Sticky inflation hurts Austria’s competitiveness

- 12 July 2023

- Eurozone Quarterly Austria

While other eurozone countries are recording significant declines in headline inflation, the downward trend in Austrian inflation is, optimistically speaking, sluggish. This decreases Austria's attractiveness, both in terms of industry and tourism, and will ultimately lead to a decline in the country's competitiveness

Better than expected, but far from good

After the first flash estimates indicated that the Austrian economy had contracted slightly by 0.3% quarter-on-quarter in the first quarter of 2023, the final revision revealed a small increase of 0.1% quarter-on-quarter, which could be considered stagnation rather than growth. While the construction sector and other economic services supported economic activity in the first three months of 2023, the slowdown in activity in the manufacturing, trade and transport sectors had a negative impact.

As in the rest of the eurozone, Austria is witnessing a divergence between industry and services. Looking ahead, however, this divergence doesn’t look sustainable. In fact, due to the loss of consumers' purchasing power and accelerating service inflation, the outlook for the services sector is also expected to become gloomier.

Sticky inflation to weigh on services sector

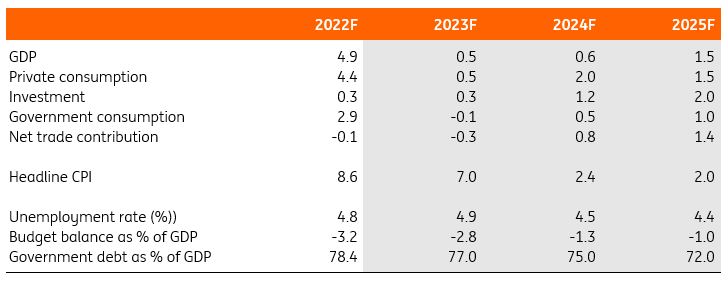

While other eurozone economies have recorded significant declines in headline inflation, the downward trend in Austrian inflation has been sluggish so far. In June, headline inflation in Austria came in at 7.8% year-on-year, against 5.5%YoY in the eurozone. Compared with the peak reached in October last year, headline inflation in the monetary union fell by 5.1 percentage points. In Austria, the decline in headline inflation between October 2022 and May this year was 3.8 percentage points only – the disinflationary trend beginning to unfold in other eurozone economies is being sought in vain in Austria.

This will affect the service sector in two ways. First, private consumption will suffer from persistently high price levels, especially since part of the cost of living is determined by administered prices, which in Austria are mostly indexed and thus increased based on inflation. This applies, amongst others, to public services, the rent of social housing or telecommunications. Moreover, services inflation is tending to accelerate, and there is no sign of an easing of price pressures in the sector.

Second, persistently high inflation will cause Austria's tourism sector to lose competitiveness. The hotels and restaurants component of the inflation basket recently became 13.1% more expensive year-on-year, and recreation and culture went up by 7%. In the eurozone, inflation in these categories was 8.4% and 5.7% respectively. If tourism in Austria becomes significantly more expensive than in other eurozone countries, tourists might switch to other holiday destinations.

Inflation in the services sector is also likely to be amplified by wage increases. Wages in the Austrian accommodation and food services sector increased by around 28% between the fourth quarter of 2019 and the first quarter of 2023. In the eurozone, wages in the sector came up by 16% over the same period. Strong wage growth in this sector was probably the result of a particularly high lack of skilled workers.

Austria's competitiveness will suffer

Increased costs are having a negative impact on competitiveness, not only in services but also in the manufacturing sector. Most Austrian exports are machines and vehicles, followed by processed goods and chemical products. While the competitive outlook for vehicles has improved recently, the results of DG ECFIN's industry survey in both the energy-intensive chemical products sector and the machinery sector point to a loss of competitiveness, both in relation to countries within and outside the EU.

Until the green transformation has comprehensively arrived in Austrian industry, no growth miracles are to be expected for Austrian industry or foreign trade. Consequently, the overall economic outlook is far from rosy. We expect economic growth in Austria to be significantly below potential both this year and next. Accordingly, the government debt ratio, which stood at 78.4% at the end of 2022, is likely to decline only slowly. After all, despite the frequent calls for a return to budget discipline, there has been no talk so far of either tax increases or significant spending cuts.

Overall, the outlook for the Austrian economy is clearly clouded and persistently high inflation will be an additional burden this year and next.

The Austrian economy in a nutshell (%YoY)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Eurozone Country Update: More accidents on the road to recovery

- This bundle contains 13 Articles