Some Brexit clarity at last?

- 28 February 2018

- United Kingdom

The UK government has finally managed to craft a Brexit compromise that ministers can rally around. But the proposals have been met with a cold reception in Brussels and pressure is building on the Prime Minister to look more closely at a customs union

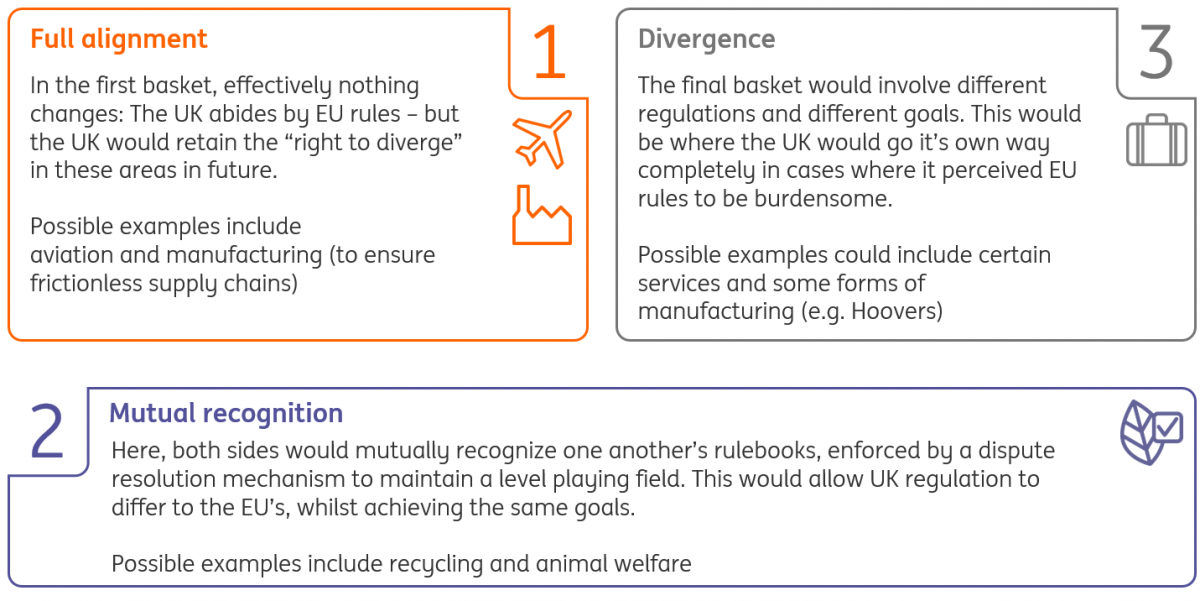

"Managed divergence" - The UK's proposed Brexit

For several months now, key ministers in the UK government have been heavily divided on the way forward on Brexit. But after a marathon 8-hour “Brexit away day”, Prime Minister Theresa May has reportedly agreed on a compromise which can unite the key factions within the cabinet. The compromise reportedly goes by the name of “managed divergence” (or “Canada plus plus plus”). We’ll have to wait until PM May’s speech on Friday for the full details, but it's assumed that this model would involve dissecting different areas of economic activity into three baskets:

How the "three baskets" approach might work

The beauty of this, in theory, is that there’s something for everyone. “Remain” ministers would be happy because it would allow the UK to remain closely aligned to the EU in key areas. And for the “Brexiteers”, it allows the government to “take back control” of regulation where it perceives EU rules to be burdensome.

Of course, it’s one thing getting UK ministers on board. Getting the EU to agree to such a proposal looks much more challenging, and in fact, the European Commission published a slide last week saying it is “not compatible” with its guidelines.

Cherrypicking is a big EU concern

From the EU’s perspective, the managed divergence proposal sounds a lot like cherry picking – a key red line for European governments, who are strongly opposed to allowing the single market to become divided up.

There are also reportedly fears that it could result in a backlash from the EU’s other key trading partners. A deal that enables the UK to excel after Brexit could embolden members of the EEA to request concessions of their own, or even make EU exit seem more appealing to some of the more eurosceptic existing member states. European negotiators will also be acutely aware that whatever both sides agree on services would also have to be offered to existing free trade partners (e.g. Canada and South Korea) under most-favoured-nation clauses.

The "three baskets" approach is unlikely to mitigate concerns over a hard border

There are practical considerations too. Reconciling the differing views of the 28 countries involved in the negotiations on exactly what sectors/areas would sit in each basket would be a very complex and time-consuming task.

But perhaps the biggest issue is that the "three baskets" approach is unlikely to mitigate concerns over a hard border with Ireland. As part of the phase I agreement back in December, the UK agreed that there would be "no regulatory divergence" between Ireland and the North. The UK's government's decision to leave the customs union, and preference to move away from certain EU rules after Brexit may not be enough to meet December's commitment.

UK reportedly banking on divisions among EU member states

Of course, none of these EU red lines is particularly new. But it's possible the UK government is banking on divisions amongst member states coming to the fore. Behind the scenes, some European governments are reportedly becoming frustrated with the more rigid approach taken by Michel Barnier and the European Commission, favouring instead a more pragmatic/flexible approach.

Judging by recent comments, a "divide and rule" approach by the UK does appear to be a concern in Brussels. According to the FT, Barnier has expressed frustration with Brexit Secretary David Davis "spending a lot of time" visiting European capitals, saying "I want David Davis to come to Brussels to negotiate".

The trade-offs between different Brexit models

What about the Customs Union?

Assuming the EU does reject the UK's proposal, this effectively leaves the government with three options. The first is the EEA, although this would involve freedom of movement, perhaps the reddest of red lines for the UK government. The second - and perhaps most likely outcome given the UK's red lines - is a Canada-style free trade agreement (although possibly with limited access to services). The third option is joining a customs union in goods with the EU.

So far, this has been strongly ruled out by UK ministers because it would prevent the government from pursuing trade deals with non-EU countries. It would also likely require the UK accepting EU regulations on goods. But the issue has come sharply into focus now that the opposition Labour Party has confirmed it favours the customs union option. There are also reportedly a number of Conservative MPs who also agree with the Labour stance, some of whom have proposed amendments to the government's trade legislation that would commit to joining a customs union after Brexit.

A vote on these amendments in the House of Commons has reportedly been pushed back by as much as two months, but given the government's working majority in Parliament is just 13 MPs (out of 650), the outcome would be very tight. As the FT noted this week, a defeat on this issue could be a major blow to Theresa May's leadership.

The EU has also raised the stakes by requesting Northern Ireland remain in a customs union as a "fallback option", should the overall Brexit deal fail to address hard border concerns. Theresa May has since said "no UK Prime Minister could ever agree" to this, not least because it would likely raise serious concerns within the Democratic Unionist Party (the DUP) over barriers to trade within the UK itself. Of course, nothing is agreed until everything is agreed, so it may not be until right at the last minute before a deal is struck. But until then, this issue is only likely to keep pressure on the government to compromise on some of its red lines, including customs union membership.

Key Brexit events in 2018

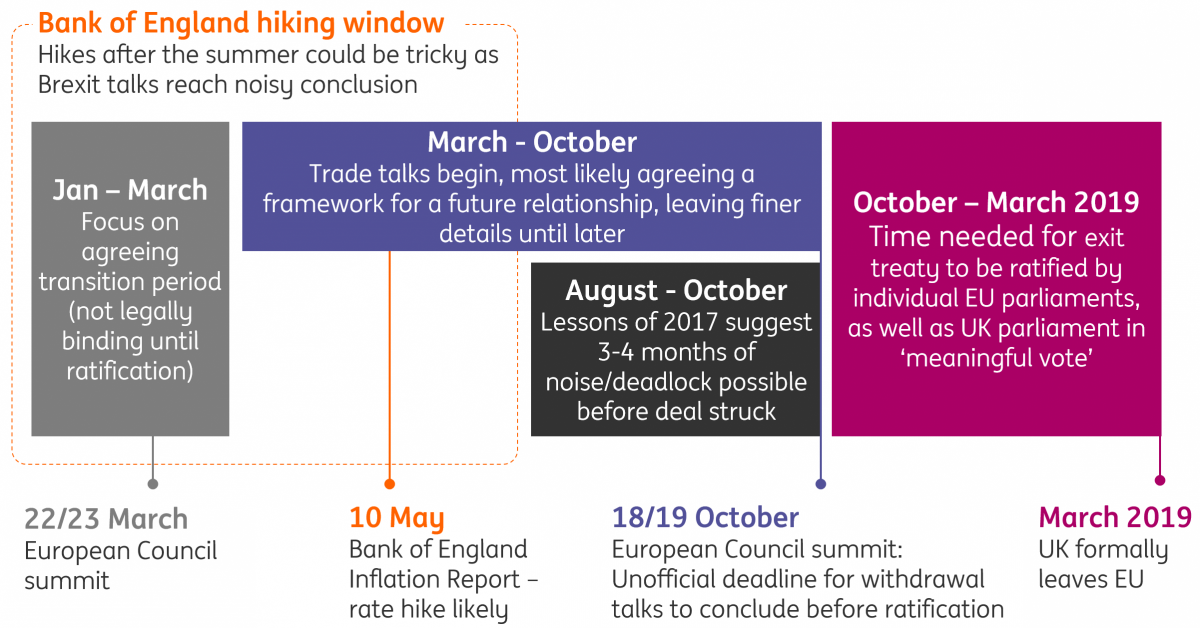

The short-term priority is agreeing upon a transition period

Aside from the trade deal itself, the big short-term priority for the negotiations is to get a post-Brexit transition period agreed in time for the March EU Leader’s Summit. That seems feasible, particularly given that both sides are clear that time is of the essence if firms are to be persuaded not to start preparing for the worst. But there are a few key legal issues that need to be sorted out first and Michel Barnier has said "significant points of disagreements" remain.

One thing both sides still subtly disagree is on exactly how long the transition should last. The EU has stated that the transition should end in December 2020, which coincides with the end of the current EU budget period. An initial draft of the UK's transition guidelines leaked last week opened the door to a more open-ended transition, although this has since been denied by the government.

It looks most likely that the UK government will agree to the EU's timeframe at this stage

With the clock ticking, it looks most likely that the UK government will agree to the EU's timeframe at this stage. European negotiators have made it fairly clear that an extension would require budgetary contributions beyond 2020. Key Conservative Brexiteers have also warned that keeping the UK aligned with the EU for longer than two years would be unacceptable, particularly ahead of the election scheduled for mid-2022. Negotiating a longer transition now could be a big political challenge.

That's not to say the transition period won't be extended later on. If negotiations take longer than expected, it is unlikely that the UK government would walk away and trigger "cliff edge" Brexit. It will also take time for businesses to adjust and re-orchestrate their supply chains, which in many cases often involve components travelling multiple times between the UK and EU before the final product is sold within the single market.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more