Spanish food and agriculture sector set for a post-inflation recovery

- 15 September 2023

- Commodities, Food & Agri Spain

Production in Spanish food manufacturing has come under pressure this year. Unfavourable weather has led to supply constraints, while the surge in food prices is dragging on consumer demand. The combination of subsiding inflation rates and wage increases will lift disposable incomes, providing an opportunity to recover some ground in 2024

Spain's food sector feels the pinch

Spain's food sector – while less cyclical than sectors such as tourism or construction – is not immune to the current economic slowdown and rising inflation. It has also been impacted by extreme weather conditions that have affected the harvest of certain food products.

The impact on Spain's food processing sector has been significant – up until July, production levels were showing a 2.5% decline from the previous year, due to reduced domestic and international demand.

Signs that consumers have been buying less have been around for a while. Food and beverage retail sales volumes decreased by 1.7% in 2022 and remained under pressure in the first quarter of 2023, according to the national statistics agency INE.

Consumer spending on food and drink has likewise been hit across Europe, although unlike other EU countries such as Germany and the Netherlands, food retail sales volumes in Spain have been picking up since the spring, partially thanks to a strong influx of tourists.

While we expect Spain's food sector to go into contraction, we see diverging trends between subsectors. Output at processors of vegetable oils, fresh produce and grain mills have shrunk more sharply as they have suffered from weather and harvesting conditions. The fish processing industry has been affected by sharp price increases for energy and operational costs, while higher selling prices curb fish consumption. In contrast, output in some other subsectors (meat, bakery, beverages, dairy) has shown much more resilience. Basic food products are generally less price-sensitive than other food products.

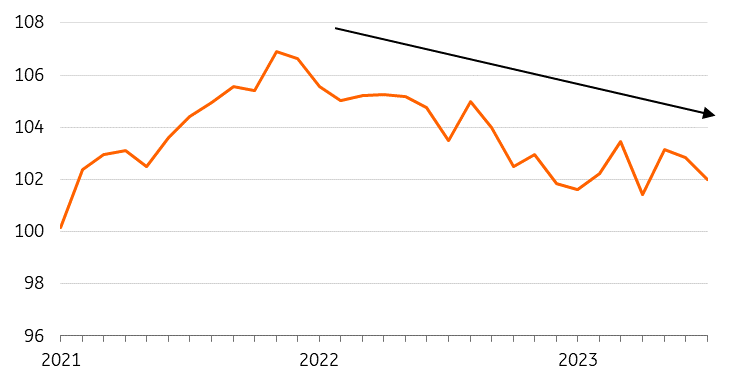

Production in Spanish food manufacturing has been falling since 2022

Index of production, seasonally and calendar adjusted data

Food price increases are slowing down

Despite the ongoing challenges, there are hopeful signs on the horizon. In a recently published ING report on food inflation trends in both Europe and the US, we wrote about how food price rises are subsiding on a month-on-month basis in Europe, although the pace differs per country. Spain seems to be lagging somewhat. A larger share of Spanish food producers plan to raise their prices further compared to their German and French counterparts.

Although Spanish food inflation is expected to continue to fall, it will ease more slowly than in other eurozone countries. Nonetheless, this will still provide some respite for Spanish consumers who have faced a significant 25% increase in their grocery bills over the past two-and-a-half years.

Higher food prices take their toll on the family budget

Increased food prices are forcing Spaniards to spend an ever-larger chunk of their budget on food and groceries. Almost two-thirds (63%) of Spaniards indicate that they spend a greater proportion of their income on food today than they did five years ago, according to a survey by IPSOS conducted in June on behalf of ING.

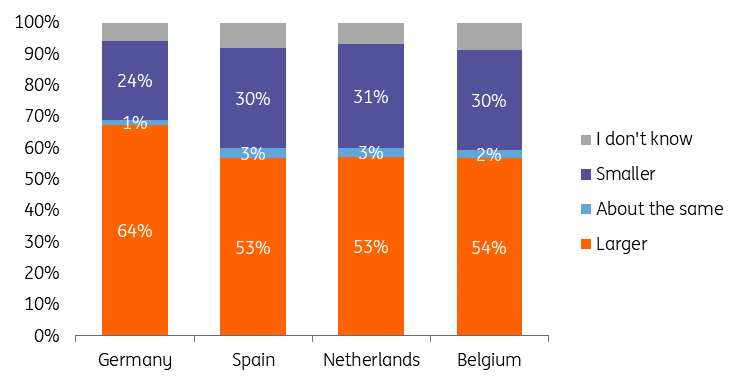

More than half (53%) of Spaniards expect the share of their income going to food and groceries to rise even more in the coming years. The Spanish figures match those of Belgium and the Netherlands, which were also included in the survey, but are still much lower than those in Germany.

To keep costs down, many consumers are changing their shopping behaviour. Within the meat category, poultry and frozen meat sales are growing and replacing more expensive beef. In dairy, some leading European producers reported declining sales volumes in the first half of the year, with value-added products like quark or speciality cheeses showing a higher elasticity than staples like milk.

Meanwhile, higher prices for fruits and vegetables tend to lead to lower sales volumes, in part because consumers opt for processed products instead of more expensive fresh products. Sales of fresh fruits, vegetables and potatoes dropped by around 4% in Spain (up until May) and by 2% in the Netherlands (up until June) for example.

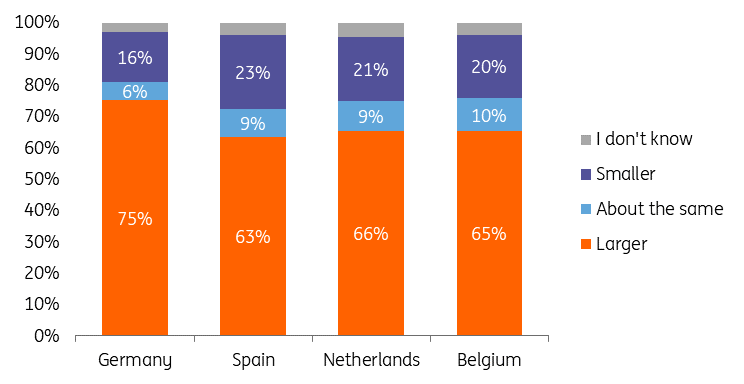

Consumer survey shows consumers now spend a larger share of their income on food...

'Compared to five years ago, the share of my net income going to food and groceries is...'

... and the majority of those polled also expect to spend a larger share on food in the future

'I expect that within five years, the part of my net income that goes to food and groceries will be…'

The outlook for household consumption will gradually improve

Private consumption was the main growth driver for the Spanish economy in the second quarter of 2023. This was due to a combination of easing price pressures and rising nominal wages, which had a positive impact on household purchasing power. While we think consumption will continue to make a positive contribution to growth, we expect tighter financing conditions and weaker labour market dynamics to dampen consumption somewhat in the second half of 2023.

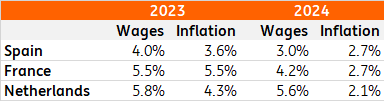

Next year, when the headwinds from these factors subside and nominal wages again rise faster than inflation, consumption may pick up further. For Spain, we expect average wage growth of 4% in 2023, followed by another 3% in 2024, both above inflation.

Under this scenario, Spanish household food consumption will be able to recover cautiously in the coming year. This offers branded food producers an opportunity to regain lost market share and volumes. The gradual improvement in household finances, combined with an anticipated upturn in promotional activities by both food manufacturers and retailers, is expected to boost food sales volumes.

Wage growth is expected to surpass inflation in Spain, France and the Netherlands

Forecasts for wage growth and inflation

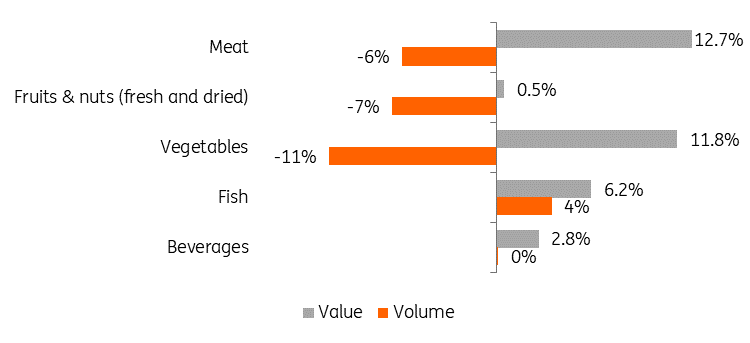

Spanish food export volumes take a hit in 2023

In addition to domestic food consumption, pressure on food exports is also increasing. While the value of Spanish food and beverage exports rose by 8% to €31bn in the first half of 2023, this increase was driven solely by higher prices, as export volumes contracted by 10% over the same period. Both lower foreign demand and lower domestic supply following exceptionally dry and hot weather have weighed on Spanish food exports.

Meat exports in particular have experienced problems due to a decline in pork exports to non-EU markets, such as China. At the same time, increased production costs and unfavourable weather conditions resulted in a decline in the trade of fresh fruits and vegetables. Exports of essential products such as citrus, peppers, tomatoes and strawberries all fell in the first half of the year.

It is very likely that volumes will remain under pressure until 2024 considering that many producers expect consumer demand to remain muted during the final stretch of this year. Meanwhile, on the supply side, forecasts for the upcoming citrus fruit and olive oil campaigns point to another disappointing year in volume terms. Given Spain's role as a major food and beverage exporter, lower foreign demand is having a significant impact on Spanish food producers.

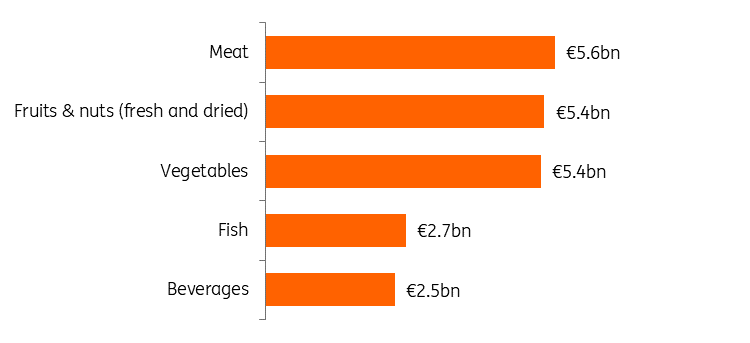

Meat, fruits and vegetables are Spain’s main food export categories

Export value in billion euros in the 1H23

Export value is generally up, but volumes have taken a hit

Growth in 1H23 compared to the same period last year

Food and agriculture will weigh on economic growth this year

The Spanish food and agriculture sector currently faces several economic challenges, including high input costs, unfavourable weather patterns, consumers whose purchasing power took a major hit last year, and sharply rising interest rates. Consequently, we expect production in the sector to contract by 1.5-2% this year. Due to slowly cooling inflationary pressures, continued wage growth, and peaking interest rates, the sector will likely be able to make up some ground next year.

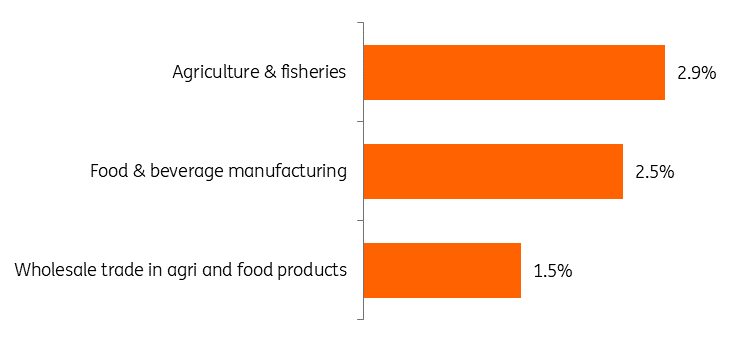

Of course, a decline in the food and agriculture sector also weighs on the country's broader economic outlook, as the sector is a solid contributor to Spain's GDP. If we look at the aggregation of agriculture, fisheries, food and beverage production and wholesale food and agricultural products, together they account for about 7% of economic activity in Spain. Since we expect a growth rate of 2.2% for the whole Spanish economy this year and 1.1% next year, the Spanish food and agri sector will thus make a strong negative contribution to the Spanish GDP figure for this year.

Food and agri subsectors account for 7% of the Spanish economy

Share in value-added output, 2021

Climate change is the biggest challenge

Although inflationary pressures remain high and will remain stubborn for the rest of the year, they will gradually normalise. The biggest challenge for the sector going forward is dealing with the impact of climate change. Changes in weather patterns are permanent and will continue to require additional action from food producers and policymakers.

With water being an indispensable resource for agriculture and food companies, there is a clear urgency to invest in measures that help to optimise water use throughout the food supply chain. For the livestock sector, measures that help to reduce heat stress on animals are equally important.

Moving up in the supply chain and diversifying sourcing are additional strategies to adapt to weather-related risks and cater to the needs of customers.

The current drop in Spanish agricultural production is being partly offset by importing more products such as tomatoes and oranges from other countries, such as Morocco and Egypt, which shows that such diversification is already taking place.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Spain’s food sector under pressure from inflation and climate change

- This bundle contains 2 Articles