Stark differences persist in fibre coverage across Europe

- 1 February 2024

- TMT

As was the case in previous years, there are stark differences in fibre connectivity across Europe. However, many of the laggards will continue to catch up in 2024

Significant investment required to meet Digital Decade goals

Europe’s Digital Decade is in full swing, yet the ambitious connectivity goal of delivering Gigabit download speed to all European households in 2030 looks like a tough task, even though millions of new homes are covered by fibre every year. Recently, a report commissioned by the European Commission found that around €114 billion needs to be invested to achieve the Gigabit coverage goal, and that €33.5 billion is necessary to achieve mobile goals (WIK-Consult). This adds up to a €148 billion investment. But depending on the deployment mode, €26 to €79 billion is required for the main transport paths. This makes for a total investment gap of €174 billion, based on the least costly deployment mode.

In short, private sector investments, as well as public funds (i.e. CEF Digital and the Recovery and Resilience Facility), are necessary to achieve Europe’s lofty connectivity goals.

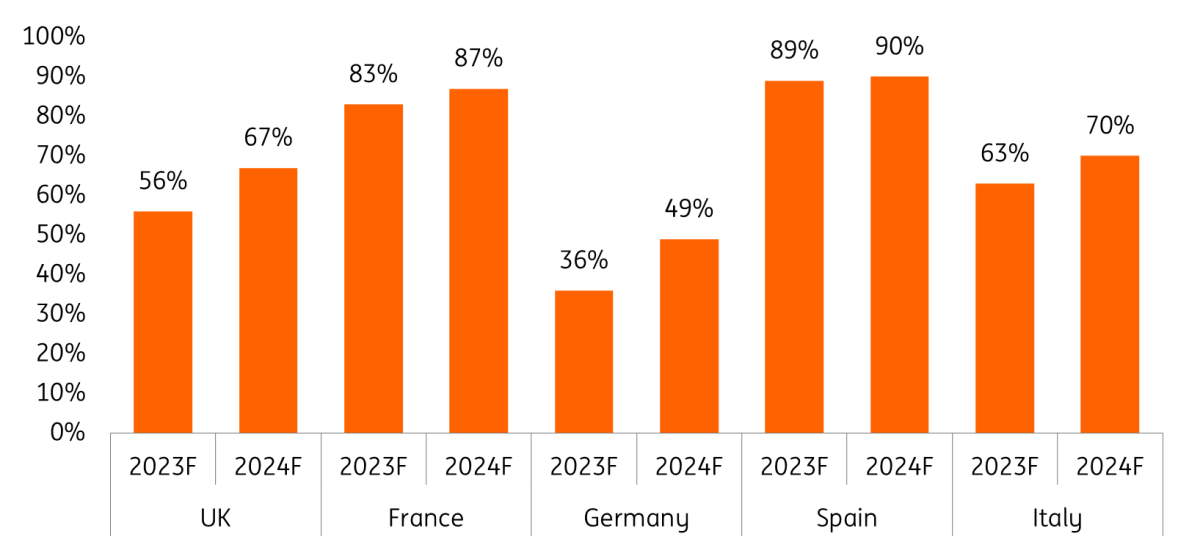

- Additional investment is particularly required in Belgium, Germany, and Greece, where less than 30% of homes were connected to fibre in 2022 (FTTH Council Europe).

- This stands in stark contrast to Lithuania, Portugal and Romania, which had connected roughly 90% of their households to fibre at the end of 2022. The difference is largely explained by lower costs per premises in South and Eastern Europe, which is why networks overlap more often.

- In France, which is also ahead of the curve, early coordination by local authorities proved very efficient. However, based on recent trends and reports, we estimate that many European laggards are currently making quick strides forward.

- In Germany, for instance, we estimate that it will have nearly half of all homes passed at the end of 2024. We expect a similar acceleration in the UK, where we estimate that two-thirds of all homes will be passed at the end of this year.

Interest rates, wage increases and competition make closing the investment gap more difficult

After an all-time high in 2022, there was slightly less activity in fibre financing markets in 2023. This is driven by three factors, the first of which is higher interest rates. As the sector is mainly debt-financed, much of the interest rate risk is hedged by undrawn facilities. However, the cost of additional financing, which is sometimes necessary, has increased, which also holds for a renewal of the financing.

Second, labour costs have gone up due to wage increases, which makes new networks more costly to build. In addition, overbuild risk in very developed fibre markets makes new networks in densely populated areas a more challenging endeavour.

Third, there is stiff competition in the fibre market, which means that money is also used to acquire new customers on existing networks next to building networks in new areas. However, there is still a lot of demand for better and faster connections with fibre, and the long-term prospects for fibre to the home, once the economy exits its current choppy waters, are good.

New homes are still passed at an impressive rate

Despite a slower financing environment, new homes are still being passed at an impressive rate, as mentioned previously. We have calculated, based on data from the FTTH Council Europe, that 93% of European (EU-27 and UK) households will have fibre coverage in 2028, up from 55% in 2022. To meet this forecast, a lot of work remains to be done. The signs are promising, however, as we expect many European laggards to catch up quickly in the years to come. We do not just expect companies in the five largest countries to invest significantly in the fibre rollout, but those in other European countries as well. Moreover, private-public partnerships are showing promise. In Belgium, for instance, Proximus, together with the Belgian Infrastructure Fund, plan to bring fibre to an additional 1.7 million homes on top of existing rollout plans which would extend coverage to 95% of Belgian households. In short, the European fibre rollout is progressing at speed, in spite of challenges.

Percentage of passed homes expected to keep growing

Consumer demand for fibre connections is also growing

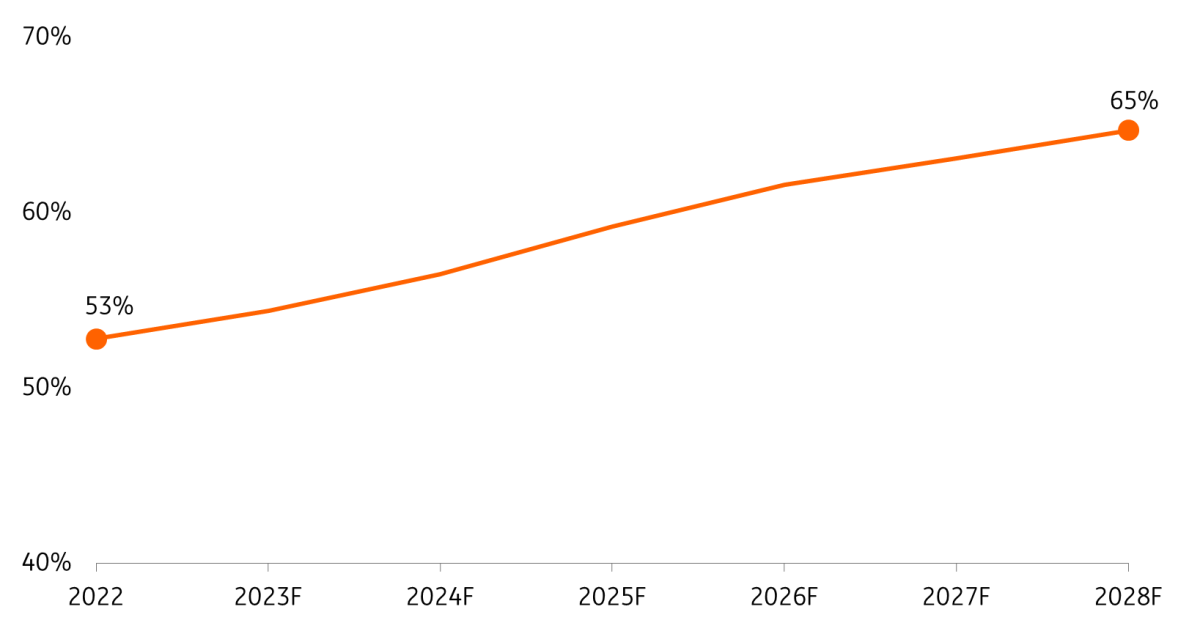

In 2012, only 30% of households were connected to fibre networks. Currently, the take-up rate is 53%, and we expect this to keep increasing for the foreseeable future. Consumers value the fast connection that fibre offers, for instance, for video conferencing and video games. It is also important for service providers because profitability increases with higher take-up rates. By 2028, we expect the take-up rate to be 65%, in line with the expectations of the FTTH Council Europe.

Usage of fibre networks will keep increasing

Percentage of people that subscribe to fibre when available

Outlook for fibre rollout looks bright in spite of challenges

Many companies have ramped up their fibre rollout efforts. We expect the percentage of homes passed in countries that currently lag behind in the fibre race to increase by (near) double digits in 2024. We should thus see strong growth in Germany, the UK especially, and to a lesser extent, Italy. This is driven by consumer demand and the connectivity goals of European governments. Thus, the fibre rollout will continue at speed in spite of increased interest rates, higher labour costs, and the risk of overbuilding. In the longer term, after 2028, we expect the fibre rollout to slow down. This is because it is prohibitively expensive to cover rural areas with fibre, especially if very large distances need to be covered. In those cases, fixed-wireless access or satellite connections can offer suitable alternatives.

In short, the fibre rollout will continue at pace in 2024, despite challenges.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Telecoms Outlook 2024: Stepping into the future

- This bundle contains 8 Articles