Softs volatility to continue

- 4 December 2023

- Commodities, Food & Agri

Soft commodities have been the best performing part of the commodity complex in 2023. Uncertainty due to the impact of El Nino and broader weather events suggest prices are likely to remain elevated into 2024

Global sugar market in deficit

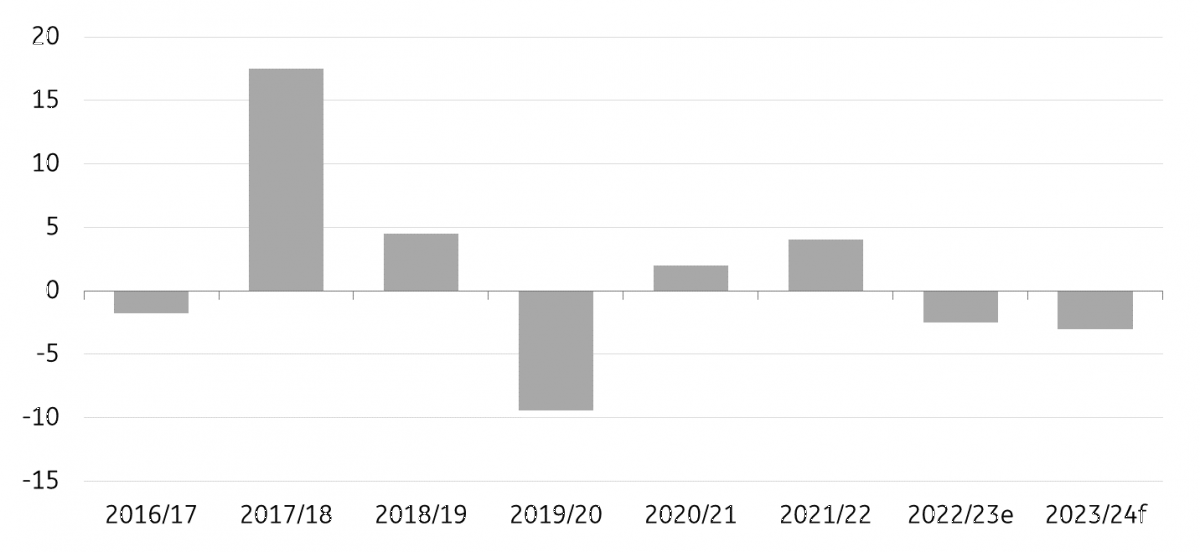

The sugar market has seen significant strength this year with No.11 raw sugar trading above USc28/lb and to its highest levels since 2011. The strength in the market has come despite Centre-South Brazil on course to produce its largest amount of sugar this season. A large crop from Brazil has been offset by worries over output from key northern hemisphere producers in 2023/24. The global sugar market is expected to be in deficit by around 3mn tonnes this season. It would be the second consecutive deficit, which suggests that prices will remain well supported through into early 2024.

The global market is usually relatively tighter in the first quarter of the year, given it coincides with the CS Brazil offcrop. However, with expectations of weaker supply from Thailand and India this season, the sugar market will be particularly tight over 1Q24.

Prices should ease from 2Q24 onwards as supply from the next CS Brazilian crop starts to come to market. The next crop is expected to see strong output yet again.

Meanwhile, the tightness in the European sugar market is likely to start easing slightly, which should take off some of the upward pressure we have seen on European sugar prices.

Record CS Brazil sugar output

The 2023/24 CS Brazilian harvest is drawing to an end and the industry is expected to crush well in excess of 600mn tonnes of cane, which should see sugar output hitting record levels this season of close to 40mn tonnes. Sugar prices have been trading at a healthy premium to domestic Brazilian hydrous ethanol, so there has been a clear incentive for mills to maximise sugar production. The sugar mix so far this season comes in at 49.41%, up from 45.97% over the same period last season.

While it is still early days and much will depend on how the weather plays out over the CS Brazilian offcrop, it appears as though CS Brazil will see another strong harvest in 2024/25, which gets underway in April. Sugar is set to remain at a strong premium to ethanol, ensuring the incentive to maximise sugar output will persist into next season. While we see strong sugar output, there will once again be logistical risks, given the expectations for yet another record Brazilian soybean harvest in 2024.

Indian and Thai sugar output under pressure

Developments in India and Thailand have been more of a concern, leaving the market tighter than expected this season. El Nino has led to drier weather conditions in Thailand, which has led to significant downgrades to the harvest that recently got underway. Some estimates suggest that Thai sugar output this season could fall into the region of 7.5mn tonnes, down from 11mn tonnes last season, which would be the smallest crop in over a decade. This would weigh on export supply for both raws and whites, and further tighten the market during the CS Brazil offcrop in 1Q24.

The prospects of no Indian sugar exports in the 2023/24 season will only intensify the tightness in 1Q24. The Indian government, which has issued export quotas in recent years, is yet to do so this season, given worries that a poor monsoon will weigh on the 2023/24 crop. Last season, the government allowed sugar exports of 6mn tonnes. Indian sugar output is estimated to fall close to 3% YoY to 30mn tonnes, and there are still downside risks to this. Weighing on sugar output even further is a larger diversion to ethanol production this year, a trend that we have seen for several years now as the government aims to increase ethanol blending.

The whites premium has remained elevated through this year, reflecting tightness in the white sugar market. And given the expectation for smaller crops from both Thailand and India, the white sugar market is likely to remain tight through at least early next year, which should continue to provide support to the whites premium.

EU sugar supplies improve

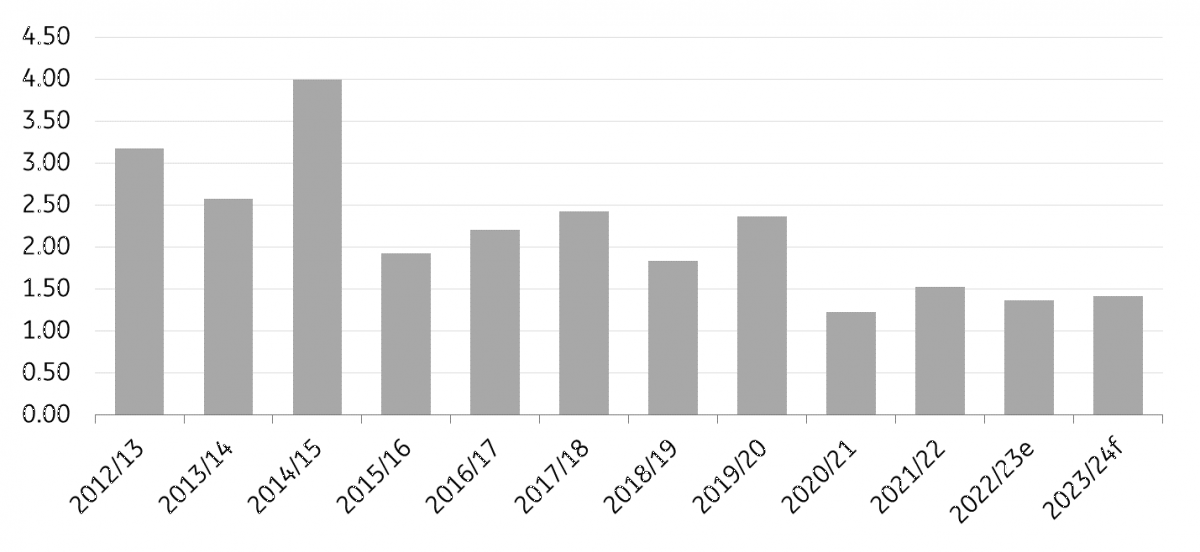

The European sugar market has seen significant strength over the last 12 months with EU output last season falling short of expectations due to dry summer conditions over 2022. This led to significant tightening in the market, which pushed prices (monthly average reported) to record levels of EUR821/t, whilst spot prices saw even more strength. For 2023, the region is expected to see somewhat of a recovery in output. EU production is expected to grow by around 1mn tonnes to around 15.6mn tonnes. This increase is driven by a combination of higher planted area and an improvement in yields. As a result, the balance is also expected to slightly loosen in 2023/24 with ending stocks to edge up to more than 1.4mn tonnes.

Back-to-back cocoa deficits

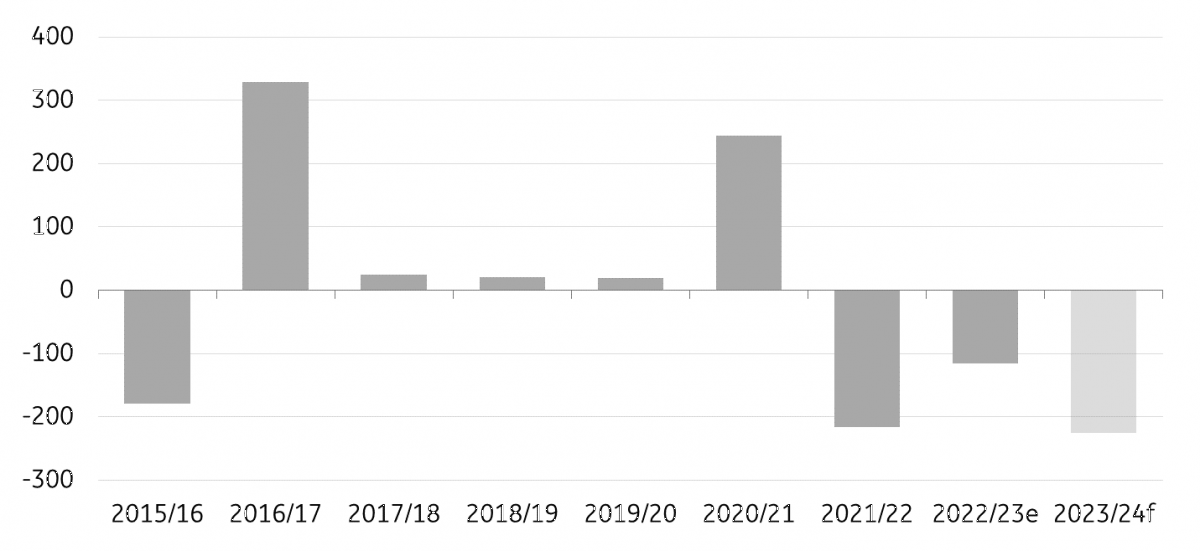

The cocoa market has seen significant strength this year with London cocoa hitting record highs. It is the second-best performing commodity this year, with just orange juice rallying more. Back-to-back deficits have tightened the market, and there is the growing likelihood of a third consecutive deficit in the 2023/24 season with concerns over output from West Africa.

The global cocoa market saw a deficit of 216k tonnes in the 2021/22 season, which was followed by a deficit estimated at around 116k tonnes last season. For 2023/24, early numbers suggest we could possibly see a deficit in the region of 200-250k tonnes. This is under the assumption of a large decrease in output from the Ivory Coast, and that the current high price environment leads to continued demand destruction.

A further drawdown in stocks would leave the market increasingly vulnerable, with global stocks at the start of the 2023/24 season estimated at around 1.7mn tonnes, whilst the stocks-to-grind ratio is at a seven-year low of 34.5%. However, it is still difficult to justify the scale of the move higher in cocoa prices, given these stock levels. Clearly, the uncertainty over the balance in 2023/24 is what is driving the market. If supply from West Africa does not turn out to be as bad as feared, the market is in store for an aggressive downward correction.

Ivorian cocoa supply under pressure

The key concern for the cocoa market is centered around the key supplier, Ivory Coast. Heavier than usual rainfall has raised worries over black pod disease and the impact this will have on output. In addition, rainfall has also led to transportation issues. Therefore, arrivals at ports are well below last year. There are some early estimates that suggest the Ivorian cocoa crop in 2023/24 could be as much 20% smaller YoY at around 1.8mn tonnes.

Demand responding to higher cocoa prices

It is no surprise that the high price environment we are seeing is already weighing on demand in a number of regions. Grinding data is down significantly in both North America and Asia. In Europe (the largest grinder), demand is proving to be relatively more robust. Higher prices are attempting to resolve the deficit through demand destruction. The latest data shows that grindings in North America were down 18% YoY in 3Q23, whilst grindings over the first three quarters of the year were down a little more than 11% YoY. In Asia, grindings were down 8% YoY in 3Q23 and down almost 4% YoY over the first three quarters of 2023. As for Europe, grindings were down 1% YoY in 3Q23, and a little over 2% lower over the first three quarters.

ING forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Commodities Outlook 2024: Cautious optimism

- This bundle contains 12 Articles