Solid UK jobs backdrop bolsters Bank of England’s rate hike case

At face value, the UK jobs market looks much like it did pre-pandemic. Taken with rising headline inflation, that makes a February rate hike look more likely. But a severe wage-price spiral looks unlikely, even if pay growth is close to pre-virus rates. That suggests the Bank of England will hike less quickly than markets are now assuming

On all the main metrics, the UK jobs market looks remarkably similar to its pre-pandemic state. The latest fall in the unemployment rate to 4.1% takes it to within a whisker of its pre-Covid level. The ending of the furlough scheme last September has been a smooth success, with no discernible increase in redundancies – a stark contrast to what happened ahead of the scheme’s original end-date in October 2020.

Alongside rising headline inflation rates and growing evidence that Omicron’s impact has been modest, a February rate rise from the Bank of England looks increasingly likely.

Redundancies have remained stable despite wage support ending last September

But markets are probably overestimating what comes thereafter. For Bank rate to head north of 1% later this year, as investors are currently pricing, we need signs that wage pressures are building further, akin to the trend seen in the US right now.

The data has been pretty hard to interpret recently, owing to various Covid-related distortions. But cutting through the noise, it looks like wage growth has slowed but remains roughly around pre-pandemic rates – which in themselves were at historically-elevated levels.

Some of this is undoubtedly due to skill shortages in parts of the jobs market, often a combination of lower inward migration and other structural factors. The chart below shows a reasonable link between sectors that have seen pay grow in excess of pre-virus trends, and those with vacancy rates above their historical averages. Unsurprisingly that’s in areas like transport/logistics – a function of lorry driver shortages and the rapid shift to online consumer spending during Covid.

Wage growth has exceeded pre-crisis trends in sectors with above-average vacancy rates

But part of the wage growth story through 2021 was probably also a by-product of the jobs market playing catch-up after the pandemic. There appears to have been strong demand for jobs both from employers and employees.

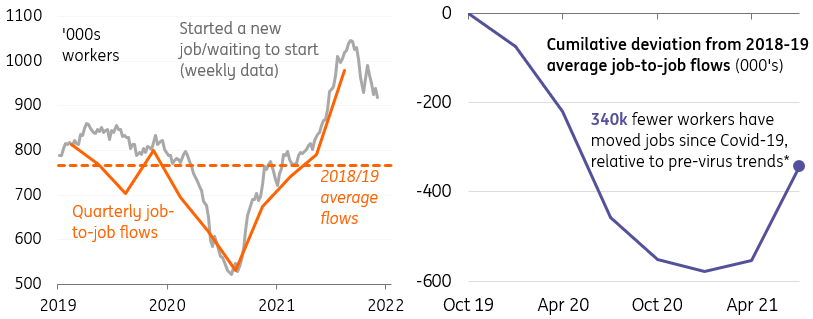

Vacancy rates are strong, though the number of people starting, or due to start, a new job was well-above historical averages through the autumn. This looks a lot like catch-up after a prolonged period of below-average job switching during the pandemic.

Indeed, if we added up job-to-job flows since early 2020 (albeit a fairly crude measure), they are still some way below what we’d have expected had pre-virus trends continued instead.

Job-to-job flows have increased since last summer's reopenings

Remember too that employment was always likely to rebound much more rapidly than after past recessions, owing to the heavy concentration of pandemic job losses (around half) in consumer services. These sectors have a history of both leading the wider jobs market out of downturns, and having above-average levels of employee turnover in a typical year.

We’d expect to see employment growth slow over coming months as this effect dissipates, potentially taking some of the pressure off wage growth if the initial mismatches we saw in the jobs market last summer have begun to fade.

In short, we think the jobs market is strong enough to support two rate hikes this year, in addition to the ‘quantitative tightening’ that the Bank is likely to undertake in tandem. But the lack of a severe wage-price spiral limits the case for raising rates faster and further than in any of the post-financial crisis years.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article