Softening US jobs market suggests the Fed’s work is done

The US August jobs report shows modest jobs growth, benign wage pressures and a large jump in the unemployment rate as the labour market slackens. With inflation set to continue slowing, the Fed is surely not hiking interest rates in September and is unlikely to do so in November either

| 3.8% |

US unemployment rate |

Employment growth is softening

US non-farm payrolls increased 187k in August versus the 170k consensus, but there are a net 110k of downward revisions to the past couple of months, indicating that the slowing trend in employment growth remains in place. The private sector created 179k of those jobs, led yet again by private education and health with 102k jobs. Leisure and hospitality also remains a healthy provider of employment with a 40k increase. Information (-15k), trade and transport (-20k – presumably Yellow bankruptcy related) and temporary help (-19k) were the key areas of weakness.

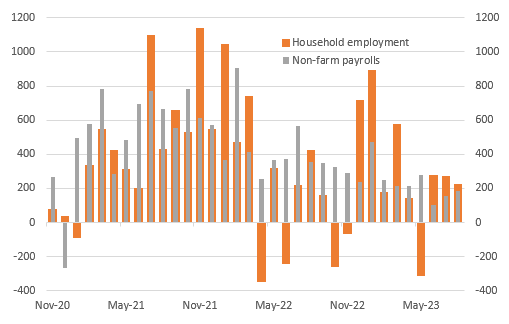

Payrolls gains versus household employment gains (000s)

Those numbers are all from the establishment survey of employers. The household survey, which is used to calculate the unemployment rate, reported a slightly stronger jobs gain of 222k, but the number of people classifying themselves as unemployed rose 514k with it seeming that more and more people are returning to the labour market. This increase in the participation rate is what the Fed wants to see and at 62.8%, it has risen nicely since a year ago when it stood at 62.1% and should help to keep wage pressures in check.

Wages cooling and unemployment is rising

In that regard, wage growth (average hourly earnings) is soft at 0.2% MoM, the smallest increase since February 2022, while the unemployment rate jumps to 3.8% from 3.5% (consensus 3.5%). It’s pretty safe to say the Fed isn't hiking in September with this backdrop, and we don't think they will in November either, with core CPI set to slow pretty rapidly in the next couple of months.

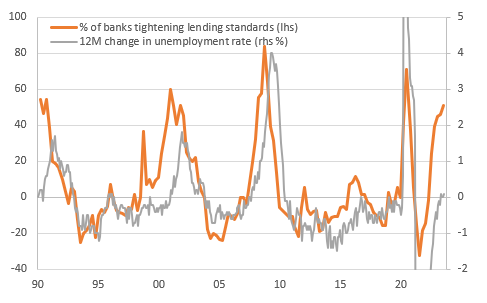

Tightening lending conditions point to a higher unemployment rate

The Fed's work is done

The chart above shows the relationship between bank lending conditions and the unemployment rate. With higher borrowing costs, less credit availability and student loan repayments all set to increasingly weigh on economic activity we fear that the unemployment rate will climb further. Unfortunately, it is unlikely to be just through rising participation rates but will likely involve some job losses too. As such, we continue to believe that US interest rates have peaked and the next move will be a cut. We are currently forecasting that to happen in March 2024.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more