continue to drive volatility in bunker fuel prices, like marine gasoil (MGO). Elevated MGO prices are narrowing the cost gap with synthetic fuels such as methanol and ammonia, at least in Europe. However, LNG stands out as the most cost-effective option, solidifying its position as the preferred fuel choice. Amid the ongoing conflict and unpredictable fuel availability, we expect shipping companies to look beyond cost considerations. Dual-fuel capabilities, diversified bunkering access, and flexible contracts that permit fuel switching are increasingly valuable strategies, especially if high prices persist. This dynamic is expected to accelerate orders for LNG, and methanol-ready vessels, supporting operational resilience while helping to future-proof fleets against further market disruptions. It may also help shipowners meet their climate targets by significantly reducing vessel emissions.

Appendix: scenario assumptions and model explainer

Two commodity price scenarios for the shipping sector from a Northwestern European perspective

Model explainer

Indicative emissions are modelled for an 82,000 deadweight tonnage (DWT) vessel, assuming 230 sailing days per year at an average speed of 12.5 knots. The analysis adopts a full life-cycle perspective, covering both well-to-tank (fuel production) and tank-to-wake (onboard combustion) emissions.

Natural gas is assumed as the primary feedstock for grey and blue methanol and ammonia, reflecting current production in Northwest Europe. As a result, no emission reductions from biomass or Direct Air Capture (DAC) are included. While these lower-carbon sources could be deployed in future pathways, particularly for methanol, they would come at higher cost and result in lower overall emissions compared to our figures. In this analysis, the “colour” reflects the pathway used to produce hydrogen: grey hydrogen is derived from unabated natural gas; blue hydrogen combines natural gas with carbon capture and storage (CCS); and green hydrogen comes from electrolysis powered by low‑carbon electricity.

For blue production routes, a CO2 capture rate of 80% is assumed. The relatively limited electricity demand in grey and blue pathways is assumed to be met by grid power with a carbon intensity of 200 kg CO2/MWh, broadly representative of the Netherlands and Belgium.

For green methanol and green ammonia, it is assumed that electrolysers are fully powered by low-carbon electricity (renewables, hydro or nuclear), sourced via Power Purchase Agreements (PPAs).

Emissions are expressed per tonne-kilometre, ensuring comparability across fuels.

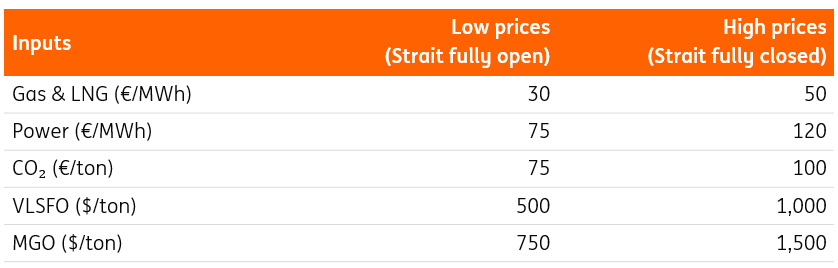

In addition to the assumptions underpinning the emissions' analysis, we’ve used different economic assumptions for a world where the Strait of Hormuz opens or remains closed. Synthetic fuel costs are modelled using different values for gas, power, carbon and marine fuel prices (see table), while an exchange rate of €1 = $1.18 is used in both scenarios.

Hydrogen production is assumed to take place within a 50km radius of methanol and ammonia plants, with transport via pipeline. This results in hydrogen costs of €1.80/kg (grey), €2.00/kg (blue), and €4.50/kg (green) in the low price environment and €2.70/kg (grey), €3.10/kg (blue), and €6.65/kg (green) in the high price environment.

Finally, the results reflect fuel costs only and exclude vessel capex and opex, so they do not represent total cost of ownership.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more